Equity and fixed-income markets experienced some selling pressure over the month as investors mulled the impact of stickier inflation and softer economic data.

Inflation Inflation Inflation

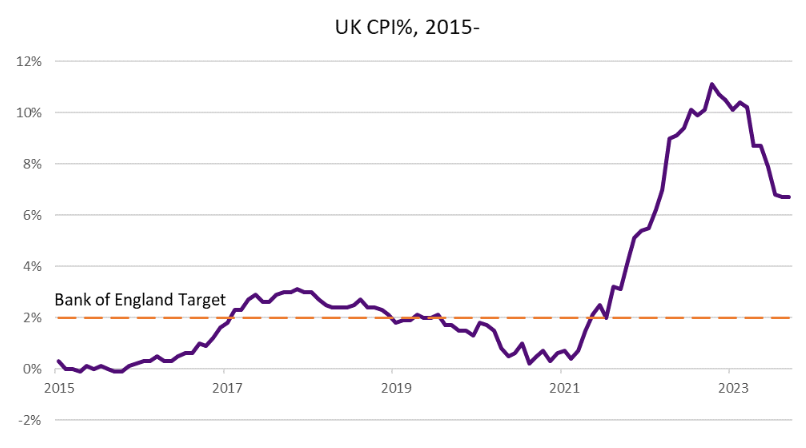

The UK Consumer Price Index (CPI) reading for September was unchanged on the August measure of 6.70%. Market participants had been anticipating a modest decline in the pace of price rises as witnessed in previous months. Downward pressure from food and non-alcoholic beverages, where prices fell over the month for the first such occasion since September 2021, was offset by higher motor fuel costs. The latter being a function of a higher oil price and a modestly weaker sterling. The core inflation reading, which excludes the more volatile inputs of energy, food, alcohol, and tobacco, fell slightly from 6.20% to 6.10%.

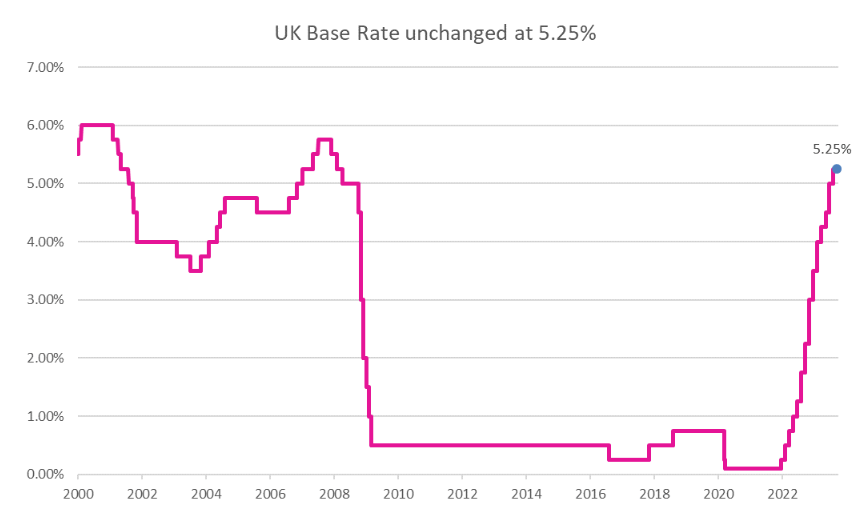

As central banks continue to attempt to combat inflation, the Bank of England’s (BoE) Monetary Policy Committee, who decides on interest rate changes, narrowly voted at their last meeting to pause a run of 14 consecutive rate rises which began at the end of 2021. This pause has led investors to believe that interest rates may have reached, or at least might be nearing, their peak.

While interest rates may be nearing their peak, market expectations are that they may remain at this elevated level for longer. This is in contrast to initial hopes they may fall as quickly as they have risen. The BoE have been keen to stress however that further work may be required to restore inflation to the target level of 2% meaning interest rates could rise higher. The next interest rate decision by the BoE, scheduled for early November, will attract much attention. Central banks continue to tread a fine line between combatting inflation, while being mindful of the potential impact on the economy.

The name’s bond, bond yields

One impact of rising interest rates, and the growing assumption of them staying higher for longer, has been rising bond yields. Key bond readings reached multi-year highs in September. Most notably, the 30-year gilt yield breached 5%, for the first time in over a decade. This has continued to have an impact on deemed ‘low-risk’ investments as the capital values of bonds and fixed-interest securities are inversely correlated to interest rates. In simple terms, as interest rates have risen, the value of ‘low-risk’ fixed-income investments has fallen.

Another impact of higher interest rates is that borrowing is now more expensive; higher financing costs have prompted areas of weakness in the economy. One area this is particularly notable in is declining house prices as reported in data provided by Halifax and Nationwide.

Mortgage affordability remains the key drag as increased mortgage costs have seen buyers needing to adjust their expectations. In other areas of the economy, data from the Office for National Statistics pointed to a decline in retail sales volumes of 0.90% in September. This was seen as a result of consumers trimming non-essential spending, with milder weather also proving unhelpful. Meanwhile, in the jobs market, vacancy levels are falling suggesting a decline in business confidence.

Despite lingering inflationary pressures and a long succession of interest rate increases, the UK economy has thus far avoided a recession. However, the extent to which this trend can continue is less certain.

On a positive note

The UK mid and smaller companies’ indices have notably trailed the FTSE 100 in the year to date. While this is unsurprising in a challenging economic environment, low valuations have attracted takeover interest. Recent examples have involved consumer facing businesses. Carpet and upholstery store ‘SCS’ were bought by an Italian furniture group. ‘Restaurant Group’, owner of brands such as Wagamama and Chiquito, has been the interest of multiple takeover bids. While investors must be alive to the risks of profits warnings, so they should not be blind to areas of value.

The US economy, a standout bright spot in the developed world, faces similar challenges to the UK. Inflation, while notably lower, has also exhibited some stubbornness. The September CPI reading in the US came in above expectations at 3.70%. This, along with buoyant labour market conditions, unsettled both equity and bond investors. The 10-year treasury yield reached its highest level since 2007, while the 30-year mortgage rate touched 8%. The 30-year mortgage rate is a key barometer for the US real estate market, where long-term fixed rates are a common feature. The US Federal Reserve meets to set interest rates on 31st October, with the decision communicated the following day.

There was optimistic news on the Chinese economy, with third quarter gross domestic product (GDP), growing by 4.90% year on year. Growth was helped by healthy consumption and industrial activity in September. However, the property sector continued to be a source of weakness. Property investment fell by 9.10% in the first nine months of 2023. At the time of writing, the leading Chinese equity indices were in negative territory on a year-to-date measure, with losses in Hong Kong being particularly pronounced.