While the delta variant continues to be a recognised threat to the global economic recovery, the cumulative impact of Covid-19 on supply chains has assumed prominence. The impact on the supply of key labour and materials is evident globally, both in the context of cost and availability. This has raised fear of the unpalatable combination of stagnating growth and inflation, commonly termed, stagflation.

Inflation in the major economies of the world is trending above the targets of respective central banks, while growth is also losing momentum.

In the UK, the Bank of England is now forecasting inflation to rise to over 4% in Q4 2021. The situation is fast moving, with stories breaking of reduced deliveries of fuel and food owing to a shortage of lorry drivers, due to amongst other factors, the closure of DVSA centres during the lockdown periods.

Energy

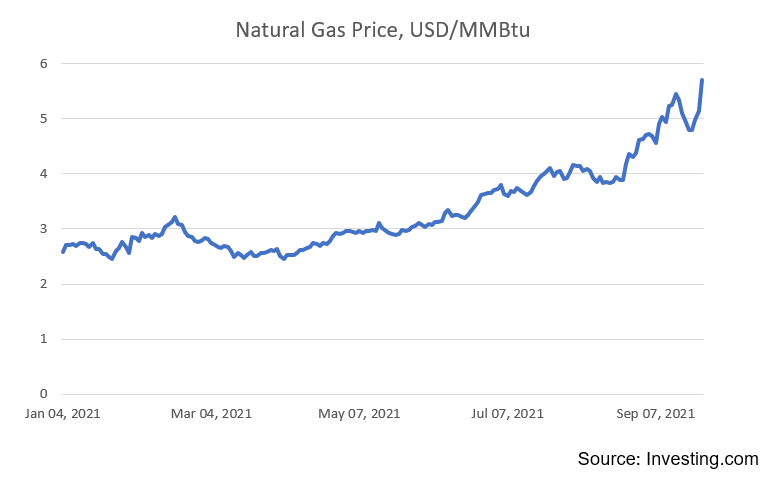

Energy is another area of concern, with a lack of gas storage capacity, and lower output from renewables, sending prices soaring.

Source: Investing.com

Central Bank support and interest rates

The UK is not alone in witnessing supply side disruption; Central Bankers are facing a difficult balance between wishing to support the economic recovery with exceptionally low interest rates and asset purchasing programmes, while also being mindful of not letting above target inflation threaten their credibility.

The Federal Reserve, the European Central Bank and the Bank of England have all spoken about moderating asset purchases, but do not appear in a hurry to raise interest rates. Market participants will be watching this stance closely. On this note, government bond yields have started to move higher, albeit from still low levels.

There are political aspects too. As we move into the winter months, and Covid-19 support measures begin to run their course, populations will likely feel a strain on their cost of living.

China

It is important to remember that the low interest rate environment that has been in place since the global financial crisis, also comes with risk. Two such risks are asset price inflation and speculation.

The heavily indebted, and financially distressed Chinese property conglomerate, Evergrande, is a poignant example. The embattled business, with outstanding liabilities of around $300bn, faces a series of bond interest payments in the coming weeks, with a default thought likely. With any large default, attention focuses to the matter of contagion.

Xi Jinping has spoken disapprovingly of speculation in the property market, but the Chinese will be keen to contain any damage arising from a series of defaults.

Authorities in China have successfully navigated both global and regional financial turbulence in recent decades, with structure of government affording them near unfettered control over all aspects of the economy and society. That said, an abundance of cheap finance has fuelled global property prices, and investors will be monitoring to what extent the woes of Evergrande herald a turning point for the asset class.

USA

Over in the US, President Biden wishes to move the focus back to his domestic agenda, by passing ambitious spending programmes. Unfortunately, these ambitions have coincided with the federal government reaching its debt ceiling.

Failure to negotiate an increase in the debt ceiling by the end of September 2021 will result in a government shutdown, with crucial payments, including social transfers, being frozen. This situation is not unique and has in recent years been typified by political brinkmanship between the Republican and Democratic Parties. However, on this occasion, the Biden Administration enters negotiations short on political capital, following the troublesome withdrawal from Afghanistan.

Against such an indifferent backdrop, risk assets have struggled to make progress throughout September. In keeping with the prior month, rising inflation concerns have reinforced the valuation of assets with index-linked protection such as property. In equity markets, companies that emerged from the Covid-19 lockdown in good financial shape have continued to report healthy results.

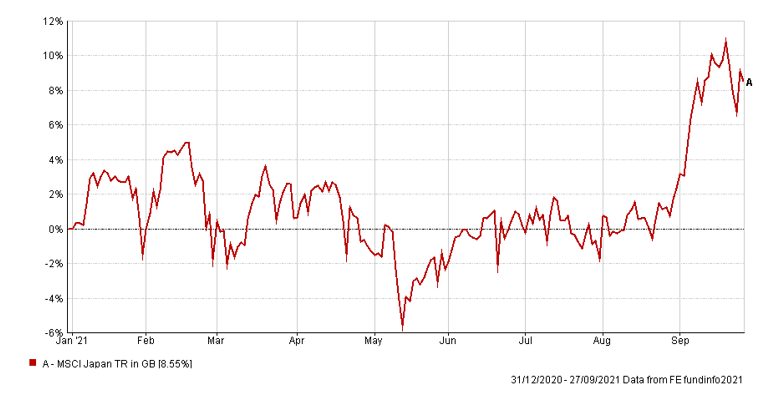

Japan

Japan has been the strongest performing equity market in September having booked further gains following the resignation of Prime Minister Suga. Having been initially received positively by investors at the start of his term, declining public support has damaged his reputation significantly due to his Covid-19 response which has been seen as a failure by many in the country. His resignation offers the opportunity for a fresh start for the country, which relatively has fared better than most during the pandemic, and investors have been keen to support this.

Issues that have received large degrees of press coverage such as price rises in the energy market, and driver shortages in the haulage industry, have created volatility in markets even as the economy begins to move on from covid and return to more normal levels of activity. Even so, investment markets have remained resilient, and many indexes remain at, or near, all-time highs. However, with volatility remaining high it is important to ensure that your investment portfolio remains suitably diversified. This allows your investments to take advantage of any opportunities that arise while protecting the value of your investment against any downturn.

Invitation

If you would like to discuss your financial plan and investment strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.