To succeed when Investing, you need wisdom (and a bit of luck!). A core part of being wise as an investor is to diversify properly. Yet what is diversification? Why does it matter and how do you do it?

Diversification is the practice of “spreading out” your investments – both within and across asset classes. For instance, the latter might involve diversifying across shares, bonds, cash and property. The former might involve investing in many different types of company shares – e.g. different industries and countries.

In this article, our Tees Valley financial planners explore the main reasons why diversification matters when investing. We also offer some ideas to achieve a well-diversified portfolio.

Diversification and risk management

Suppose you invest most of your money into a single company and its stock price crashes. If it never recovers, you have potentially lost all of the capital.

By investing in, say, hundreds of companies (even thousands) you can reduce the impact that a single stock failure would have on the overall value of your portfolio.

However, what if the stock market itself crashes (a “bear market”)? This can result in thousands of shares falling in price simultaneously – pulling down a portfolio.

This is where spreading investments across asset classes can help reduce your risk. For instance, if you are 50% invested in shares and 50% invested in bonds, then you will likely be far less affected by a stock market crash compared to someone 100% invested in the former.

However, this is not to say that investors should never favour particular asset classes when building a portfolio. Indeed, it can be appropriate to build portfolios comprising 80% shares or even more, depending on the investor’s goals, risk tolerance and strategy.

To be most confident in your asset allocation, it helps to speak with a financial planner. This gives you a second pair of experienced eyes on your investments to give you the best insights and peace of mind.

Diversification and investor psychology

Humans are influenced by powerful emotions when it comes to investing. Loss aversion can be especially compelling – i.e. the fear of increasing losses as an owned share falls in price.

This can lead an investor to “cut and run” to try and avoid further losses. Yet this often results in “crystallised losses” if the share price later recovers.

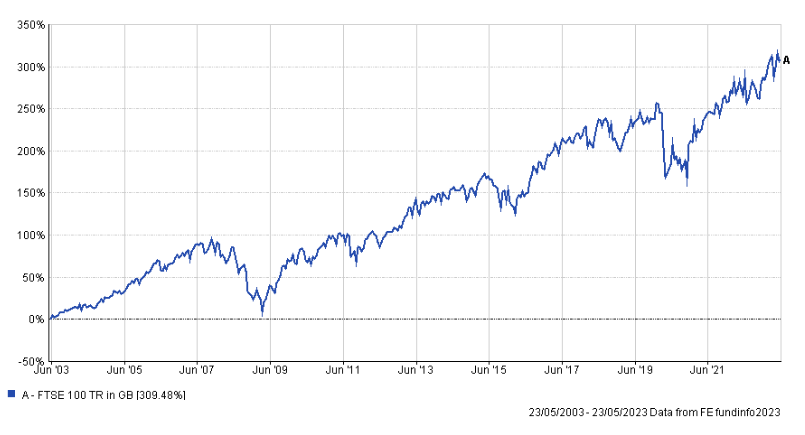

Investment growth never happens in a straight line. Rather, a line graph of your portfolio would likely show “ups and downs” along the way – hopefully, also with an overall upward trend. As an example, see the below chart of the FTSE 100 showing its growth over the last twenty years.

In an ideal world, investors would recognise this long-term trend and stay invested during any market volatility – confident that their long-term strategy will eventually carry them towards their goals.

However, humans rarely work like this. We need to account for our psychological makeup when building an investment strategy. This is where diversification can help.

Diversification can help to “dampen” the volatility of a portfolio in the short term, making it easier for the investor to cope with. The appropriate level of “dampening” will vary across investors depending on personality traits such as risk tolerance.

It is difficult to be honest with ourselves about our ability to cope with investment risk and volatility. A financial planner can help you ask yourself the risk questions and build a portfolio which best reflects you – minimising the chance that you will make impulsive decisions in the future based on powerful emotions, such as loss aversion.

Diversification and retirement

Eventually, you may wish to retire and use your investments to help provide a steady income. This might involve taking dividend payments from certain shares. It could also mean selling certain investments gradually to release cash that can be spent on your lifestyle.

However you take a retirement income, diversification is essential to protect your wealth and ensure that you do not outlive your investments.

For instance, suppose you rely entirely on dividend-paying shares to finance your retirement. What if a market crash occurs one day, leading most of these companies to “tighten their belts” to maintain their business – e.g. suspending, cutting or even cancelling their dividends?

This happened in 2020 when the Covid pandemic hit global markets. Even longstanding UK dividend-payers, such as banks and telecoms companies, cut or deferred their payments to investors.

By diversifying your income sources in retirement, you can minimise the potential negative impact should one (or more) of these sources fall or stop.

For example, an individual in retirement could generate income from their State Pension, a final salary pension (from a previous employer), a private pension (which has consolidated multiple pension pots over a career), an annuity and perhaps rental income from a buy to let property.

In this example, should a problem arise with one particular income source, the individual still has four other income sources to sustain them in retirement. Diversification, in this respect, is another form of financial protection!

Interested in exploring how to best diversify your investments? Our Tees Valley financial planners here at Vesta Wealth can assist you.

Invitation

If you would like to discuss your financial plan and retirement strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.