Stability appears to have returned to financial markets following recent turbulence. Markets were reeling in March following a flurry of banking failures, including Silicon Valley Bank and Credit Suisse, which raised questions over the stability of the wider financial sector. Despite March’s volatility, at the time of writing, developed market indices broadly remain in positive territory for 2023.

High Inflation

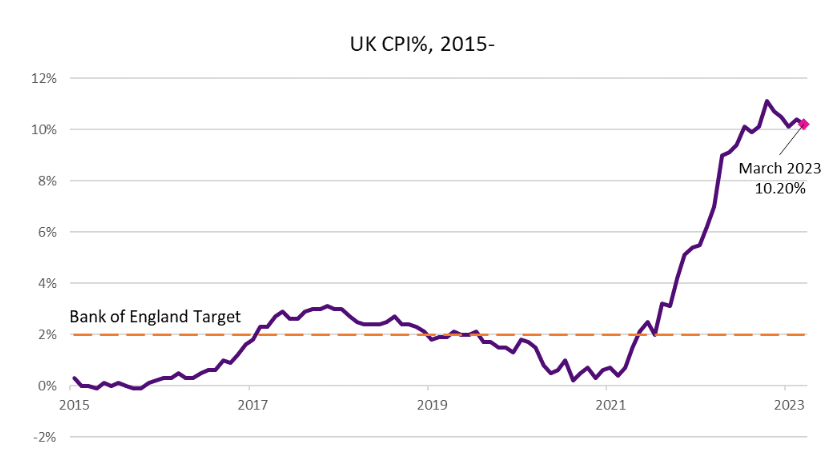

The economic landscape continues to be mixed. The UK consumer price index (CPI) measurement for March 2023 defied forecasts, remaining above the double-digit level at 10.20%. A modest retreat from the February reading of 10.40%.

With the Bank of England having only increased the base rate to 4.25% in March, financial markets moved to price in a further 0.25% increase at the forthcoming May 2023 meeting. Expectations were also raised for an additional hike in the summer. Central banks however will remain data vigilant as it continues to balance curbing price rises without disrupting economic activity.

The biggest culprit driving inflation increases is still food price inflation. As measured by the ONS, Food prices in March rose by 19.1% compared to the same period last year, the fastest pace of increase since 1977. Data from April suggests a slight slowing to the speed of food price increases as data provider, Kantar, have estimated that grocery price inflation has fallen to 17.30%. Despite this forecast slowing, there is no immediate relief on the horizon for households with already strained finances.

While Inflation is still expected to fall steadily during the second half of 2023, it is proving stickier in the UK. The UK has the highest inflation rate in the G7, currently double the rate recorded in the US, and comfortably over the Eurozone level of 6.90%. This makes for a challenging environment for the resolution of ongoing pay disputes, with the government keen to avoid further stocking inflation, and employees anxious to safeguard their own living standards.

Economic Resilience

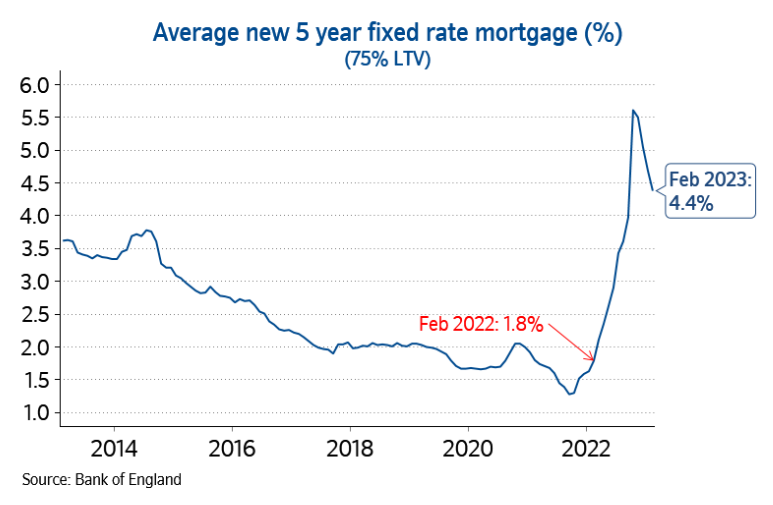

Despite the ongoing cost of living pressures, the UK economy has thus far avoided a recession. However the persistence of low growth is unwelcome and has been an impediment to recovering to pre-pandemic levels. One particular area of concern for the economy however is the impact of rising interest rates on mortgage repayments.

With potentially 3 million households facing higher mortgage payments, either via floating variable rates or expiring fixed rate terms, any abatement in the rate of inflation will provide useful relief. The concern for the housing market was that as mortgages became more expensive, this would put downward pressure on house prices. So far these concerns have not been realised with the UK housing market showing resilience. Measures of house prices have been little changed, supported by still high employment levels.

There was also better news on public finances. Higher than forecast taxation revenues saw borrowing reach £139.20bn in the financial year to March 2023, lower than the forecasted figure of £152.40bn. The negative impact of inflation on household finances has boosted government income as rising prices has provided a boost to VAT receipts. There has also been strong growth in collections from the self-employed, higher rate taxpayers and corporation tax following Chancellor Jeremy Hunt’s move to restore public finances to a more stable footing. With a general election due next year, debate will shift to the scope for tax cutting ahead of the vote.

Market Activity

While profits warnings from UK listed businesses have increased, reaching post pandemic highs, bargain hunters have been at work. Dechra Pharmaceuticals, Wood Group, THG, Network International, Medica Group and Industrials REIT have all been subject to bid activity as depressed values appear attractive to companies looking for takeover opportunities. This suggests pockets of value exist in the market, and companies looking to expand are not showing signs of caution.

In the US, first quarter earnings season commenced in a muted fashion. On a positive note, major US banks, JP Morgan and Bank of America reported solid results. A suggested loss of momentum in the US jobs market placed the US dollar under pressure, as investors mulled the impact of rising interest rates on the US economy. The Federal Reserve is expected to remain vigilant to remaining inflationary pressures, as the core rate, excluding more volatile items such as food and energy, ticked up slightly to 5.60%.

Over in Asia, the Chinese economy grew by 4.50%, year on year in the first quarter of 2023, exceeding forecasts of 4.0%. This was helped by strong retail sales, as physical stores reopened and enjoyed a release of pent-up demand following covid. The Chinese Government is working to an annualised target of 5% growth for 2023, as real estate investment remains in decline. Despite more positive economic growth, financial markets in the country remain below developed market peers.

As interest rates have risen, this has had a negative impact on the capital values of bonds. With forecasts suggesting inflation is far from slain, some market participants are expecting further interest rate rises, leading to bond yields rising further. Despite these rises and the impact on bond prices, after a torrid year in 2022, higher quality bonds appear to be trading at a more attractive level.

As always, geopolitical risk is difficult to gauge. Markets have become muted to the noise of the Ukraine war and its impact on the supply chains, particularly those of oil and gas. The spring months are expected to see a renewed offensive from the Ukrainian military, however there is little international consensus over a plan for peace. Meanwhile, tensions over the sovereignty of Taiwan remain sensitive, with western nations seeking to find constructive ways to engage China.

Invitation

If you would like to discuss your financial plan and investment strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

e: [email protected]

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.