Is it ever too late to start a pension? Many people do not think about their retirement plans until much later in life. At which point, a lot of time has been lost to contribute towards your pension. You will need to work harder to make up for lost ground. Yet it is still possible.

Below, our Teesside financial planners at Vesta Wealth offer a short guide for those who fear they have left pension planning to the “last minute”. Please contact us for more information or to speak with a financial adviser:

t: 01228 210 137

e: [email protected]

Why time matters

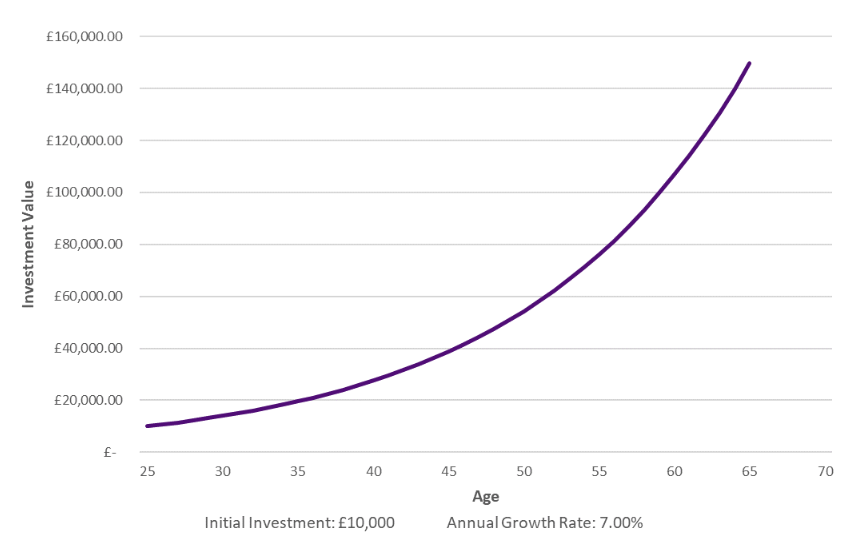

One of the main benefits of starting a pension early is that your savings can benefit from compound interest. Suppose you invest £10,000 when you are 25 and leave it invested in a portfolio, returning an average of 7% per year after accounting for any fees. By year 20, the total amount could stand at over £38,000. However, by year 40 it could stand at nearly £150,000.

This “snowballing” growth happens due to “interest generated upon interest” (i.e. compound interest). However, if you have left pension planning until later in life, you have less time for compound interest to work its magic on your portfolio.

Now suppose you start pension saving at age 60. To get to a similar target of around £150,000 in only 5 years, you may need to commit a £110,000 lump sum into a portfolio (assuming the same 7% annual returns). In short, the longer you wait for pension planning, the more it is likely to cost out of your own pocket.

What should I do?

If you think you have left it too late to start pension planning. Firstly, do not lose hope. It may be discouraging to hear about the opportunity cost you have incurred by delaying your pension plan. Yet there may be more possibilities for you than are immediately clear to the eye.

A good initial step is to check your State Pension. The chances are, you have built up National Insurance (NI) contributions automatically over your career – giving you a future income entitlement. You need at least 10 “qualifying years” of NI contributions on your record to get any State Pension at all. To get the full new State Pension of £203.85 per week, you need 35 years.

£203.85 per week equates to £10,600.20 per year in 2023-24.Given that a recent study suggested at least £12,800 is needed to sustain a minimum living standard for a single person in retirement, the State Pension can lay a strong foundation for your future finances. You can check your NI record for free on the government’s online portal.

Taking more proactive steps

Your State Pension situation will help to guide your next steps for your retirement plan. For instance, if you want to retire in 5 years (when you reach State Pension age) but have 25 qualifying years on your record, you need another 10 years to get the full new State Pension.

Working another 5 years gets you halfway there. However, to achieve the remaining 5 years you may need to explore other options – e.g. voluntary NI contributions and/or delaying your State Pension. It is wise to consider financial advice at this stage to gain all relevant information.

Even with the full new State Pension, however, it is unlikely the income will cover your full income needs in retirement. You will also need other income sources – e.g. an annuity and/or income from flexi-access drawdown – to help you achieve a more comfortable lifestyle.

The good news is that it is not too late to open a pension in your 50s, 60s or later. If you are employed, consider your workplace pension. Have you been contributing to it? If so, how much do you have saved? Are there other, older schemes (e.g. from past jobs) where you may also have pensions that you have forgotten about?

Tracking down old/lost pensions is a good idea at this point. A financial adviser can help you do this more thoroughly and offer guidance on what to do with them. Perhaps consolidating them into a single pension “pot” could help you manage things more easily, keep fees down, and open more investment options for you.

With a clearer idea of your assets – e.g. State Pension and workplace/personal pensions – you can begin to plot a course to close the gap between your current financial position and where you want to be in retirement.

For example, perhaps you need another £100,000 in your pension pot before you can safely achieve the future income you want. In which case, how much do you need to contribute to your pension over the coming years to achieve that target?

What kind of investment strategy will be used along the way? Here, you need to carefully consider your attitude to risk and your time horizon. If you are near retirement (e.g. 5 years away), then you may want to take a more “cautious” approach to your portfolio – e.g. leaning towards bonds rather than equities – since you do not have a lot of time for your investments to recover if there is a market downturn.

Invitation

If you would like to discuss your financial plan and retirement strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

e: [email protected]

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.