The March 2024 Spring Budget ignited many conversations about household finances. How would they be affected by the new measures – particularly the cut in National Insurance?

At Vesta Wealth, many clients in Cumbria have asked such questions and our financial planners wanted to offer some reflections to give readers more clarity and information.

We hope these insights are helpful. Please contact us for more information or to speak with a financial adviser:

t: 01228 210 137

e: [email protected]

What is happening in the economy?

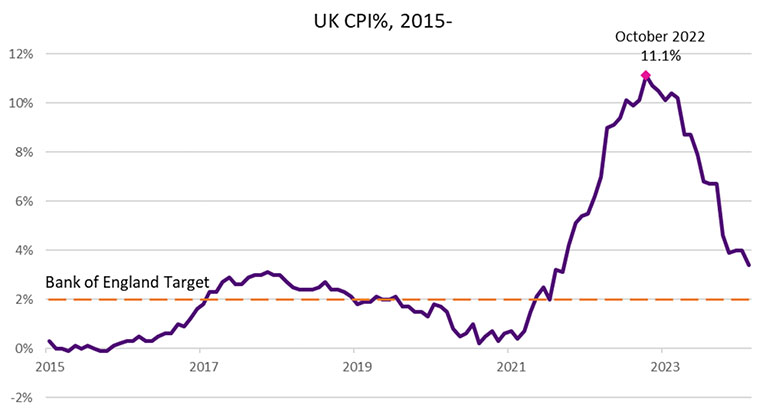

The Spring Budget mentioned the UK’s recent journey with inflation (the general rise in prices for goods and services). This reached a peak of 11.1% nearly a year and a half ago. More recently, it stood at 3.2% in March 2024.

This is still above the Bank of England (BoE) target of 2% inflation. The Bank’s forecasts however are optimistic that price rises may start coming under greater control later this year. With inflation continuing to fall, some analysts expect that rates could fall from 5.25% to 4% by the end of 2024.

While wages have risen, high inflation has eroded “real” household incomes since the same amount of income cannot buy the same amount of goods or services as 12 months ago. This is continuing to put pressure on UK living standards, which have recently experienced the biggest decline since Office for National Statistics (ONS) records began in the 1950s.

However, the Spring Budget was optimistic that real household disposable incomes would return to pre-pandemic levels by 2025-26 (next April). Public spending is expected to grow by 1% per year, in real terms, rather than following inflation (leaving room for cuts to public services).

What about my tax bill?

The headline measure from the 2024 Spring Budget was the planned cut to National Insurance (NI), now in effect from 6 April. Now, employees pay 8% rather than 10%. For a worker on £35,000 per year, this could save £450 in tax. The self-employed rate has also fallen to 6%.

Whilst this may sound like good news, bear in mind that income tax rates and thresholds have not been changed. Indeed, they may remain frozen until 2028. Many analysts have pointed out that this, in effect, amounts to a “stealth tax” on many workers.

As their earnings increase, many workers will find more of their income entering a higher tax bracket (often without realising). This is partly why UK tax revenue, as a share of GDP, is still expected to rise to its highest level since 1948 over the next four years (37.1%), despite the cut to NI in the Spring Budget.

Childcare, energy, and other matters

Until recently, the threshold earnings level at which Child Benefit started to be lost was £50,000. The Spring Budget confirmed an expansion of the threshold to £60,000 in April 2024, which will be welcome news to many parents.

The Chancellor also confirmed his childcare funding expansion plan pledge from last year, allowing many working parents of two-year-olds in England to now access 15 hours of ‘free’ childcare. This could allow tens of thousands of extra parents to re-enter the workforce.

There is also some good news on the energy front. On 1 April 2024, the energy price cap dropped by 12.3% for average use dual fuel customers, from £1,928 to £1,690. A further fall is predicted in July 2024.

Options for households in 2024

Taken together, these Spring Budget announcements and economic changes paint a complex picture for many households. Fortunately, a robust financial plan can help you optimise your position in this landscape – helping you progress towards your goals.

As always, a good starting point is to review your budget. Are you overpaying for the things you need (e.g. your mortgage), and are you paying needlessly for things you do not – such as unused subscriptions and memberships? Having a “financial cleanup” can free up more disposable income for other important purposes.

One of these includes your “emergency fund”, which financial planners often recommend building up to 3-6 months’ worth of your living costs. This helps you avoid turning to debt (e.g. credit cards) if you suddenly face a major expense, like property repair work.

Another key step is to review your tax plan – an often-overlooked strategy to put more hard-earned money back in your pocket. For instance, are you making the best use of your £20,000 annual ISA allowance (which lets you generate capital gains, dividends, and interest without tax)? Are you making full use of your allowances for earnings – e.g. the Marriage Allowance which allows a husband, wife or civil partner to transfer £1,260 of their Personal Allowance to the other person?

Invitation

If you would like to discuss your financial plan and investment strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

e: [email protected]

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.