Political events took centre stage in May. The decision by UK Prime Minister, Rishi Sunak, to call a general election on 4th July 2024 was a surprise to both financial markets and political analysts. Wider expectations had been set on a date in the autumn period. For investor portfolios, the news has barely registered an impact with markets more closely focused still on inflation and the future path of interest rates.

Prompted by Inflation?

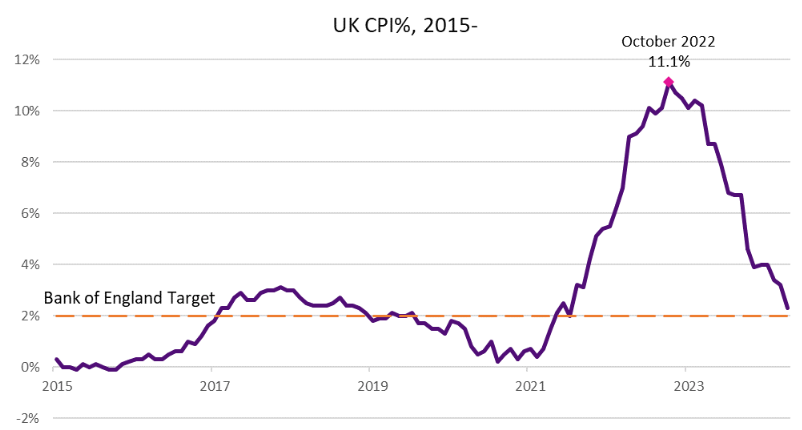

Sunak moved to seek permission from King Charles to dissolve parliament shortly after it was reported that UK inflation had fallen to its lowest level in almost three years. Inflation, as measured by the Consumer Prices Index (CPI) was recorded in April at 2.30%, down from 3.20% in March. The news was welcomed by both consumers and the government as it showed inflation returning closer to the Bank of England’s (BoE) target rate of 2.00%.

Financial markets reacted negatively to the news. Market forecasts had expected the reading to be even lower at 2.1%. While this difference between expectations and reality is small, the perceived stickiness of inflation has kept the debate around the timing of interest rate cuts fluid.

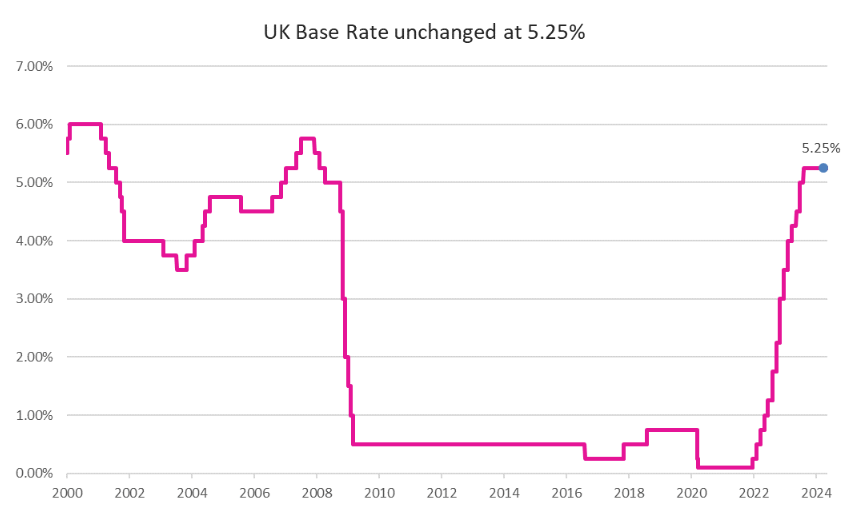

Earlier in the month, the BoE held interest rates at 5.25% for the sixth time in a row. Of greater significance was the voting split of 7-2 in favour of holding rates. This marked an extra member voting in favour of a cut. The BoE at the time noted “encouraging news” on inflation, and the likelihood that this will move even closer to the target rate of 2.00% in the coming months.

Following the meeting of the BoE, the gilt market initially adjusted to price a higher probability of a cut at the June meeting. However, with inflation in April not falling as much as the market had expected, optimism for a rate cut in June was tempered. Gilt yields rose and some commentators are now expecting the first interest cut to be made later in the year.

Economic Recovery?

Alongside slowing inflation, improving economic data could well have influenced Sunak’s surprise decision. The UK economy exited a shallow recession in the first quarter of 2024, with gross domestic product (GDP) increasing by 0.60%, ahead of expectations of growth of 0.40%. The Office for National Statistics estimated that house prices rose by 0.70% between February and March, with a year-on-year increase of 1.80%. This was the first recorded annual increase since June 2023.

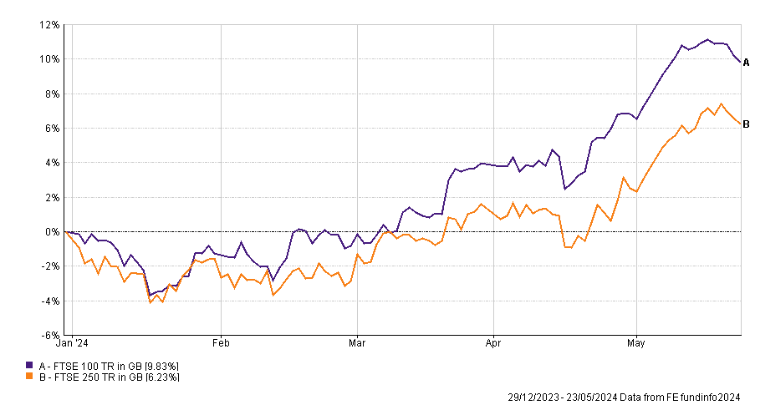

The UK equity market, considered a global laggard in recent years, has been in fine form, with the FTSE 100 establishing a number of record highs during the month. UK equities continue to trade on valuation discounts relative to their developed market peers. This has not gone unnoticed by investors, be they individual, or corporate.

There has been a noticeable increase in takeover activity, some successful, others rebuffed. However, interestingly, such activity has been broad based, both in terms of market capitalisation and sector. Companies have also been active in buying back and retiring their own equity. Buybacks and takeovers, alongside the absence of new listings, have served to shrink the pool of publicly traded equity available to investors, which whilst positive for short-term returns, is not a healthy long-term dynamic for the economy.

On the subject of new listings, the small module computer manufacturer, Raspberry Pi, provided a dash of optimism when announcing plans for an initial public offering on the London Stock Exchange. Securing new listings, and breathing new life into the UK equity market, will be a key priority for whatever government is formed post the July general election.

The election and investment markets

The imminent UK general election prompts questions regarding the potential impact on financial markets. The initial reaction on the announcement was sanguine. As manifestos are published, and campaigning moves to full vigour, some turbulence might arise as policies are announced and candidates compete for the attention of voters. However, each party faces the same dynamics of underinvestment in public services and infrastructure, alongside stretched finances.

With memories of Liz Truss’s ill-fated mini-budget still fresh in the minds of politicians, the need to remain credible is paramount. Given recent polls, investment markets will assume a Labour victory and will already have priced in what can be expected from that result. A lot can change however between now and election day. Whatever the gyrations ahead, the UK general election is not expected to be as divisive as the US Presidential election in November.

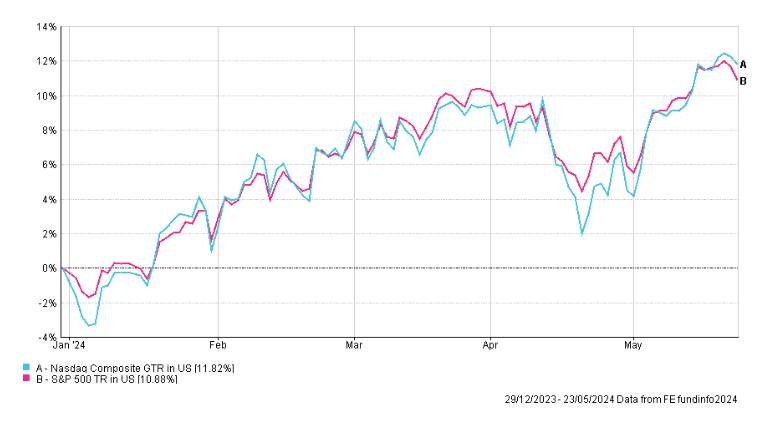

Staying with the US, Nvidia, the poster child for the boom in artificial intelligence, delivered another set of blistering quarterly results. The results, which surpassed very buoyant expectations, briefly powered the technology focused NASDAQ Composite index to a record high. The shares of the best-in-class chip provider, which already trade on a premium valuation, leave investors pondering how long can such a phenomenal rate of growth be maintained?