Investment markets have largely shrugged off the impact of Donald Trump’s trade tariffs following the announcement of various pauses and concessions. While US stock markets have not recovered completely to their record highs, markets have enjoyed a strong run of performance in recovering from the turbulence they experienced. Investors remain concerned however about the prospect of future tariff announcements, alongside the impact of inflation and rising government debt levels.

Moving on up

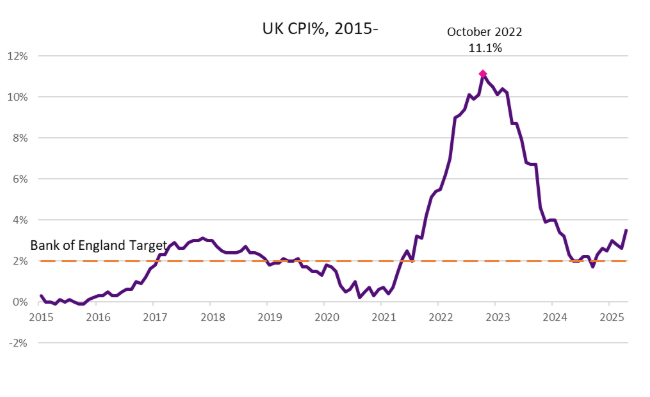

In the UK, the Consumer Prices Index (CPI) measure of inflation for April 2025 at 3.50% reversed the recent trend of falling inflation. This reading was an increase from the March level of 2.60%. April’s measure was expected to rise as the cost of many bills and utilities face annual increases in the month, although this measure was higher than economists had forecast.

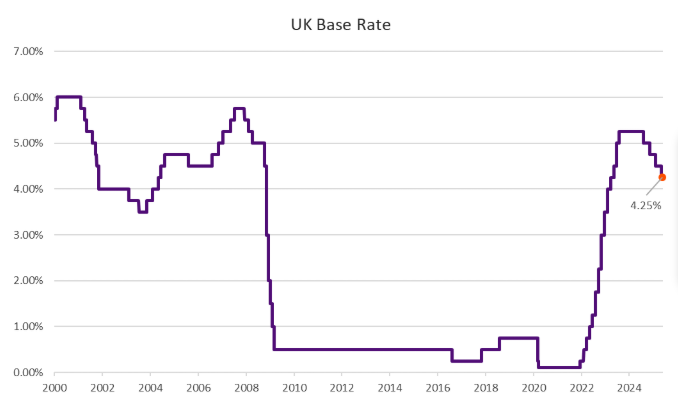

Earlier in the month, the Monetary Policy Committee of the Bank of England voted to cut interest rates by 0.25%, taking the base rate to 4.25%. The decision was however divided. Of the nine voters, five voted for a 0.25% cut, two voted for a larger reduction of 0.50%, with two voting for rates to remain unchanged. Bank Governor, Andrew Bailey, noted that while the likely direction of rates is down, the timing is less clear owing to economic uncertainties.

In positive news, the UK economy is estimated to have expanded by 0.70% in the opening quarter of 2025, exceeding expectations. It is likely however that some activity was pulled forward in anticipation of the tariffs levied by the administration of Donald Trump. On a positive footing however, the UK government has reached trade agreements with India, the US, and the European Union. Each respective agreement evoked a variety of conjecture, with the full merits of each likely to take many years to assess.

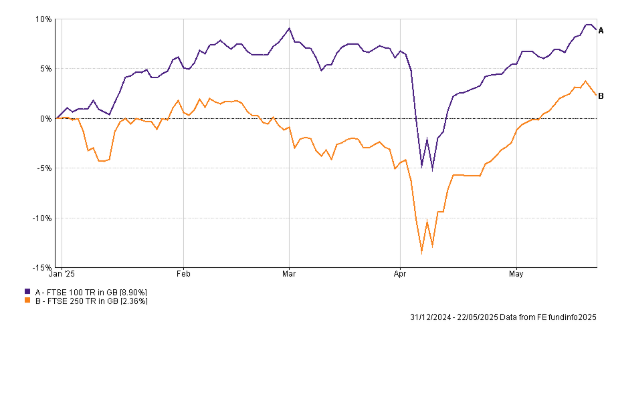

Despite the turbulence following the initial announcement of Trump’s Tariffs, UK stock markets have made a positive start to 2025. The large-cap FTSE 100 sits on solid year to date gains, outperforming the leading US indexes. The more domestically focused FTSE 250 is also positive year to date following a strong recovery in April and May. One area of concern for investors is rising bond yields with UK Gilt yields moving higher over the month, a trend noted globally.

Big, Beautiful Bill

In contrast to the Bank of England, the US central bank, the Federal Reserve, made no change to interest rates at its May meeting. The biggest factor in this decision was the economic uncertainties relating to tariffs. The decision drew anticipated criticism from Donald Trump who has pushed for lower rates since he returned to office. Lower interest rates in theory provide greater opportunities for economic growth; something which Trump wants to take credit for.

As in the UK, US bond yields rose sharply in May. Largely this was a result of investor concern about the sustainability of US government spending, and the country’s ability to service its ongoing debt commitments. These fears were exacerbated by Trump’s “big, beautiful bill” which narrowly passed through the House of Representatives by a 215-214 vote. The more than 1,000-page bill includes a wide range of policies including tax cuts, changes to benefits, and, significantly for investors, the ability for the US government to borrow more money.

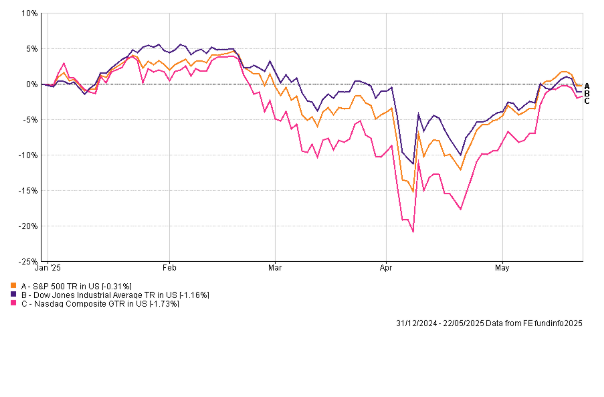

There were a small number of Republican Party dissenters. Speaker, Mike Johnson, aims to get the bill on the desk of Trump by the 4th of July, assuming it also passes the Senate. Investors greeted the passage of the bill with caution, noting the potential for the already wide budget deficit to further deteriorate. US Treasury yields will be closely monitored in the coming weeks and months after rising sharply in May. US equities, which have bounced off their post-tariff lows, are also likely to be sensitive to bond yield movements.

Global Markets

As in the UK, European equities have also booked solid year to date gains despite the trade uncertainties with the US. Inflation in the Eurozone continues to moderate and is expected to fall to the target level of 2% by the middle of this year. This assumes lower energy prices, no further escalation in tariffs, and the deflationary impact of diverted Chinese imports as items are redirected from the USA.

In China, the government announced a further stimulus package to boost growth. The package was based on monetary easing, via lower interest rates and injections of liquidity. The package received a muted response in contrast to the explosive equity market surge after the intervention in September 2024. Investors remain concerned about the potential future impact of tariffs and the ability of the government to provide continued fiscal support to the Chinese economy.