The FTSE 100 shrugged off stickier inflation and geopolitical tensions in the Middle East to establish new record high levels in April. While a strong month for UK equities, global markets have faced a higher level of volatility. Much of this has been driven by changing expectations of central bank policy in response to recent inflation data.

Falling Inflation?

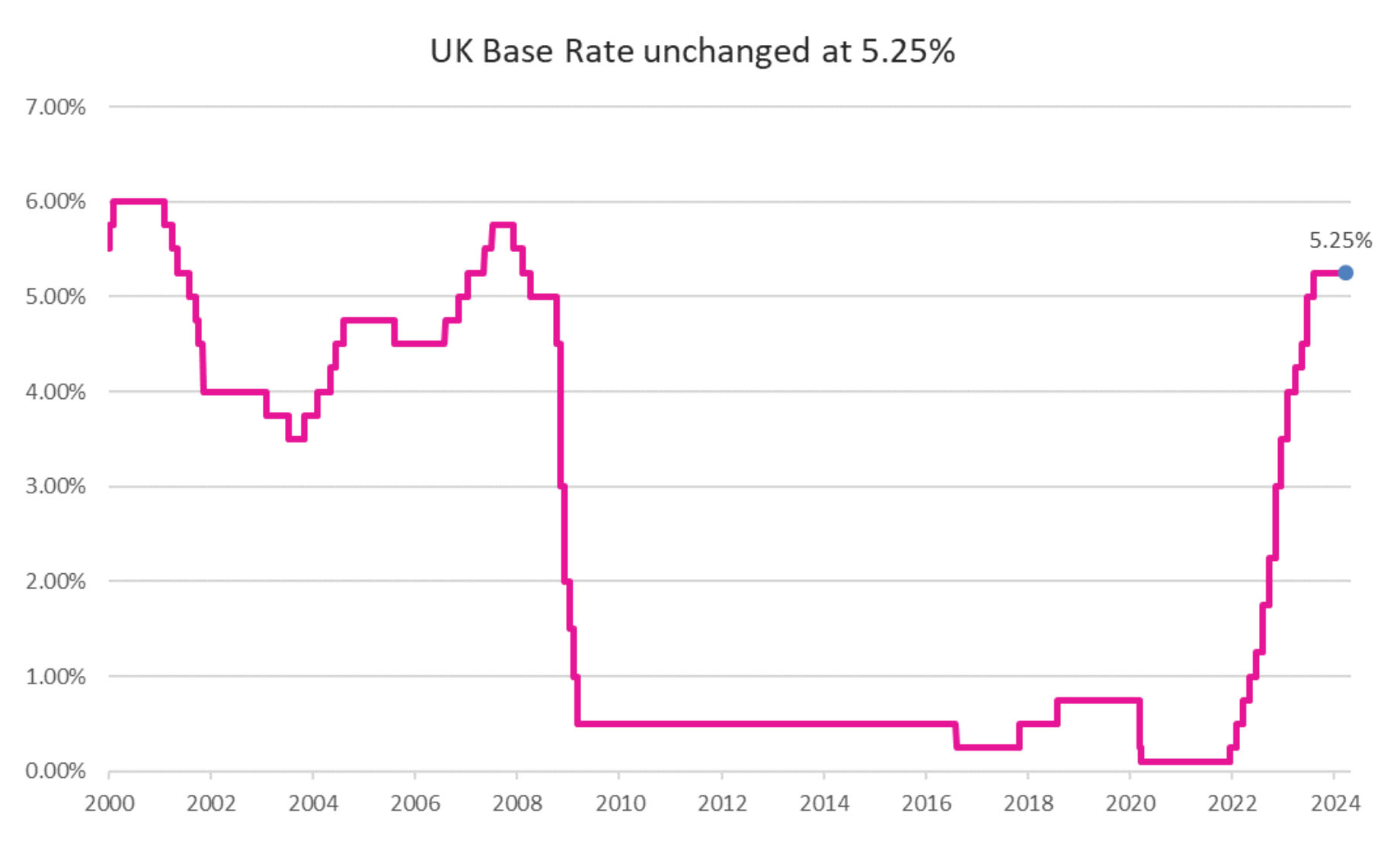

Inflation remains a key driver for investment market returns. At the start of 2024, investors were hopeful that the fight to control inflation had been won and that central banks would begin lowering interest rates. Despite this hope, none of the US Federal Reserve, European Central Bank, nor the Bank of England have yet made any cuts to interest rates.

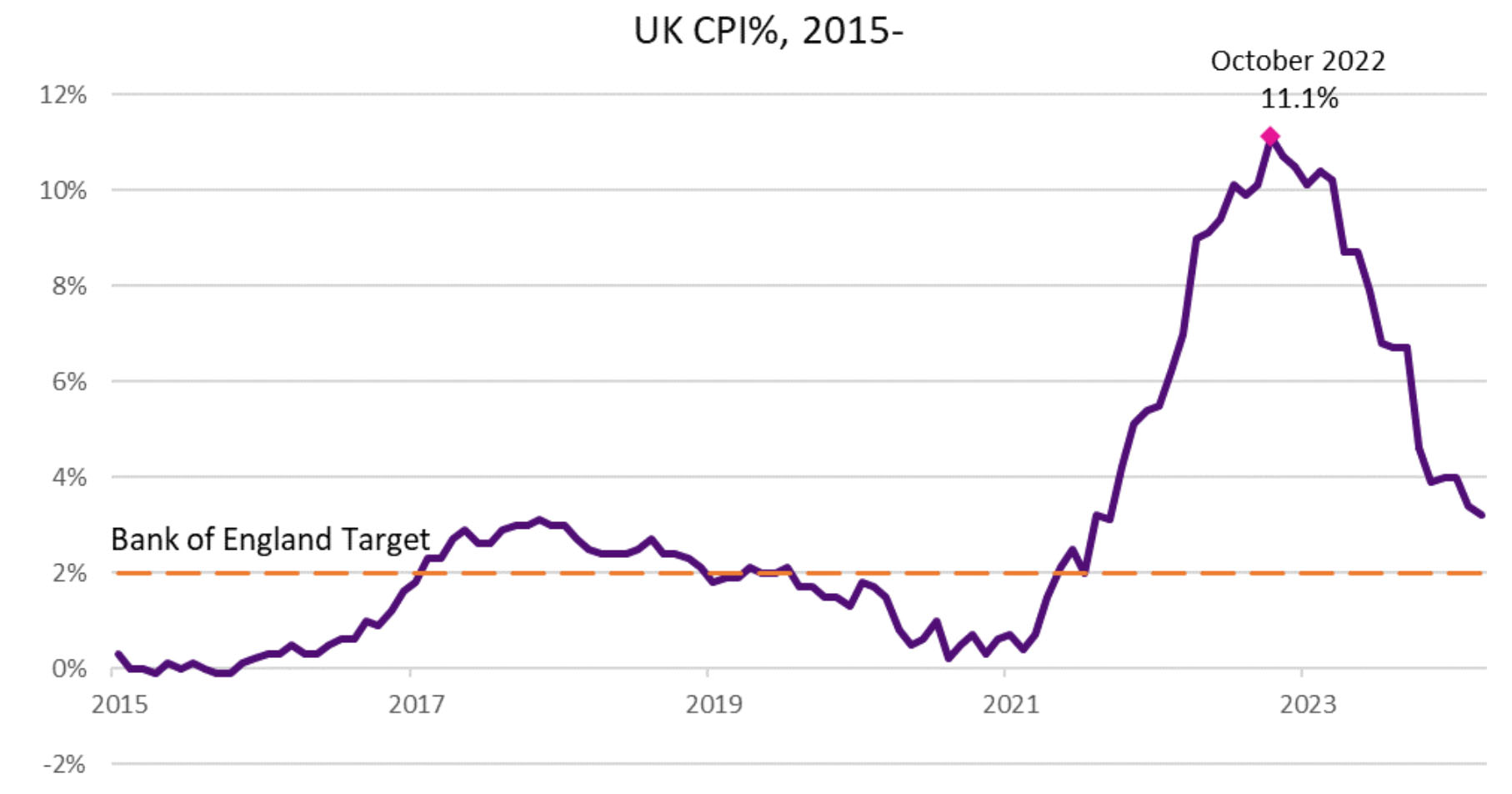

The debate on the timing of interest rate cuts remains fluid. Recent statements from the Bank of England suggest that any cuts are more likely to be later in the year than envisioned. The bank highlighted the fact that while inflation is falling, it remains above the target rate of 2.00%. Statements from other central banks suggest this focus on inflation returning to target is a common theme in their decisions on interest rate policy.

It is a positive story in the UK though as inflation continues to fall. The Consumer Prices Index (CPI) for March was recorded at 3.20%, down from 3.40% in February. Core CPI, which excludes energy, food, alcohol, and tobacco, fell from 4.50% to 4.20%.

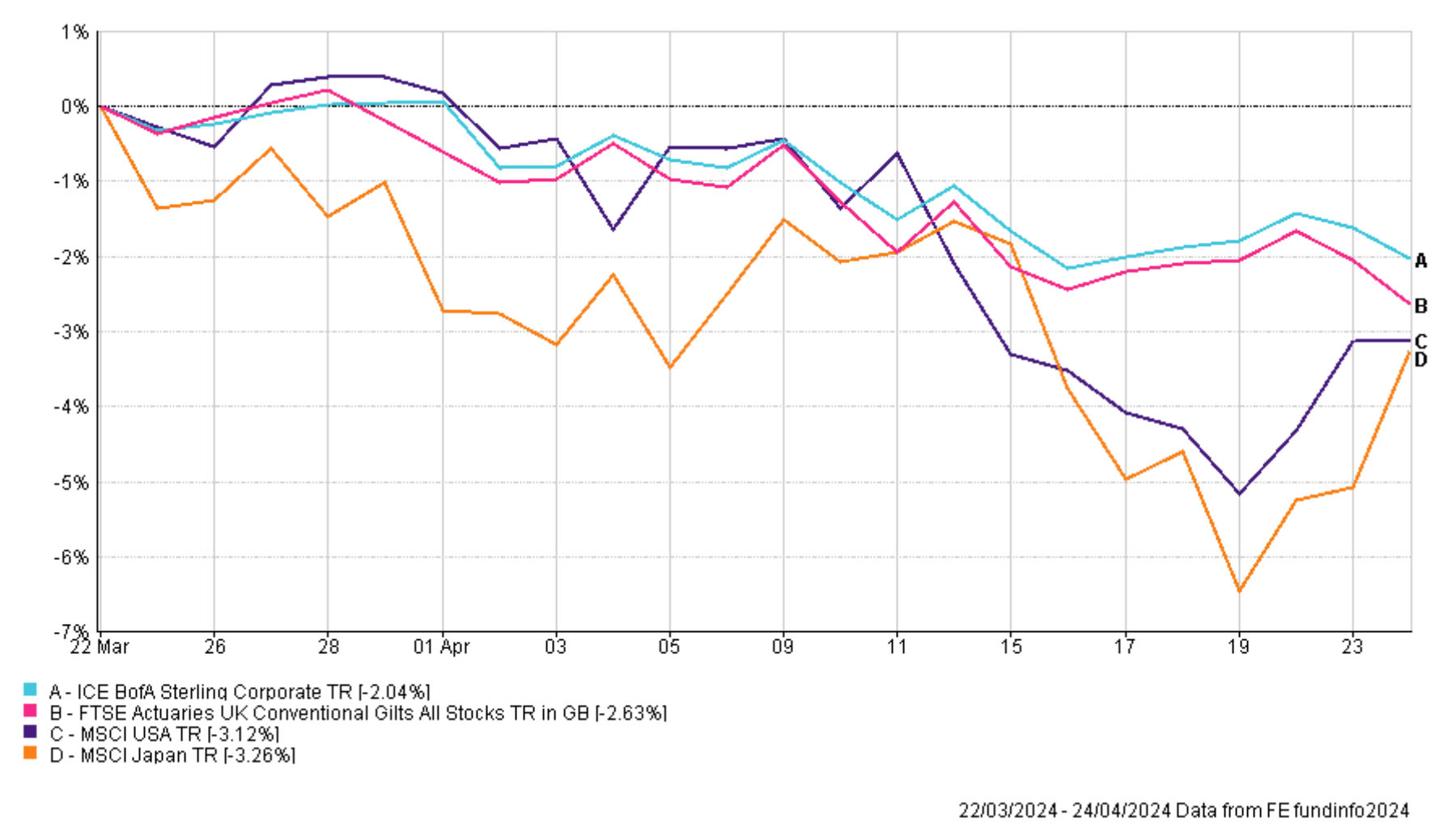

In more worrying news however, data in the US appears to show that inflation is starting to rise. This presents policymakers around the world with significant challenges. They do not want to cut interest rates too early when inflation is not under control as it could potentially create even higher levels of inflation.

With inflation appearing to be on the rise again in the US, this has prompted investors to adjust their expectations of when interest rates will start to fall. This can most clearly be seen within the bond markets, with yields rising to reflect the ‘higher for longer’ thoughts.

To varying levels, this change in expectations has also impacted equities. This is most notable in the US. Having enjoyed a strong start to the year, US stock market indexes faced a more difficult April as rising inflation created fears that the US Federal Reserve would not cut interest rates any time soon. Markets do not like uncertainty, and the greater uncertainty about the timing of interest rate cuts will continue to add an air of caution for investors.

UK Equity Success

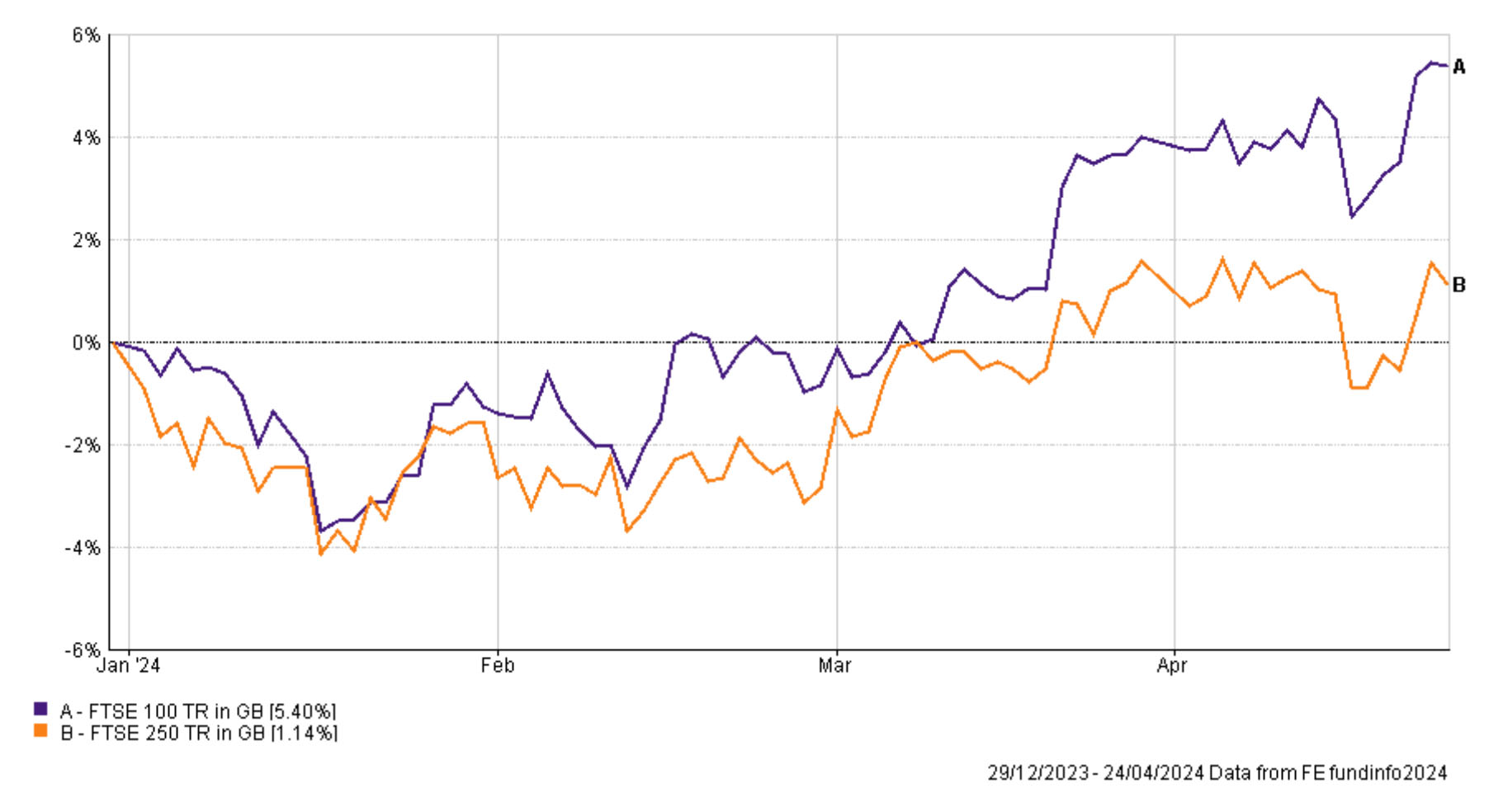

In contrast to the volatility that some equity markets have experienced in April, large cap UK equities have shown comparative resilience. As noted, the FTSE 100 enjoyed a strong month to establish new record highs. This is a boost for UK investors as UK equities have long been considered a laggard to their global peers.

One of the reasons for this strong performance is valuations. UK equities on a valuation basis are widely considered ‘cheap’ in comparison to developed market equivalents. With less pressure on their valuations, they are not as sensitive to the outlook of interest rates like other markets, such as the US.

Another factor is currency. With recent inflation data, it is expected that the Bank of England will cut interest rates before the US Federal Reserve. For investors, this decreases the attractiveness of pound sterling, and sterling has depreciated in value across April. While the FTSE 100 is a UK index, the majority of its constituent companies earn the majority of their revenues overseas. In fact, many FTSE 100 companies report their revenues in dollars. As pound sterling has weakened, these companies are worth more due to this currency conversion of these revenues and profits.

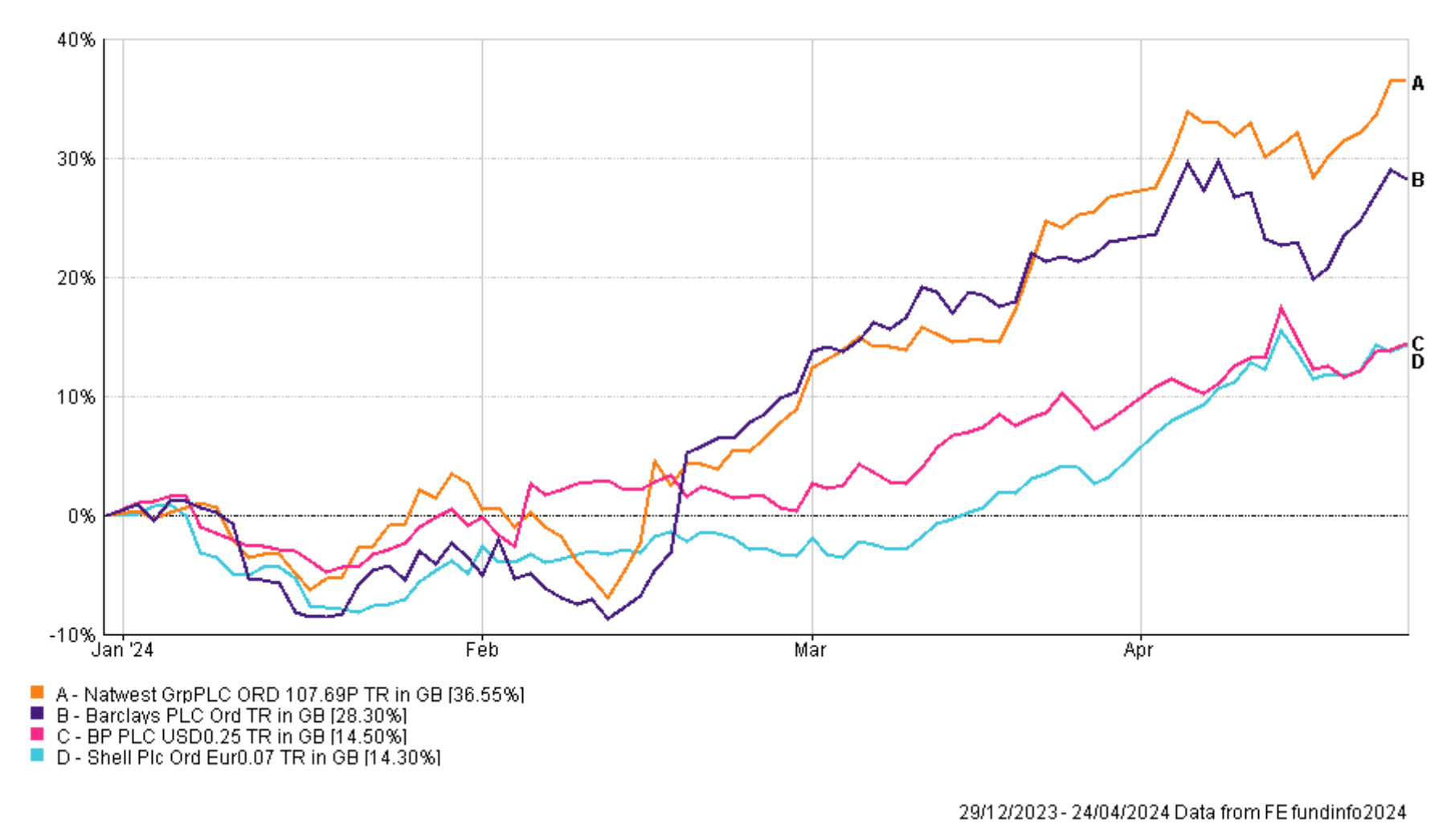

The companies which make up the FTSE 100 have also been delivering positive earnings reports. Banks such as Natwest and Barclays show respectable year to date gains. For oil companies, such as Shell and BP, rising oil prices in combination with a strengthening dollar also provided a boost to valuations.

The UK economy, while still struggling with low growth, is showing some positive signs moving forward. Employment levels are still high, and wage growth is outpacing inflation. In a boost for consumers, grocery inflation has returned to more benign levels and household energy bills have also fallen.

Despite breaking new ground, the FTSE 100 is still lagging leading European peer indexes. However, the relatively good value of UK equities, amid challenging valuations in leading behemoth global technology stocks, is causing retrospection amongst asset allocators.