It has been a difficult month for investment markets since our previous update. Russia’s invasion of Ukraine and the ongoing conflict has introduced a great deal of uncertainty for markets. This is both in the near-term with how sanctions and conflict impact on trade and investment. But also, in how the conflict might be resolved and what this resolution might mean for economies and markets around the world.

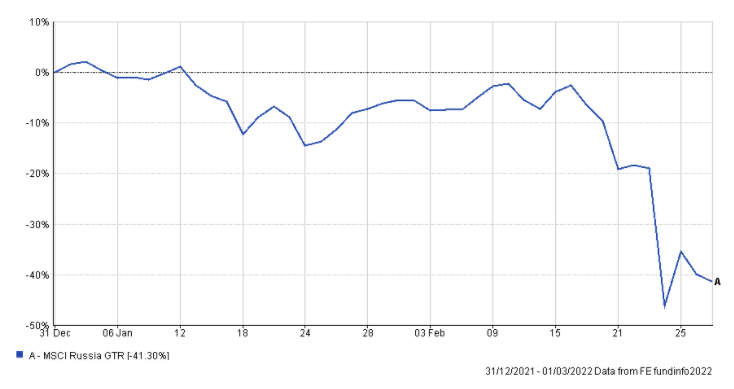

The initial market reaction to President Putin’s decision to invade Ukraine on 24th February was perhaps understandably negative. War is an inherently uncertain timeline and markets do not like uncertainty. The biggest impact was felt in markets directly exposed to the conflict, with Russia being the biggest loser following the immediate imposition of severe sanctions on the country and its high-profile citizens.

On the day of the invasion Russian stock markets lost over 33% of their value. In an effort to protect the Russian stock market from further declines, the Russian central bank suspended trading on the market and it has remained closed since the end of February. Russia’s currency, the Rouble, also came under pressure as a result of sanctions and the uncertainty of the conflict saw its value fall to record lows. As a result of sanctions on foreign currency reserves, there is a risk that Russia will default on its debt. This is an area of concern for investors, but it is hoped it will not decrease confidence in other debt markets.

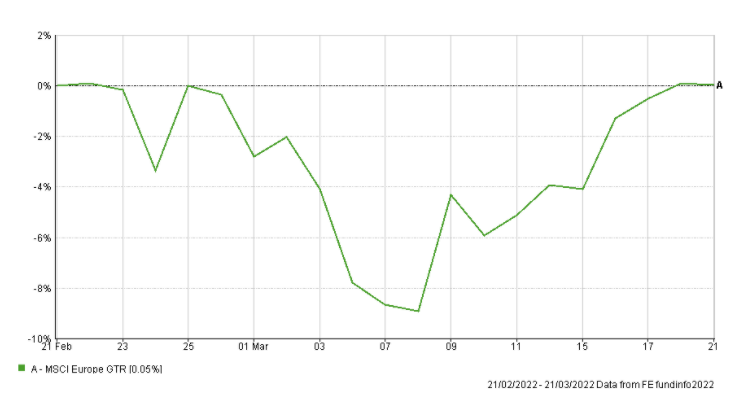

European markets have been volatile following the invasion due to its proximity to the conflict and its greater reliance on Russian supplies of commodities, chiefly energy. The impact of sanctions on trade in the region and the uncertainty resulting from the conflict saw broad European indexes fall nearly 10% in value in the weeks following the invasion. Since then, however markets have recovered strongly following greater optimism that a resolution can be found to the conflict which would ease pressures in the region.

Inflation, Inflation, Inflation

The big concern for investment markets before the invasion was inflation. More specifically what central banks would do to combat it. Markets had performed strongly since the start of the pandemic thanks to supportive central bank policy however have faced greater headwinds since November when these policies started to be unwound in a bid to control inflation.

This broad theme is still the dominant factor for investment markets with the crisis in Ukraine exacerbating troubles. Impacted supply chains are being further impacted and the effects this is having on for example oil prices are clear to see with record fuel prices on UK forecourts. The added inflationary pressures as a result of the invasion have increased fears that heightened inflation could be a more sustained problem than expected with prices being driven even higher.

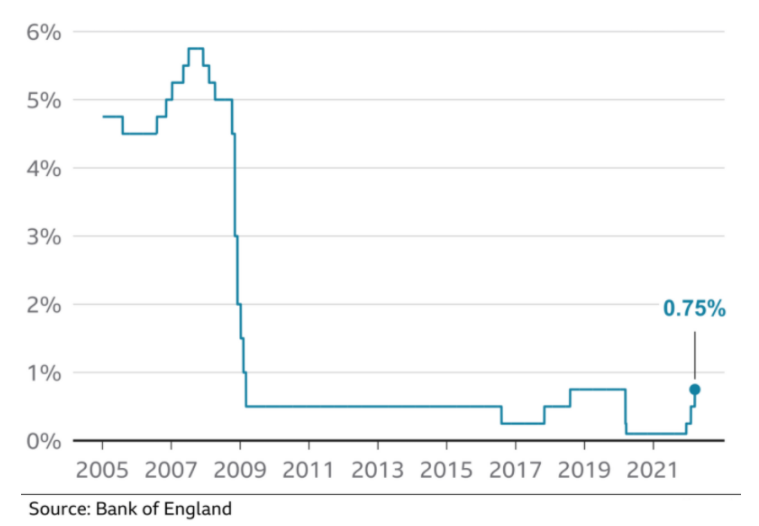

It was no surprise to anyone in March then that the Federal Reserve raised US base rates for the first time since 2018 while the Bank of England raised rates for a 3rd time in 4 months. These moves had been clearly signalled ahead of both meetings. What perhaps was surprising to markets was the differing rhetoric from both groups accompanying the respective rises. The Federal Reserve took a very hawkish stance signalling further rate rises are to be expected at all other remaining meetings this year. In contrast, the Bank of England appeared to move away from comments previously suggesting further rate rises were “likely” leading to a minor fall in future inflation expectations.

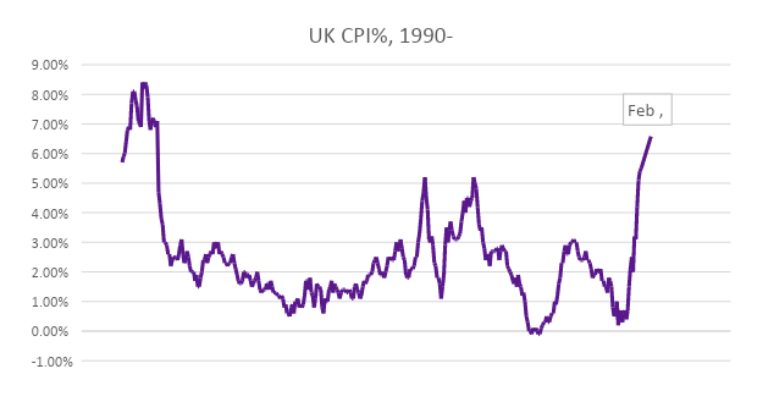

Where the situation in Ukraine could cause more longer-term concern for investment markets is the impact that sanctions, and the impacted supply chains, could have on global trade. A negative outcome to this would be reduced economic growth which would cause a dilemma for central banks. Do they remove supportive policies to attempt to combat inflation? Or do they maintain them to support potentially disrupted economies while letting inflation run hot? With inflation in the UK reaching a 30 year high in February, even before the energy price cap rises, the Bank of England will have this dilemma to consider.

Covid

Covid, two years on since the UK entered its first lockdown had moved to the back of investors’ minds as cases were falling and restrictions were being lifted. It has however been pushed back to the fore by a resurgence of the virus in China. Several areas of the country have been placed into lockdown creating uncertainty within investment markets given the potential impact to the level of demand in the global economy, alongside further potential impacts to supply chains. Chinese equity markets had been under pressure even before this current wave of the virus; however, they have received a boost in recent weeks following commitment by the Chinese government to resume economic stimulus to boost the ailing economy.

The events of the past month, and the uncertainty surrounding these issues highlights the importance of diversification within investment portfolios. A portfolio wholly invested in assets exposed to Russia and eastern Europe would have seen its value fall significantly in recent weeks. But by investing in a wide range of assets, portfolios can be protected from the severest bouts of market volatility. Here at Vesta Wealth, we ensure all our clients’ portfolios are suitably diversified to ensure they avoid excessive exposure to any one source of risk.

Invitation

If you would like to discuss your financial plan and investment strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

e: [email protected]

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.