After a difficult year for investors, suddenly there is confidence in markets. For months, the narrative dominating the investment outlook has been high inflation and the reaction of central banks in their attempts to control it. However, with inflation appearing to be falling globally, central banks in the UK, US, and Europe have given tentative signs that interest rates may have reached their peak.

Interest rates down from here?

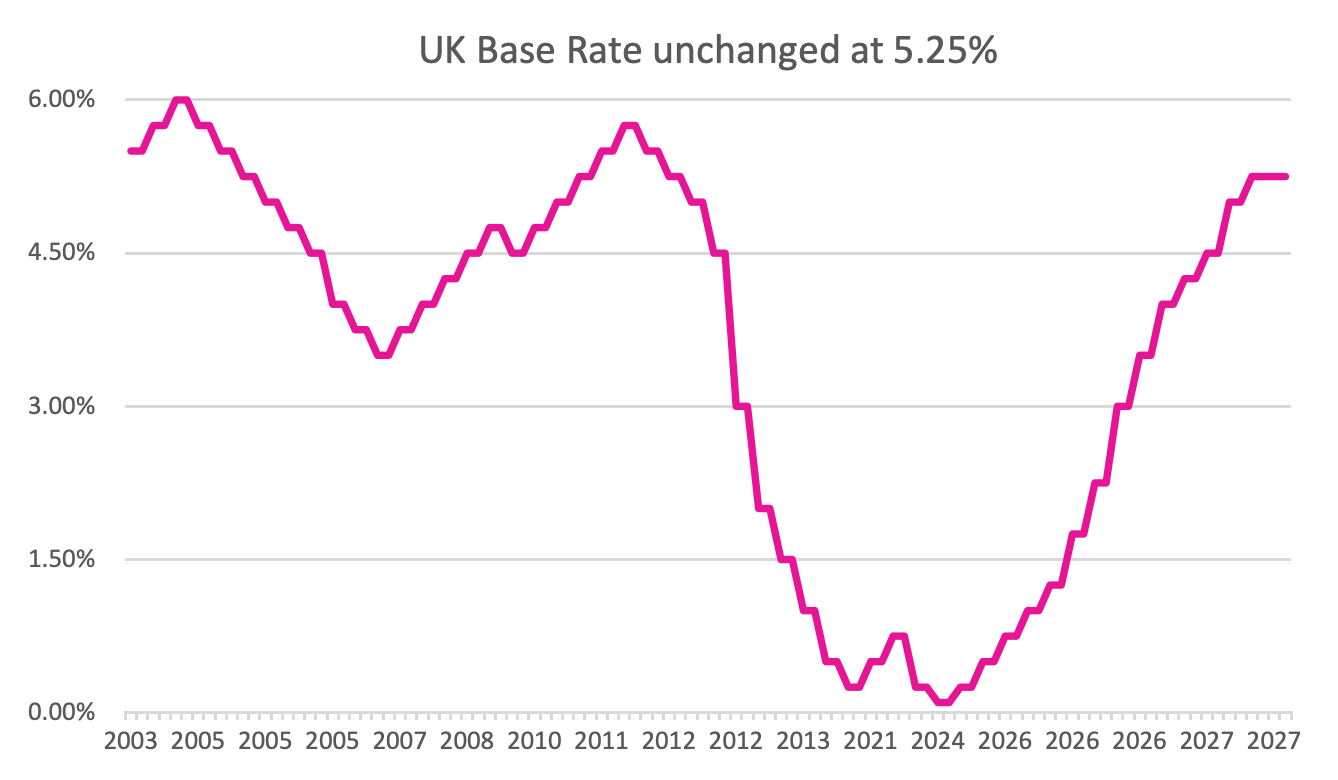

Markets have been under pressure in recent months as sentiment turned to an expectation that interest rates might remain ‘higher for longer’. Over the last two years, and for fourteen consecutive meetings of the Bank of England’s (BoE) Monetary Policy Committee, the decision was made to increase the base rate. This meant interest rates have risen from 0.10%, in December 2021, to 5.25%. However, for the past two meetings, the decision was made to pause interest rate rises. The US Federal Reserve and European Central Bank also maintained their respective base rates at their most recent meetings prompting investors to suggest that rates had reached their ‘peak’.

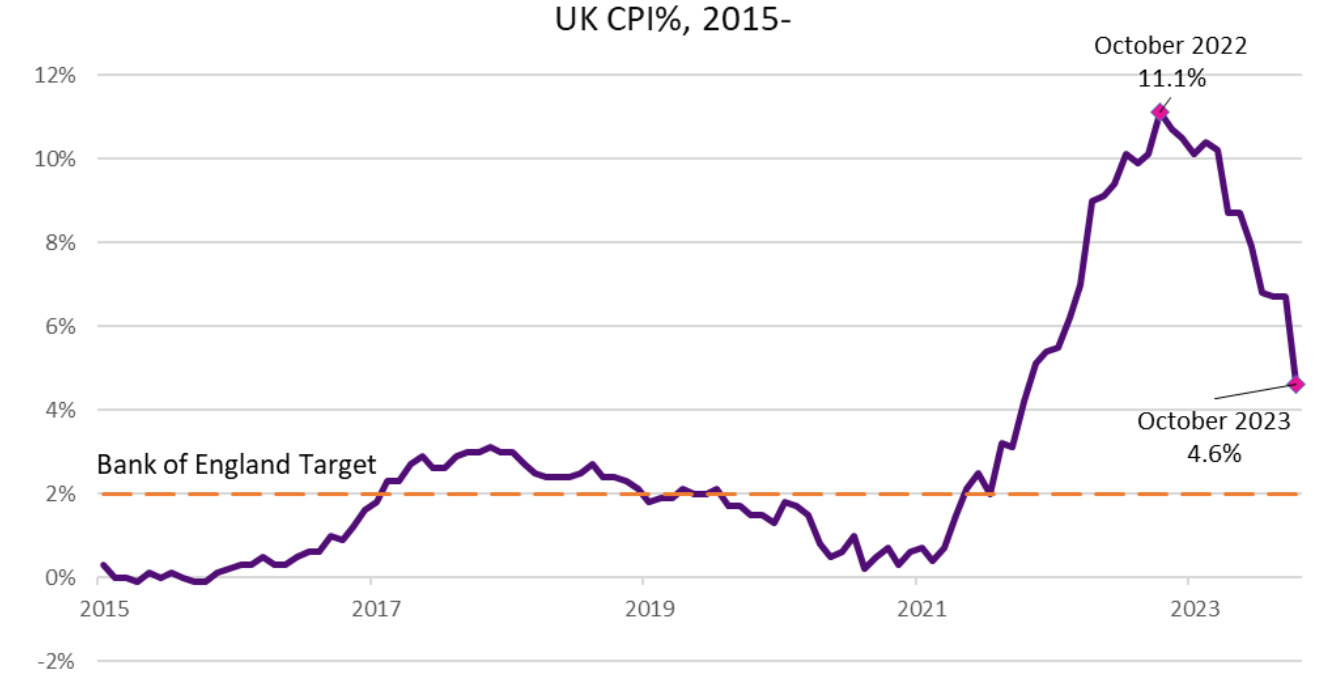

There is certainly a case for this argument as these pauses have been prompted by falling inflation readings. In the US, inflation fell further than expectations and was recorded in October at 3.20%. Whatever credit UK Prime Minister Rishi Sunak can claim in ‘halving’ inflation, this ‘pledge’ has been achieved given the most recent inflation figures for the UK. UK CPI inflation in October was measured at 4.6%, down from 6.7% in September. Much of this fall can be attributed to a fall in the energy price cap compared to October last year (when inflation was at its peak of 11.1%).

Market confidence

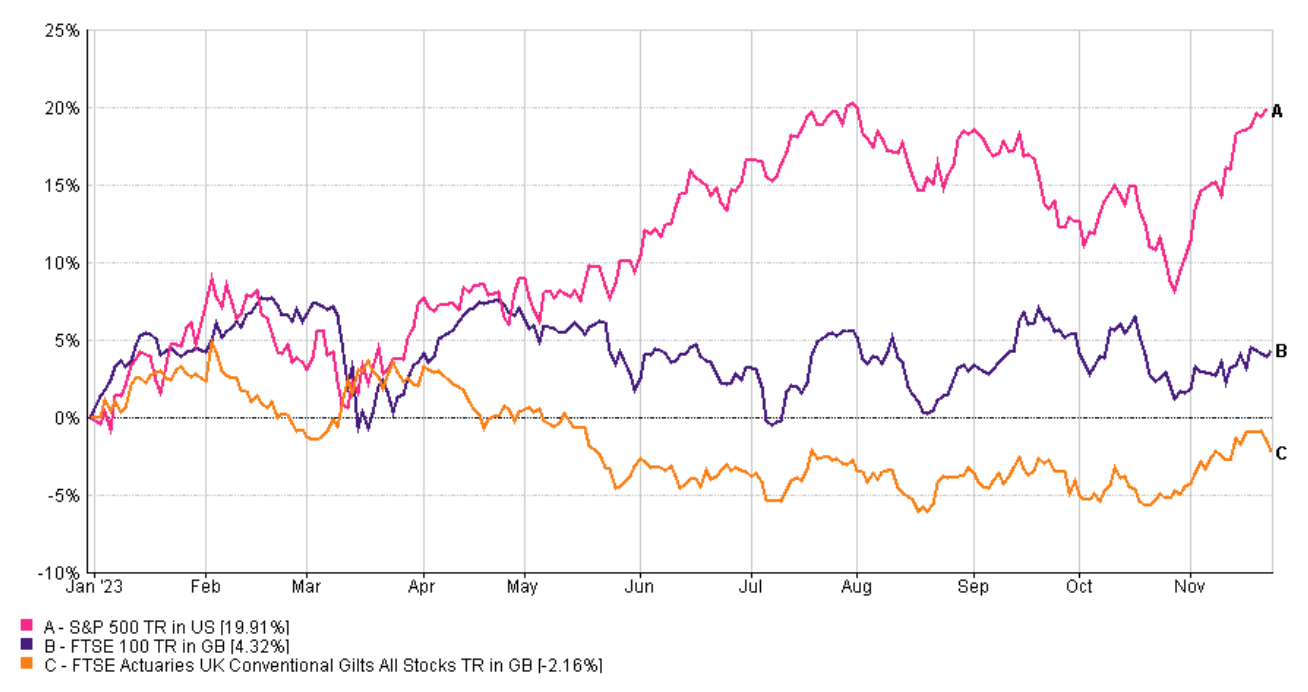

With inflation on a downward trend, investors are now more hopeful it may give central banks greater scope to begin cutting interest rates. Markets have therefore pivoted back from the ‘higher for longer’ narrative towards the original hope that interest rates may be set to fall earlier and faster. This change in sentiment, alongside growing investor enthusiasm, has resulted in a sharp rise across all developed markets in both equities and fixed interest.

While inflationary pressures do appear to be weakening, central banks have been keen to stress to investors that the job of fighting inflation is not finished. With inflation in the UK at 4.60%, prices are still rising at over double the BoE’s target inflation rate of 2%. It therefore remains to be seen which side of the argument will win out.

The great uncertainty for central banks, in any future policy moves, is the lagged impact of interest rate rises in the economy. For example, in the UK many households remain on low interest fixed-rate mortgages taken out when interest rates were at record lows in the aftermath of the pandemic. As households re-mortgage, this impact on household finances is one area that could have a detrimental impact on consumption. It is this fine balancing act which central banks continue to tread; fighting inflation without causing undue economic harm. While inflationary pressures remain more subdued however, investors will continue to hope for supportive monetary policy in the near future.

The Magnificent Seven

One of the standout investment markets in 2023 has been US equities. Despite inflationary pressures, and rising interest rates, US stock market indices have delivered strong performance with the S&P 500 delivering a return of nearly 20% year to date. What is interesting about this performance however is how much of the performance of the overall index has been driven by a small number of companies.

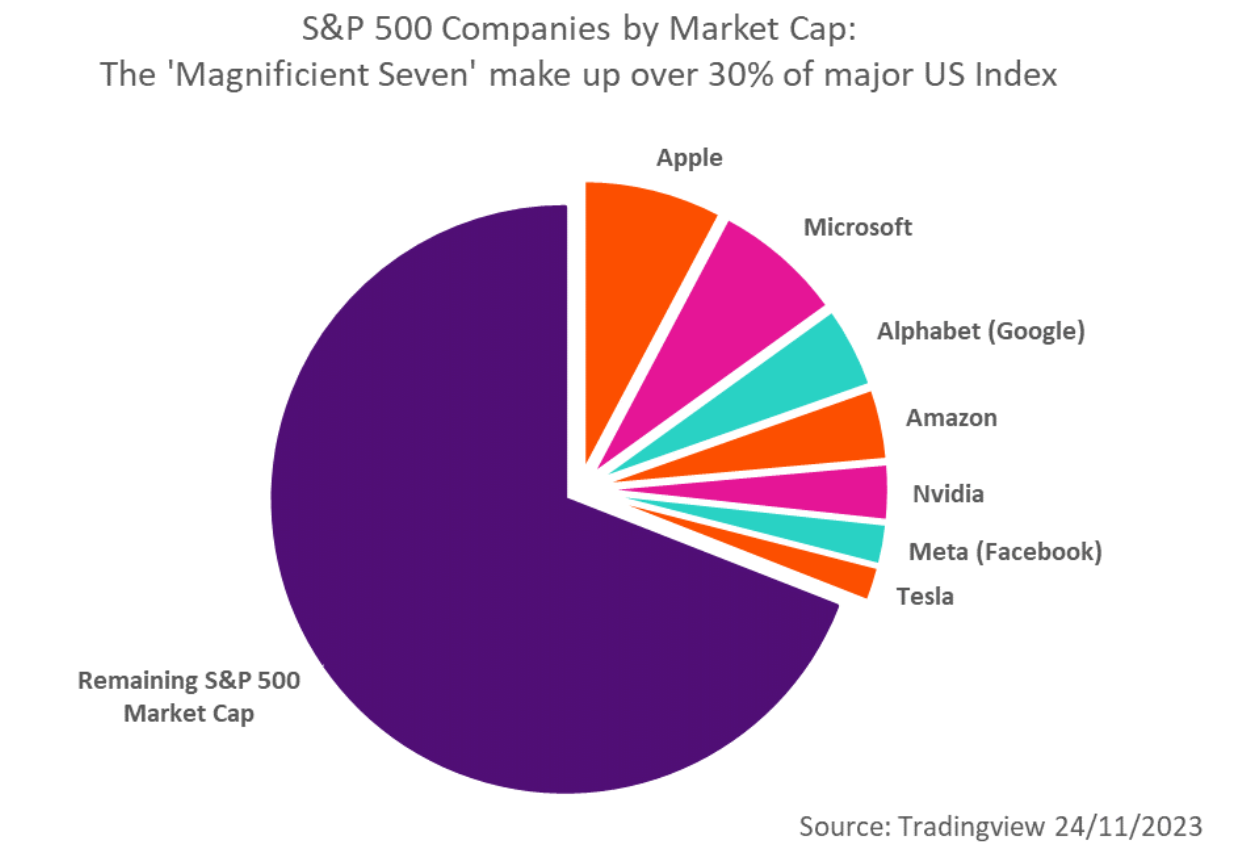

Measured by market cap, the seven largest companies in the S&P 500 (Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla) now represent over 30% of the index as a whole. These seven companies, monikered ‘the magnificent seven’, have collectively delivered returns of more than 50% year to date. The remaining 493 companies in the S&P 500 index have delivered negligible growth. So while US stock market returns have been very strong, and viewed purely on an index level they have, this performance has been almost entirely driven by just seven companies.

With the disparity in performance between the mega mega-cap tech titans and the rest of the US stock market, it is tempting to make comparisons with the 1990s dot-com tech bubble. These companies are trading on eyewatering valuations, but the reality is they are very strong businesses. It is not simply a fact of they have ‘.com’ in their company name and the promise of a shiny website. These companies enjoy a near monopoly in their industry and generate strong revenues as a result. They are the amongst the best companies in the world and have earned their position.

That is not to say however they are without threat. In the case of, for example, Nvidia, investor enthusiasm for the company has centred on the ‘promise’ of AI and their industry leading position. Revenues and profits have been forecasted to grow to stratospheric levels and there is always a danger these expectations may not be met. Similarly, it would not be surprising to see industry regulators become uneasy with these companies’ dominant positions. For now, the ‘magnificent seven’ continue to dominate US stock market indices and will remain a large driver of returns as a result.