As expected, the US central bank, the Federal Reserve, commenced its interest rate cutting cycle on 18th September with its first cut to interest rates since March 2020. Ahead of the meeting, there was a fluid debate regarding the size of the first cut. A simple 0.25% cut, or a more aggressive move of lowering rates by 0.50%. The latter option was chosen, taking the target range down to 4.75%-5.00%.

Aggressive Rate Cut

The decision was not unanimous. Federal Reserve Governor, Michelle Bowman, advocated for a more moderate cut of 0.25%. Rates had previously been held at what was a 23 year high since July 2023. Chair of the Federal Reserve, Jerome Powell, contested views that the size of the cut highlighted that the central bank was “catching up,” following weakening labour market data.

Investment markets traded in volatile fashion in the immediate aftermath of the cut. US equity indices initially rallied in response to the decision, before ending the session marginally down after traders digested the size of the cut and examined the accompanying commentary in more detail. Markets opened the following day in a more buoyant fashion and US equity indexes reached new record highs as optimistic sentiment dominated.

Economic Growth

The boost for investors was new economic data from the central bank forecasting solid economic growth through 2025. The meeting followed news earlier in the month that inflation in the US, as measured by the Consumer Price Index (CPI), had fallen to 2.50% in August. A reduction from the July print of 2.90%. Whilst still above the target level of 2.00%, the Federal Reserve sees inflation ending the year at 2.60%, falling to 2.20% in 2025.

For much of September, investors have focused on this economic data for signs of economic strength or weakness. Concerns over a slowing job market were allayed as nonfarm payrolls data for August suggested the US economy added 142,000 jobs. Alongside this, the unemployment rate in the US ticked down from 4.30%, to 4.20%. While investors will likely remain cautious around any disappointing data points in coming months, the US economy does not appear to be showing recessionary trends.

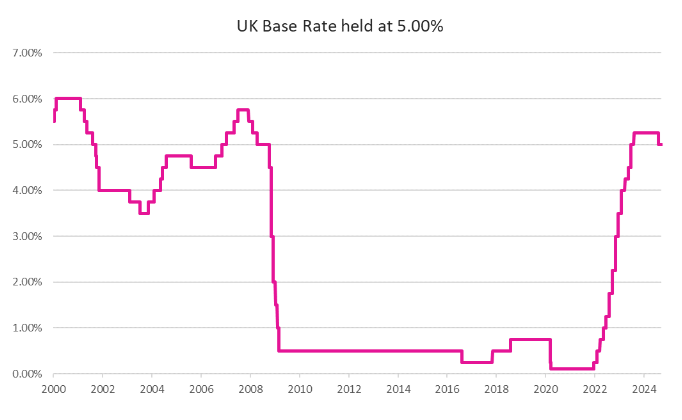

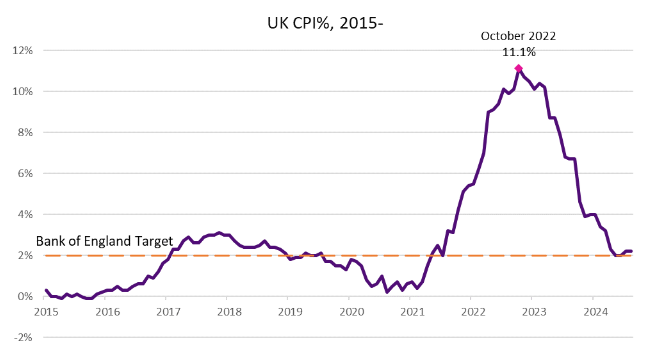

The UK economy

In the UK, CPI inflation for August was recorded at 2.20%, unchanged from the prior month. Voting 8-1 in favour, the Monetary Policy Committee of the Bank of England (BoE) held interest rates at 5.00% on 19th September. The lone dissenter voted for a 0.25% cut. After the meeting, sterling strengthened to a two and a half year high against the dollar.

BoE Governor, Andrew Bailey, suggested that further rate cuts are on the way should inflation remain at low levels, but cautioned against cutting too soon. One area of concern for the BoE remains the stark gap between goods and services inflation. Deflation in CPI goods deepened from -0.60% to -0.90%. While CPI services rose from 5.20% to 5.60%. As a services dominated economy, there are worries this could drive the headline rate of inflation higher.

Also in focus for investors at the recent BoE meeting was the programme of quantitative tightening. As well as voting to hold interest rates, the BoE also voted to reduce the stock of gilts by £100bn over the next 12 months, in step with the prior period. This will be achieved via sales and natural maturation. Quantitative tightening is the process of unwinding the vast bond buying programme conducted during the Covid-19 pandemic. The opposite of quantitative easing, in simple terms it essentially removes money from the economy.

Europe and elsewhere

The European Central Bank made its second cut to interest rates this year, reducing rates to 3.50% on 12th September. The bank also revised down its 2024 growth forecast to 0.80%, owing to weaker domestic demand. Eurozone inflation was recorded at 2.20% while inflation across the entire European Union, including members not using the euro, was 2.40%. Both figures were lower than the preceding month. Romania recorded the highest rate at 5.30%, with Lithuania accounting for the lowest at 0.80%.

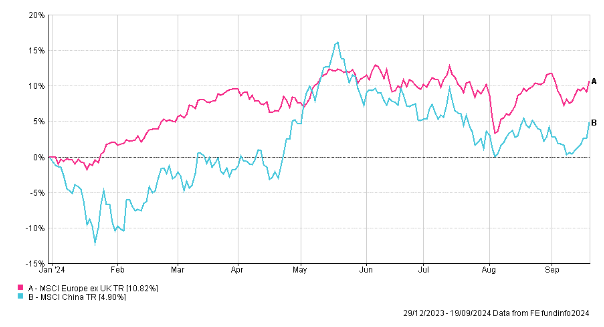

In China, weaker than expected industrial output and retail sales figures both stoked doubts about the health of the economy. After years of leading growth figures, investors continue to question the ambition for 5% gross domestic product (GDP) growth in 2024. The Producer Price Index, sometimes referred to as factory gate prices, remains in negative territory. This is fuelling concerns that China is exporting deflation as a result of overcapacity within its economy.