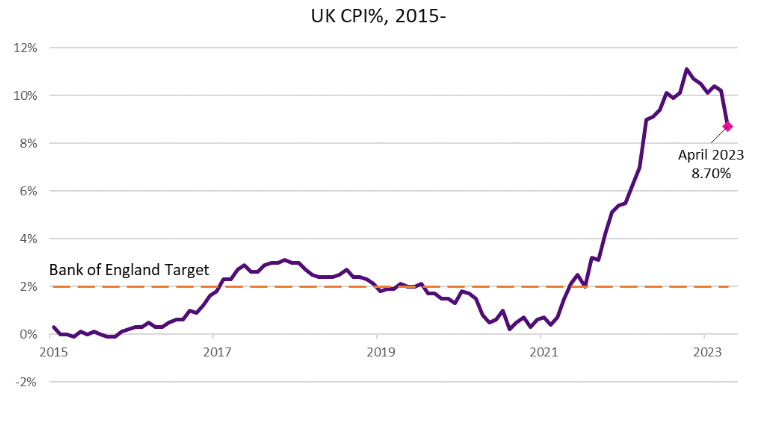

There were further signs that inflation may have peaked this month as UK CPI inflation was recorded at 8.70% in April, a marked decline compared to the 10.10% recorded in March. This represented the largest decline in annual inflation figures since 2021 when interest rates started to climb. While it is to be welcomed that inflation has fallen below the double-digit mark, investors were disappointed the headline figure exceeded consensus forecasts of 8.20% suggesting higher inflation remains in the system.

Food Prices

Part of the reason for the decline in the rate of inflation is the impact of energy prices and the relative effect of the energy price cap rise in April 2022. However it will come as no surprise to many households feeling the strains of cost-of-living increases, that food prices continue to be a key driver of inflationary rises, with the pace of inflation remaining at 45-year highs. The Office for National Statistics (ONS) recorded overall food prices rising by 19% in the year to April 2023.

To add further pressure on households, much of this rise is due to increased prices on staple items. For example, rice, flour, pasta, eggs, and fruit, were all subject to increases exceeding the headline figure. This has led to calls for a closer look at the food supply chain, with citations of ‘greedflation’ as food producers stand accused of raising prices further than necessary under the excuse of increased costs.

Battling inflation

With CPI falling below 10%, the focus will shift to the pace of decline, as the Bank of England works to restore it to the target level of 2%. This is a significant challenge given the second-round effects of inflation, such as wage increases. Private sector pay growth averaged 7%, with the public sector at 5.60%, annualised, in the period between January and March this year. Despite previous unwelcome comments from officials, this is understandable, as employees seek to protect their standard of living, amid budgetary pressures.

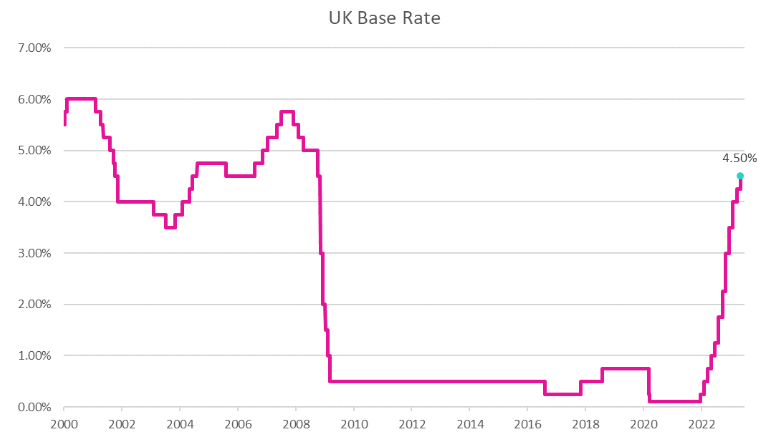

The Bank of England raised interest rates by a further 0.25% to 4.50%, earlier in the month, a 12th consecutive increase. This followed similar moves by the Federal Reserve and European Central Bank. The Bank noted that inflation is expected to stay higher for longer and remain above the 2% target level until after the next election, which must be called before the end of 2024. This was accompanied by a more upbeat assessment of the economy, noting stronger-than-expected consumer expenditure, and rising business confidence, with the UK expected to avoid a recession, as growth forecasts are upgraded.

The housing market has also been more resilient than previously forecast. An element of caution is required, as forecasting amid a succession of interest rate increases is challenging, due to the delayed impact of said actions, which can take 9 months or more to have any effect. The impact will be felt by millions of homeowners, who fall off fixed-rate mortgages and face more expensive refinancing or move onto variable-rate mortgages. To counter these pressures, household energy bills are expected to fall from the summer.

Debt Ceiling

One area of potential concern currently for investors, particularly in the US, is the protracted discussions over the US ‘debt ceiling’. In simple terms, the ‘debt ceiling’ places a limit on the total amount of government debt the US can legally have. Without ‘raising’ the debt ceiling, estimates suggest that the government could run out of money by the beginning of June 2023, risking a debt default, which could be greatly damaging to both the domestic and global economy.

However, this is not expected to happen. History has shown that beyond partisan brinkmanship, compromises are found. However, as time passes without a deal, the chance of a compromise not happening increases. Financial markets do not like uncertainty and a question of ‘might’ has resulted in markets becoming more nervous.

Raising the debt ceiling is necessary to facilitate expenditure that has previously been approved. Treasury Secretary, Janet Yellen, forecasted that a debt default in early June ‘” is highly likely” without a deal, which places a great obligation on the talks between the Republican House of Representatives Speaker, Kevin McCarthy and the Democrat President, Joe Biden. The issue is therefore a political one. It is hoped that despite differences, both parties will ultimately put country first. The performance of US stock markets in recent months has been positive for investors as, despite these concerns, an improving economic outlook and better-than-expected company reports have boosted forecasts.

These acts of high-stakes political theatre serve as a reminder that governments around the world face challenges to live within their means. This can also be seen closer to home, with UK borrowing for April 2023 increasing to £25.60bn, swelled, by amongst other things, rising debt costs. Issuing long-dated, inflation-linked debt, appeared compelling when price rises were benign, but has become uncomfortably expensive as inflation soared. This has made it difficult for the government to boost the economy via tax cuts, as the need to maintain fiscal credibility is paramount.

It has been a challenging year to date for fixed-income investors as rising interest rates and yields have had a negative impact on the capital values of bonds. The ten-year gilt yield has risen above 4%, with the 30-year yield exceeding 4.50%. On a brighter note, fixed income investors can now access competitive yields.