Published 24 October 2022 (before Rishi Sunak’s instalment as Prime Minister)

For several years now, investment commentators have found themselves much absorbed in political machinations. This is a global phenomenon, but one that continues to be poignant in the UK. If we look back as far as the Scottish Independence Referendum in 2014, there have been many false dawns promising stability. Meanwhile, the Brexit process has exhausted the political machinery of government and continues to divide the population.

The extraordinary events of summer and autumn 2022 appear to have taken this trend to a new level. If we take the most recent examples, there are both differences and similarities. The resignation of Boris Johnson in July 2022 was related to the standards of conduct expected by the public from those who govern them. This is of course particularly important at times when the public are asked to make large sacrifices in the national interest. The ensuing historically short tenure of Boris Johnson’s successor, Liz Truss, encompassed matters pertaining to both ideology and standards of conduct. Leaving aside political ructions, the UK faces the same problems confronting many developed nations. The most pressing being debt, the cost-of-living crisis and the distribution of wealth.

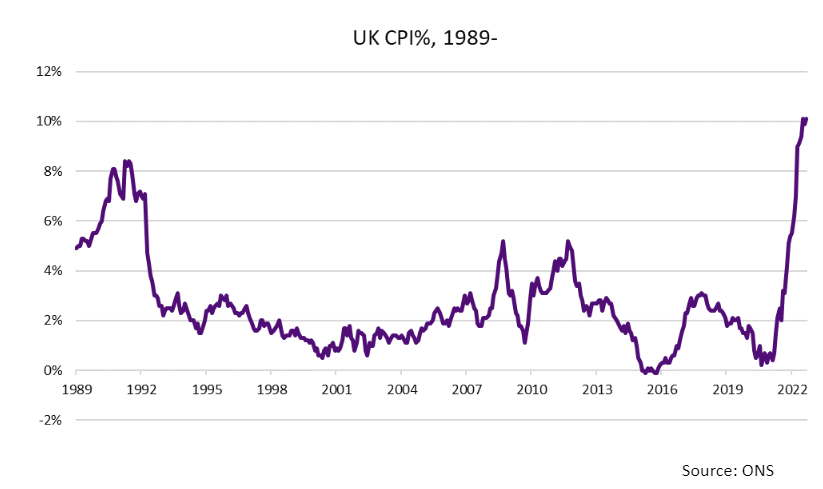

Addressing monumental issues such as the Covid-19 pandemic, and surging energy costs, has placed enormous strains on public finances across the world. This can be seen in the deterioration of debt to gross domestic product (GDP) ratios which in the UK was measured at 96.8% in March 2022. A further complicating matter is the lower levels of growth and disappointing productivity performance in the UK.

Source: ONS and OBR

There are two prominent approaches proposed to this conundrum. One being ‘austerity’, reducing the debt part through the restoration of public finances by reducing spending to create a stronger foundation for the economy to prosper. The other entails ‘going for growth’. Instead growing the economy which will hopefully generate higher taxation receipts to stabilise public finances, and wealth to cascade down to all constituents of society.

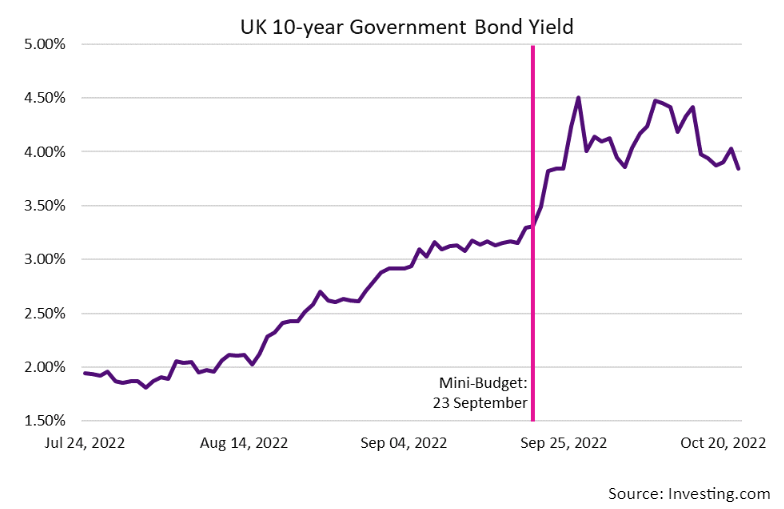

The latter was the approach pursued by the short-lived Truss administration. This approach requires higher short-term borrowing and lower taxation. Communication is crucial to secure the confidence of financial markets, and the wider populace, a factor overlooked by Liz Truss and Kwasi Kwarteng. A shock and awe style ‘Mini Budget,’ along with the scant regard of independent institutions such as the Office of Budget Responsibility (OBSR), and the Bank of England, proved to be poor foundation upon which to build a policy.

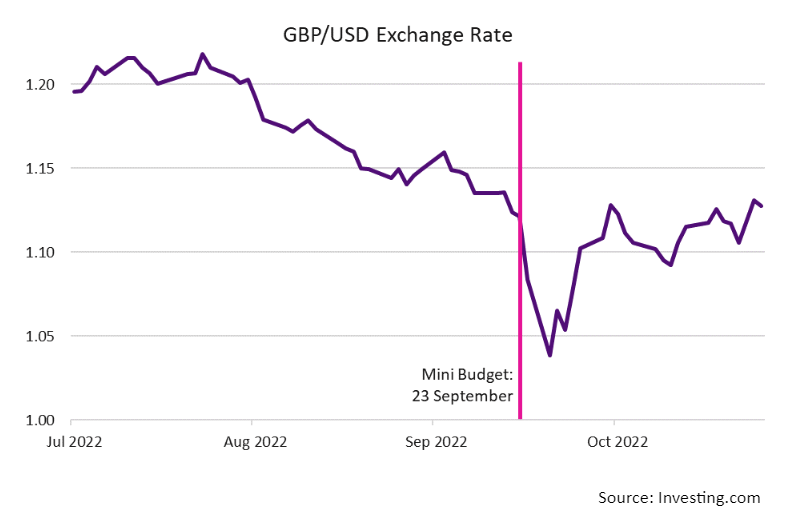

Matters were exacerbated by the strength of the US dollar, fuelled by a programme of aggressive monetary policy tightening by the Federal Reserve. This has had the impact of creating a flight to quality and has drained liquidity from risker areas of the global financial system. Consequently, sterling-based assets suffered a sharp sell-off. Pound Sterling fell to an all-time low against the dollar; while spiralling gilt yields prompted the Bank of England to intervene, temporarily, in the gilt market in order provide breathing space for pension schemes operating liability driven investment (LDI) strategies.

The scale of the miscalculation of the content, and presentation, of the ‘Mini Budget’ prompted the appointment of a new Chancellor, Jeremy Hunt, and the reversal of many of the policies which secured Liz Truss the leadership of the Conservative Party. Such a series of extraordinary U-turns led to the inevitable demise of Liz Truss’s Prime Ministership.

Thus, the short-term stability provided by Jeremy Hunt’s reversal of the more contentious elements of the ill-fated ‘Mini Budget,’ ran into a new wave of uncertainty, concerning who will run the UK, and what policies will they pursue? At the time of writing, the likely successor appears to be former Chancellor, Rishi Sunak. Boris Johnson’s modern-day interpretation of classic history has fallen on the sword of his own turbulent, and all too recent, term as Prime Minister.

But whatever the outcome, households, businesses, institutions, and financial markets, desperately require stability. There will be tough decisions to make, and unpalatable policies to implement. However once we can see broadly what is proposed, lives, business plans, and investment strategies, can be structured accordingly.

Stepping away from domestic politics, the ongoing war in Ukraine, and its wider ramifications for energy markets, remains a complicating factor. The conflict has become one of attrition, both militarily and economically. With winter approaching, the momentum of the conflict may wane, however, strains on European energy infrastructure will be more acute, and the efficiency of which provisions have been built up over the summer months revealed.

With the cost-of-living crisis still pressing, financial markets are heavily fixated on the monetary policy of the Federal Reserve. Investors are looking for signs of inflation peaking, and with it, where interest rates will settle. Any indication of a moderation in monetary policy tightening will likely be received favourably by financial markets. Calling a turn in markets is notoriously difficult. They are forward looking, and do not pause to allow investors to allocate capital when circumstances appear brighter. For the patient longer term investor, volatility can present very profitable opportunities.