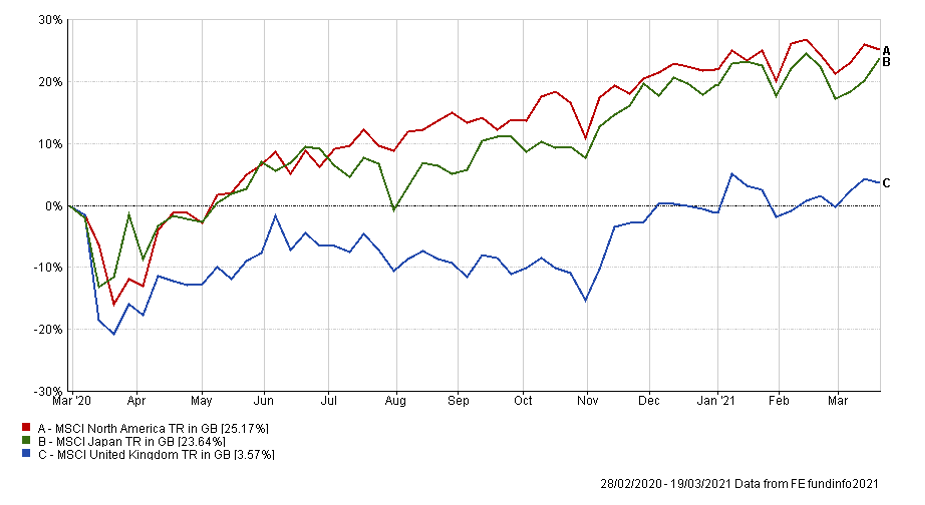

Markets have enjoyed a strong summer. With economies continuing to open up and a relatively slow news cycle, the global backdrop for equities remains supportive and optimism has been rising. Many stock market indexes, notably in the US and Europe, have recorded new all-time highs. The UK’s main index, the FTSE 100, however has trended largely sideways being impacted by a strengthening US dollar following comments made by the US Fed regarding monetary policy.

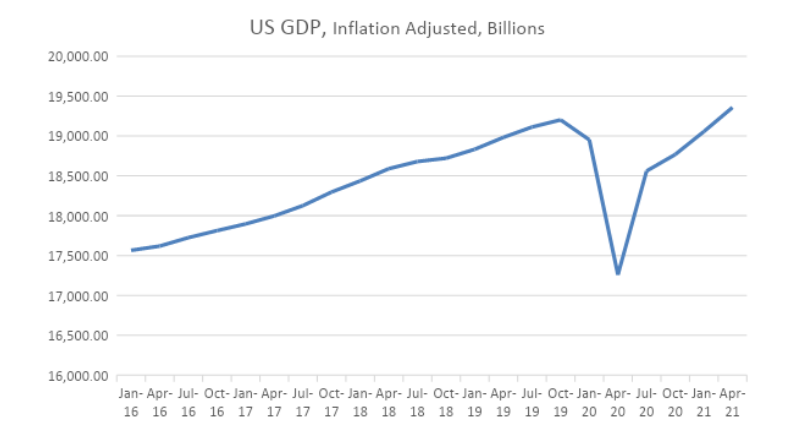

Inflation, the bogeyman for markets at the beginning of the year, was brought into sharp focus once again following the most recent meeting of the US Federal Reserve Open Market Committee. Responsible for the setting and management of monetary policy within the US, they indicated supportive monetary policy measures may be reduced earlier than planned. These programmes had been introduced to boost the economy while it was shut down and economic activity had ground to a halt. While the UK economy has not quite recovered to its pre-covid level, the US has already reached that point.

Source: Federal Reserve Bank of St. Louis

With economic activity continuing to resume even further, the Federal Reserve has indicated that these support programmes can begin to be withdrawn, as they are simply not needed in such quantity anymore and otherwise it might risk overheating the fragile economy. As we have written in recent months, part of the reason for the speed of recovery of financial markets from the post covid lows has been this copious support from central banks. Comments about their removal sparked volatility in markets, as investors weighed the sustainability of stock market valuations.

Vaccines vs variants

Covid continues to play a role in markets with the extra virulence of the Delta variant causing a threat to the global economic recovery. The extent of this threat varies, as case numbers and vaccination rates vary from country to country. In addition, there is no uniform strategy for containing the spread of the virus with some countries like Australia and New Zealand heavily locking down while others like the UK are happy to let the virus spread.

The delayed 2020 Tokyo Olympics were a muted success without the atmosphere of a global audience. However, the event was overshadowed by rising case numbers that will have a greater impact on the upcoming Paralympics. Japan can be seen as an example of covid impacting markets with the Olympics only able to provide a small boost to sentiment.

It remains the hope that increased vaccination rates will serve to allow economic activity to continue a trend to normality. Early signs are positive that the vaccines are working to break the link between cases and hospitalisations, but the situation is finely balanced. The risk remains that new variants will emerge and present new challenges as we move into autumn and winter months. Any reasons for questions to arise over the efficacy of the vaccines against new variants could temper optimism surrounding a return to normal and lead to increased volatility in markets.

China’s tech crackdown

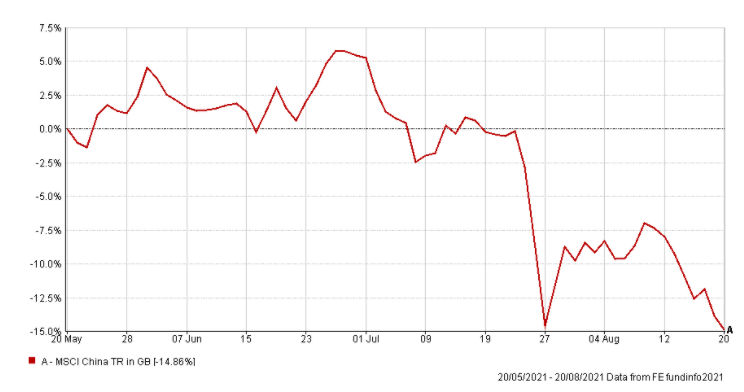

Chinese equities have faced a difficult quarter as authorities in the country have moved to clamp down on the oligopolistic practices of leading technology businesses, while also paying close attention to gaming and private education companies. Xi Jinping has been keen to emphasise that the crackdowns are motivated by a desire to promote the welfare of society and the consumer. However, what is more concerning for markets is whether the true motivation for these moves is a desire to reassert an iron grip on society and its resources. The uncertainty of this answer has led to a sharp fall in valuations of Chinese companies as investors digest the news.

Afghanistan and the world beyond covid

Since the beginning of the pandemic, markets and the news cycle have been dominated by the virus. With countries focused on fighting the pandemic, they have been less concerned with fighting amongst themselves and each other. While the tragic human story in Afghanistan has diverted the gaze of the media, investment markets appear to be unconcerned by the events and in the near term it is an event that is unlikely to massively impact portfolio values on its own.

The decision of the US to stage a withdrawal from Afghanistan is not new, with plans developed during the Presidency of Donald Trump. However, it could have ramifications if the situation provides a catalyst for geopolitical issues to become the focus once again as the world begins to move on from the virus. The tragic circumstances of the US withdrawal has been seen as weakness for the US and President Biden. It will be important to observe the response of China, Iran, and Russia, who may feel more confident in challenging US supremacy while Biden seeks to secure his own domestic legacy.

Without the pandemic to fight, attention will begin to focus on other areas. As the world moves on from one crisis, it might not be long before it walks headfirst into another. Markets will react accordingly, but this further demonstrates the importance of remaining in a suitably diversified portfolio. To protect against any downturn within markets and take advantage of opportunities when they arise.

Invitation

If you would like to discuss your financial plan and investment strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.