Watching your portfolio rise and fall significantly during volatile markets can be deeply uncomfortable. Yet one of the worst things you can do is pull your money out in a panic. This just serves to crystallise your losses and potentially causes you to miss out on the recovery afterwards (after all, stock markets tend to go up in the long term). How can you keep your head during a falling market and how can you protect your portfolio “from yourself”? Below, our team at Vesta offers some tips from our Carlisle financial planners.

Be careful about “timing the markets”

At the time of writing, the UK stock market is holding fairly steady – despite forces which are pushing it downwards (e.g. rising interest rates). As questions still circulate about whether the UK could enter a recession, investors could be seen as waiting for a “dip” in UK shares – intending to then jump in and buy at lower prices, in preparation for a later rebound. Indeed, some investors have benefitted from this approach before. When global markets crashed in March 2020 when Covid concerns spread to investors, some investors “bought the dip” at/near the troughs that appeared with the FTSE 100, S&P 500 and other key indexes – enjoying impressive returns when these soon rebounded only months later (partly due to confidence from government and central bank support policies).

This time around, in October 2022, some investors are tempted to hold their money and wait for another dip in stock markets. Already, the S&P 500 has fallen over 25% since the start of the year and the Dow Jones is down over 20%. With the Federal Reserve increasing interest rates and expected to raise them further into 2023 to counter inflation, there is a possibility that these indexes could fall even more. The problem with all of these forecasts, however, is that they are just predictions based on assumptions about the economy, global events and sentiment in the markets. It is impossible to predict what will actually happen.

The risk of building up cash and waiting for a “dip” is that you miss out on the growth you might have achieved by investing it gradually instead. This “pound cost averaging” approach is often preferable for individual investors, since it helps many people stomach the risk involved with investing their money. At certain times, your contributions will buy investments when they are “highly-priced” and, other times, you will buy “at a discount” (when the markets fall). This takes away much of the temptation to try and time the markets, which is nearly impossible even for professional fund managers to do effectively and consistently.

Take the long-term view

If you approach investing with a short-term mindset, trying to make money “quickly”, then you will likely make costly mistakes. When your shares go down, you will be tempted to sell them to try and limit your losses and move the money into another “hot” investment to try and recover and surpass what you originally had. A long term investor, however, accepts that their portfolio will fluctuate in value along their investment journey. In the years ahead, they can be confident that their strategy and patience will result in more wealth.

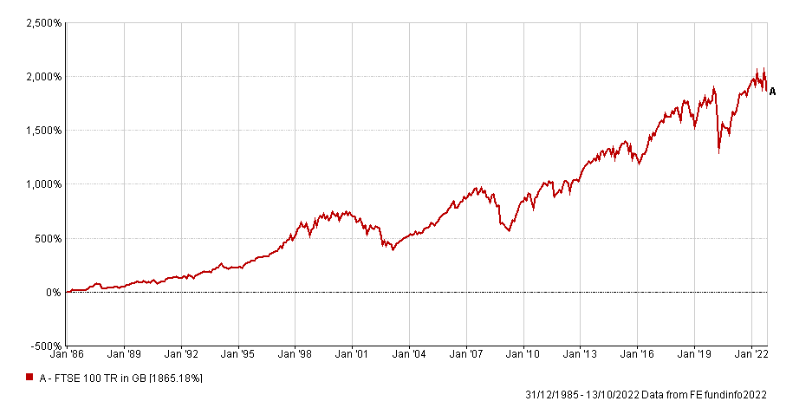

Taking time to consider the facts about markets can help you keep a level head when you feel the urge to start “day trading” with your investments (buying and selling regularly). Stock markets, for instance, tend to go up over time because the economy grows and the top corporations within the major indexes earn more money. Between 1950 and 2021, for instance, the S&P 500 has averaged an 11.53% return per year. Here in the UK, the FTSE 100 has given an average 7.75% return per year since its inception. These figures are despite many “shocks” and bear markets along the way, including the 2008 Financial Crisis and the more recent covid stock market crash. In other words, markets rise and fall in the short term; yet in the long term, the markets tend to rise.

This is not to say, however, that you shouldn’t take care with your risk. If you intend to retire in the near future, for example, then the last thing you want is your portfolio dropping sharply as you look to start accessing your money. This is why working with a financial adviser can help, since professional guidance can help you position your portfolio as you get older to ensure your income needs are met as you near the “decumulation” phase of your investment journey. Whether you are looking to purchase an annuity or withdraw a sustainable level of income from your investments it might require a change in strategy. This might involve moving investments out of more “volatile” assets (e.g. growth shares) into “safer” ones, such as certain dividend-paying shares/funds and UK government bonds.

Invitation

If you would like to discuss your financial plan and retirement strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

e: [email protected]

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.