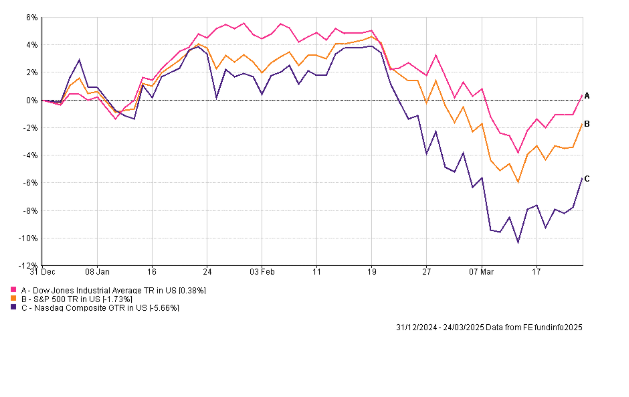

After two years of exceptional returns, US equities continued their difficult start to 2025. The biggest concern for investors remains the potential impact of the tariff-led trade and diplomacy policy of US President Donald Trump. For UK Investors, the fall in value of US equities has been exaggerated by the relative impact of currencies due to a weakening US dollar.

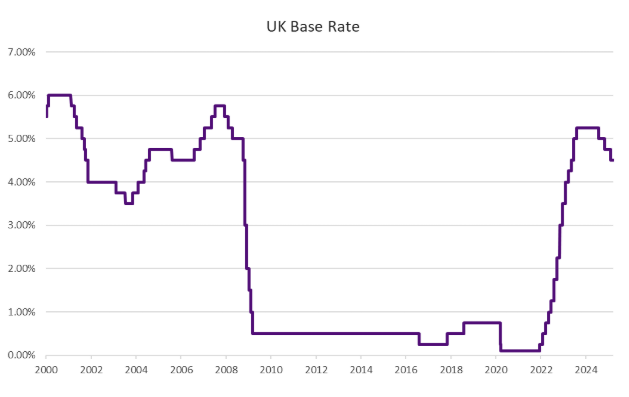

Uncertainty was an influential factor behind the US Central Bank, the Federal Reserve’s, decision to keep interest rates unchanged at a range of 4.25%-4.50% at its March meeting. Rates have been held at this level since December 2024. Whilst noting that economic conditions remain healthy, the Federal Reserve downgraded its 2025 economic growth forecast by 0.40% to 1.70%. In addition, inflation forecasts were raised, owing to the likely inflationary impacts from levying tariffs on imports.

The high degree of uncertainty has been the principal reason for the sharp falls in US stock markets. The Nasdaq Composite index entered correction territory, defined as a fall of over 10% from peak levels, with the S&P 500 index also briefly flirting with the measure. The potential impact of tariffs on US companies has meant investors have looked to other regions and assets offering greater perceived stability.

For US interest rates, the median estimate of committee members is for two cuts in rates over the remainder of 2025. However, assumptions will likely be fluid as circumstances evolve. Donald Trump’s rhetoric on trade tariffs has been erratic, veering from hardline to flexible. This uncertainty, alongside lower growth assumptions, are factors weighing on the dollar which has lost ground against leading currencies. A softening of Trump’s rhetoric in recent weeks has alleviated some investor fears but markets remain below their record highs.

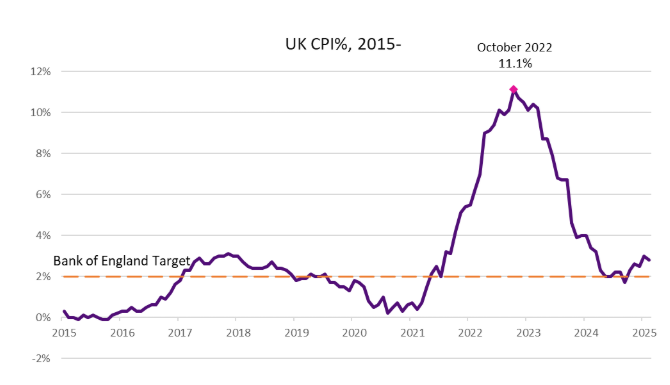

In the UK, the bank of England made no change to interest rates at its March meeting. This decision was widely anticipated with UK inflation, as measured by the Consumer Prices Index (CPI), at the time of the decision rising to 3.00% in January, up from 2.50% in December. Inflation data reported in late March showed the rate of inflation fall slightly to 2.80%.

Investor attention was instead focused on speculation surrounding the Chancellor’s Spring Statement alongside updated economic forecasts from the Office for Budget Responsibility (OBR) for the UK economy and public finances. The forecasts are important in estimating any fiscal headroom Reeves’s has in maintaining her fiscal rules of covering general expenditure with revenue, as opposed to borrowing.

In the lead up to the statement, investors largely anticipated the announced spending cuts to enable the chancellor to meet those self-imposed fiscal rules. Lower growth forecasts, higher bond yields, and above target inflation are all factors impacting on public finances. This is in addition to other pledges such as increased defence spending in response to the war in Ukraine.

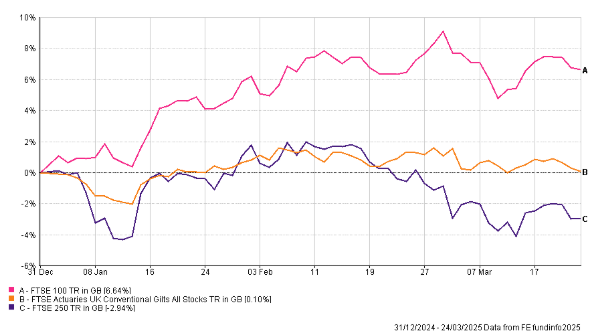

Despite indifferent performance over March, the FTSE 100 has enjoyed a strong start to 2025 and is one of the best performing major asset classes in the first three months of the year. There are further positive signs in the broader UK market. Companies are buying back shares and raising dividends, whilst takeover activity continues which can be interpreted as a sign of value.

Industry surveys, such as the Purchasing Managers Index (PMI) are also showing promising signs for the UK economy. Readings for the service sector indicated an acceleration in activity. In contrast however, the reading for the manufacturing sector suggested a decline in activity. This slowdown has been attributed to uncertainty surrounding the potential impact of Donald Trump’s tariff-led trade policy.

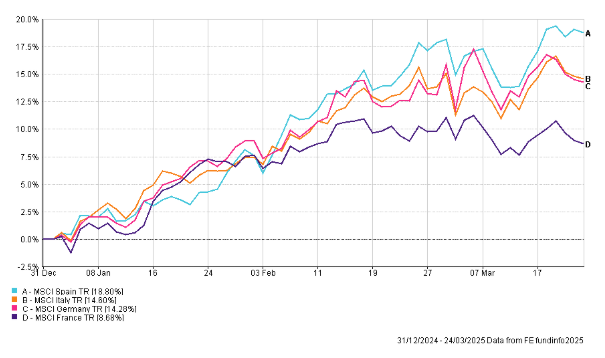

European equities have also started 2025 in fine form. Investor optimism has increased in Germany, the continent’s largest economy, following the election earlier this year. The new government has announced a reform of fiscal rules, potentially unleashing large scale investment in both defence and infrastructure. This would create a significant boost to the recently depressed manufacturing base of the country. US-led talks about ending the war in Ukraine remain volatile, however an end to the war in Ukraine would naturally be beneficial to reducing trade uncertainty in the region.

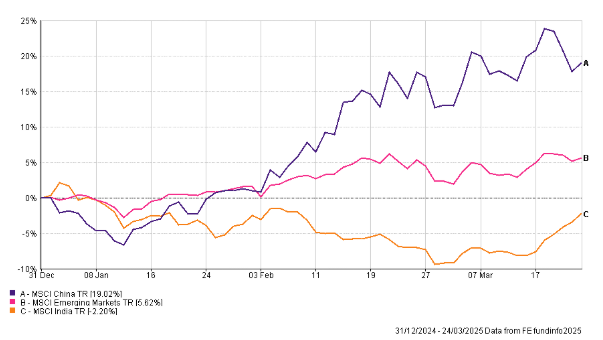

In Emerging Markets, Chinese equities have enjoyed a positive start to the year. As large exporters however, China is particularly exposed to any potential trade tariffs which could impact on demand for their products. Indian equities enjoyed a more positive month in March following a difficult run of performance, but are also exposed to the same uncertainty surrounding tariffs.