Two financial pressures are increasing on households across the UK – the mortgage (or rent) and energy bills. As the Bank of England (BoE) raises interest rates, lenders are pushing their own rates higher too. This creates challenges for homeowners but also potentially some opportunities to overpay on the mortgage. Higher inflation has also arrived, especially in the form of higher electricity, gas and petrol prices. In this article, our Carlisle financial planners at Vesta Wealth explain how the landscape is shifting in these two areas and offers ideas about how to prepare your financial plan.

Plan for your mortgage

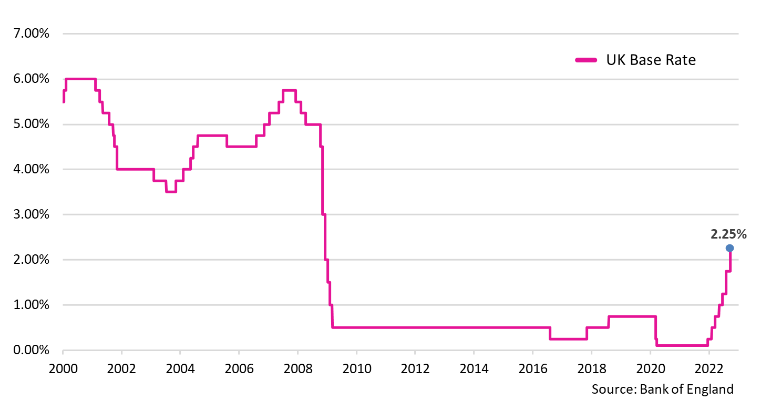

Only last year in 2021, the base rate was at a historic low of 0.10% – enabling banks to offer mortgage deals at record-low interest rates (one lender even offered a 0.95% two-year fixed). Since then, however, the BoE has raised the base rate 7 times and it now stands at 2.25%. Future rises are expected, possibly to 6% or higher, by early 2023. Already, mortgage holders are being affected.

The 0.50% hike on 22 September already means that a homeowner with a £270,700 property value could face a £196 higher monthly payment than last November (assuming a loan-to-value of 75%). If the base rate rises to 3% before November 2022, which some in the market expect, then an average 2-year fixed deal for someone with a 25% deposit could see their interest rate go from 4.14% to 4.89% (possibly adding another £100 to monthly costs).

Of course, rising mortgage costs may not transpire for you. However, now may be a good time to review your monthly finances to make sure you can maintain stability, especially since the winter months are typically more expensive (e.g. higher heating bills and Christmas costs). If you have extra cash savings or disposable income, then higher mortgage costs could be an opportunity to overpay your mortgage (e.g. if the rates exceed those on regular savings accounts). However, speak to your financial adviser to make sure that overpaying fits into your wider financial priorities and plan such as ensuring you also have a strong emergency fund.

Plan for energy bills

Only a few months ago, some experts were forecasting annual energy prices as high as £6,000 by April 2023. There were also warnings of an 80% price hike to £3,576 by October 2022. With the government’s new Energy Price Guarantee, however, the ‘average’ household’s energy bill will be ‘capped’ at £2,500 until April. Whilst there are certainly drawbacks to this policy (such as adding more debt to the public purse), it does let households plan ahead more confidently for their energy costs this winter.

Take care not to assume that you can now be cavalier with your energy consumption. Bear in mind that the £2,500 figure relates to the average bill for a typical household based on 2019 consumption figures. It is not the bill itself that is capped, but the actual unit costs of energy and standing charges which are capped. As a result, if you use more energy than average you will have a higher bill, if you have lower-than-average usage you will likely have a lower bill.

As examples, for electricity, the average standing charge will be 46p per day and 28p per day for gas. Those living in a detached house, therefore, may face a bill of £3,300 for the year under the new guarantee (based on government figures for average costs). Those in a semi-detached house may face costs closer to £2,650. People in a purpose-built flat may pay £1,750, whilst those in a bungalow might pay £2,450.

Those entering a new energy agreement from October 2022, therefore, may still end up paying over the £2,500 guarantee for the following 12 months. It may be helpful to discard the idea of a maximum energy bill and focus on your actual usage. If you limit your energy consumption in the coming months, you might even pay less each month for energy than you do now. This might be particularly true when factoring in the £400 energy bill support scheme. Doing so could help you mitigate a possible rise in your mortgage costs, open opportunities to strengthen your emergency savings and allow more contributions to your long-term investments (e.g. your pension).

For those on the State Pension, be aware that the Energy Price Guarantee may lower how much extra income you expected to receive in April 2023. The State Pension had been on track to rise by over 10% (in line with inflation). However, the new guarantee is expected to mute the inflation figures used under the “triple lock” system to determine State Pension entitlement for the tax year. Therefore, your State Pension may only rise by 3.7% (although it may be higher if UK inflation remains persistently at the current high levels).

Invitation

If you would like to discuss your financial plan and retirement strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

e: [email protected]

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.