For most people in the UK, pensions will form the backbone of their retirement income. Taking time to plan ahead will help ensure financial stability and comfort in later life – helping you achieve your long-term goals.

Below, our Stockton financial planners offer 4 ideas to help people maximise their pension income. We hope this content is useful. Please contact us for more information or to speak with a financial adviser about your personal goals and needs:

t: 01228 210 137

e: [email protected]

#1 Build the best State Pension

In the 2023-24 tax year, the full new State Pension now offers £203.85 per week (£10,600.20) following a 10% increase in April. Given that someone in retirement may need around £20,000 per year just to cover essential living costs, the State Pension is likely to be a vital income stream for most people in retirement.

Your future State Pension income is largely based on your National Insurance (NI) record. Those with at least 35 full “qualifying years” under their belts should receive the full new State Pension in the future (unless the rules change, of course!).

Consider speaking with a financial adviser about how to maximise your State Pension. Depending on your situation, you may be on course to build up the remainder of your 35 qualifying years simply by continuing in your employment. Others may need to consider voluntary NI contributions.

#2 Start early with your pension

Your State Pension is not the only type of pension available to workers. Under the auto enrolment rules, employees are now automatically opted into a workplace pension scheme. In 2023-24, an employee must contribute at least 3% of his/her salary. Their employer must put in at least 5% (for a total of 8%).

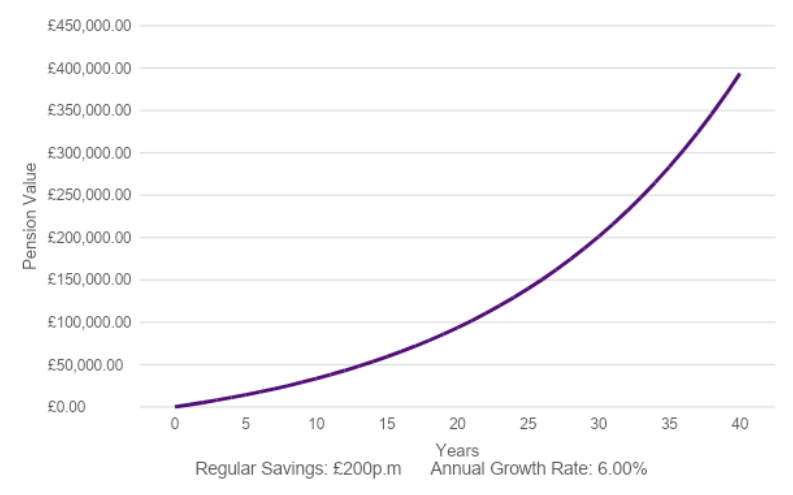

The earlier you start contributing to a pension the better. This is because the investments in your pension have more time to grow using the power of compound interest. For instance, suppose you and your employer contribute £200 per month and you make a 6% average investment return each year.

By year 20, your pension fund could contain over £92,000 inside. However, if the period is extended to 30 years, the fund could hold over £200,000.

Do not worry if you are further along in your career and worry that you have left it too late to start saving towards your retirement. It is rarely too late to take positive steps in the right direction. Seek professional advice to explore your options.

#3 Review and optimise your investments

Perhaps you already have a portfolio in your pension which is slowly building wealth for retirement. If so, are your investments working as hard for you as they could?

In some cases, an individual may not have the appropriate investment strategy in place to progress effectively towards their goals.

For instance, someone early in their career (e.g. a 25-year-old) may not be suited for a “cautious” strategy which is mostly invested in bonds. Given the long investment horizon before them, it may be better to concentrate the portfolio more towards shares, which could offer higher potential returns over time (albeit at higher risk).

Someone nearing retirement, conversely, may wish to start “de-risking” their portfolio to protect the retirement savings they have already accumulated.

Another area to consider is fees. The funds offered by various pension schemes (e.g. certain workplace pensions) may be quite expensive relative to other funds on the market. They may also offer fewer investment options.

A financial adviser can help you “look under the hood” of your pension scheme(s) and identify other possibilities in the pension marketplace which you may wish to consider.

#4 Explore different pension income options

Broadly speaking, there are two main routes for taking an income from a pension. You can keep your pension money invested and make gradual withdrawals (income drawdown). Or, you can use some/all of your funds to buy an annuity – a product which provides a retirement income.

Different people might opt for the first, the second or a combination of the two, depending on their needs, goals and circumstances. Sometimes, shifting market or economic conditions can change the calculation when determining which route is best for you.

In 2023, for instance, interest rates have risen sharply – now standing at 5.00% (the highest since the 2008-9 financial crisis). This has caused the annuity market to improve to a 14-year high. For some people who previously were unsure about an annuity, now could be a good time to re-explore the different options for their pension with an adviser.

With this said, annuities are not right for everyone. Whilst they can provide a lot of stability and predictability for your retirement income, they are also more inflexible than income drawdown. If you later regret buying an annuity, you cannot “return” it. So you must be sure that it is the right decision before proceeding. Speaking to an adviser can help you consider your options and ensure your income needs are met throughout your retirement.

Invitation

If you would like to discuss your financial plan and retirement strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

e: [email protected]

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.