Following a long succession of interest rate increases in developed markets, the narrative has shifted to a plateauing of monetary policy. With inflation showing signs of falling, many market commentators have suggested that interest rates may be approaching their ‘peak’. However, with inflation still elevated, debate remains as to whether central banks will see their job as complete in combating rising prices, and indeed how quickly interest rates might then be allowed to fall.

Inflation vs the economy

There are a lot of variables in the discussion of interest rates and their impact on investment markets. One of the principal concerns is the impact of higher interest rates on the health of economies. To add to these concerns, there are many estimates over how long it takes for interest rate changes to impact the economy. Some suggest a lead time of up to 18 months. As interest rates have risen so quickly, it is unlikely the full impact of these increases has been felt.

This has created a complex dilemma for central bankers trying to restore inflation to desired levels. Central Banks, who were criticised for being too slow in taking action to combat inflation, are now worried of the risks of overtightening which could lead to economic damage. Rather than pushing on with rate rises until inflation returns to target levels, there is an acknowledged desire to ‘pause’ interest rates around their current level. This might allow prices to settle in a more orderly fashion while assessing any economic headwinds which result.

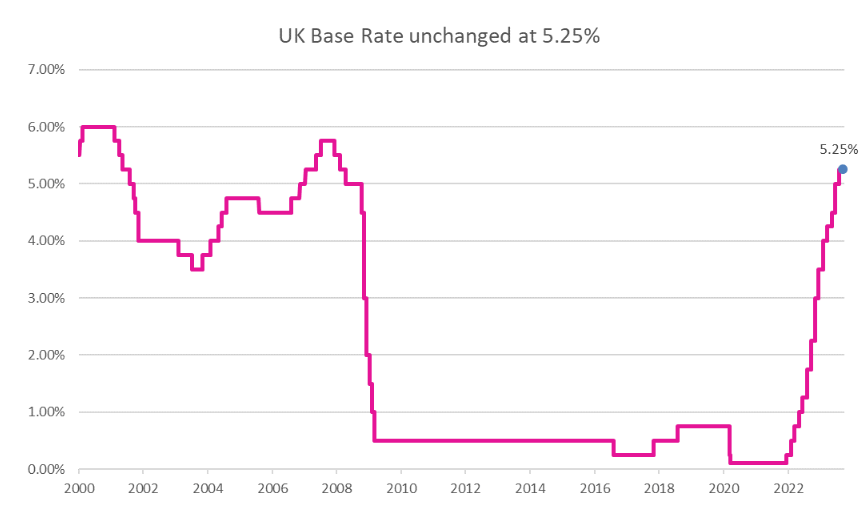

This ‘pause’ of interest rate rises was seen in September when the Bank of England (BoE) narrowly voted to leave rates unchanged at 5.25% following a run of 14 consecutive rises. The decision was taken by the bank following data which showed that inflation has fallen in recent months. The bank did however stress that further action would be taken if needed.

Inflation remains high

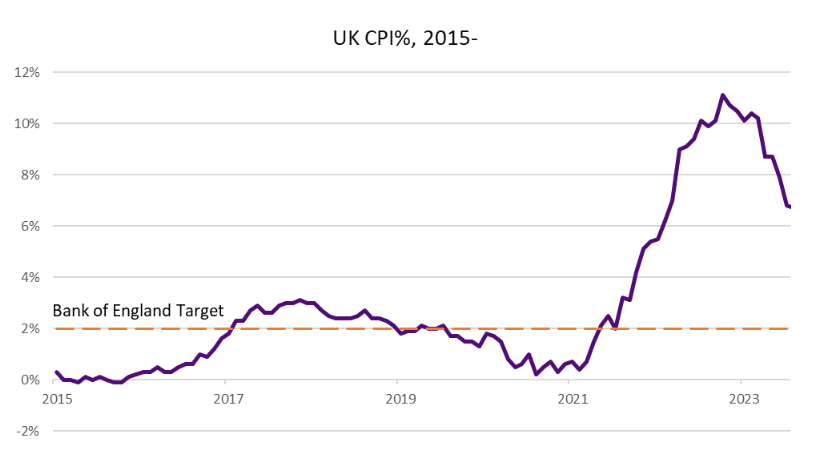

In August, UK Consumer Price Index (CPI) inflation was recorded at 6.70%, marginally down on the prior month reading of 6.80%. Market expectations had been for a slight increase, owing to the disruptive impact of higher fuel costs, so this was a positive surprise. Pleasingly, core CPI, which excludes the more volatile components such as energy, food, alcohol, and tobacco, also declined from 6.90% to 6.20%.

While inflation appears to be trending in the right direction, these inflation readings remain uncomfortably high. The difficulty for the BoE is balancing the impact of rising prices against the growing stream of weakening economic data. With mortgage financing becoming more expensive, the housing market has shown weakness with estimates that UK house prices fell by 5.30% in the year to August. The largest annual decline in 14 years. Furthermore, the labour market has also shown signs of cooling, with lower vacancy rates and higher redundancies. Industry surveys have also given a sign of a slowdown in economic activity. While none of these figures are a guarantee of recession, there is a suggestion the economy is starting to feel the impact of tighter monetary conditions.

A global problem

These challenges are not unique to the UK. To varying degrees, many key economic geographies are confronting challenges. Earlier in the month, the European Central Bank raised rates for a 10th consecutive meeting to 4%, the highest level since the creation of the single currency. There are also signs of economic slowdown in Europe. The German economy is struggling the most amongst the Eurozone members amid sluggish demand from China, and the institution of a new energy policy owing to events in Ukraine.

In the US, in a similar fashion to the BoE, the Federal Reserve elected to hold rates at their current range of 5.25% to 5.50%. With inflation running at 3.70% in the US, the Federal Reserve noted that tighter credit conditions would exert downward pressure on inflation. In contrast to the softening economic data in Europe, the US economy has shown comparative resilience to higher interest rates so far.

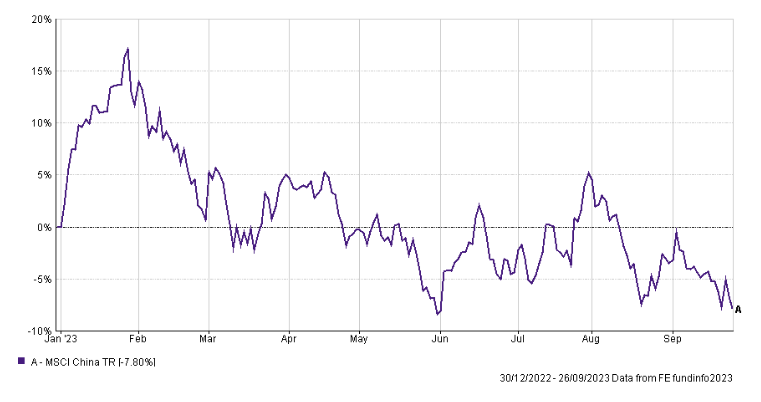

Over in Asia, the Chinese authorities have in contrast to developed markets been loosening monetary policy, via lower interest rates and relaxed reserve requirements for banks. This follows a loss of momentum in the economy following the end of the zero-covid policy and ongoing challenges within the real estate sector. Investors are cautious over the future outlook and sustainability of the Chinese economy with heavily indebted businesses, Evergrande, and Country Garden, remaining immersed in complex negotiations with creditors.

Optimism

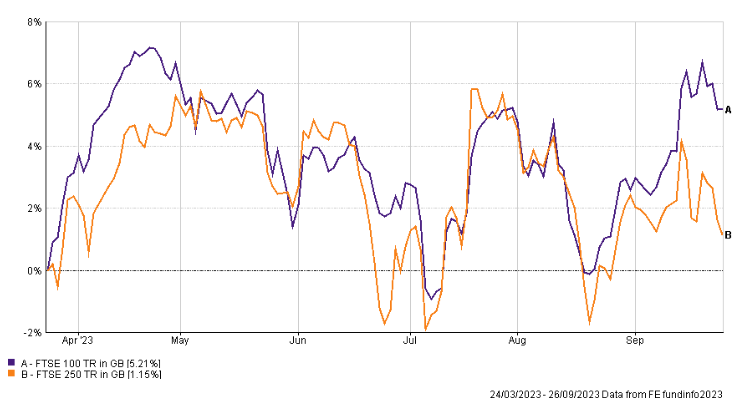

There are undoubtedly economic challenges for investors to navigate, but conditions are not uniformly bad. Returning to the UK, as to be expected, there has been an increase in profit warnings. But equally, many businesses continue to trade well. Retailers, JD Sports Fashion, Marks & Spencer and Next have demonstrated that consumers are still willing to spend, if the offering is appealing. Should employment levels remain historically high, and inflation returns to desired levels, consumer finances will begin to appear healthier. Whilst we must be mindful of the near-term risks, equally, it is important to remember that financial markets are priced off anticipated future conditions, rather than current events.