Investment markets continue to enjoy a buoyant start to 2024. Falling inflation, the prospect of falling interest rates, and strong earnings reports from major companies are creating an optimistic outlook for investors. With positive investor sentiment, many global stock markets continue to set new record-highs.

Land of the Rising Stocks

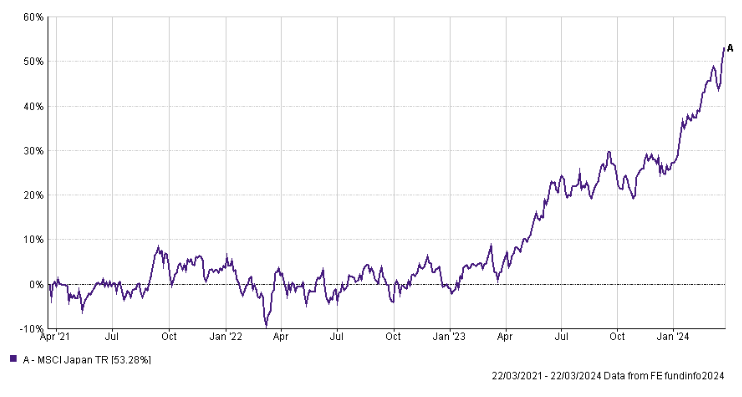

Japanese stock markets are one such example with indexes in the country continuing to attract investor support. The widely followed Nikkei 225 index crossed the 41,000 level for the first time on 22nd March 2024. Viewed out of context, the fact investors welcomed the news that inflation in Japan has increased (reaching 2.80%, up from 2.20% in January) might appear surprising. However, sustained, modest, inflation levels are seen as confirmation that the Japanese economy is successfully emerging from a long struggle against deflation.

Earlier in the month, the Bank of Japan (BOJ) ended eight years of negative interest rates, designed to reflate the economy. The BOJ increased rates for the first time in 17 years, from -0.10% to between 0% and 0.10%. Greater confidence in the Japanese economy, combined with a greater focus on shareholder returns, continues to attract investor interest in the country.

Battling Inflation

In contrast to Japan, it is a very different landscape in other developed economies. The emphasis is still on taming inflation and opening the path for interest rate cuts.

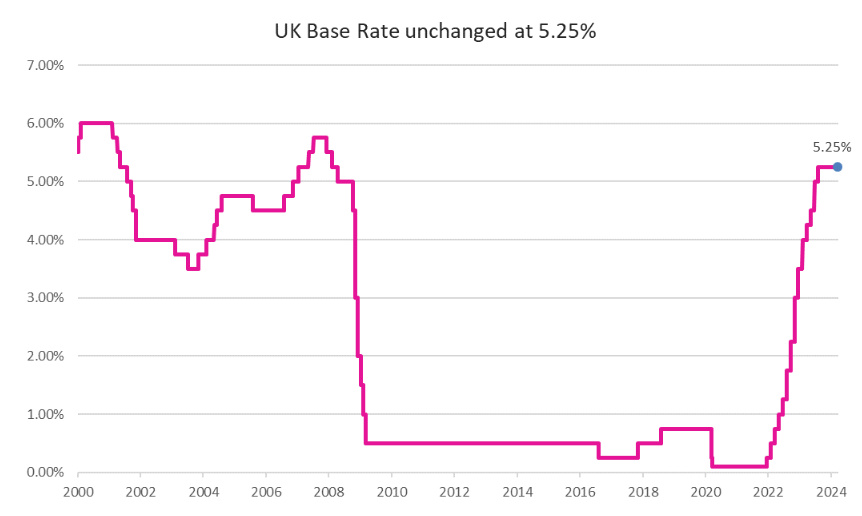

In line with investor expectations the Bank of England (BoE) kept interest rates on hold in March for the fifth consecutive meeting. The BoE noted encouraging signs of falling inflation. The news was followed up by comments from Bank of England Governor, Andrew Bailey, that interest rate cuts will be “in play” at future meetings.

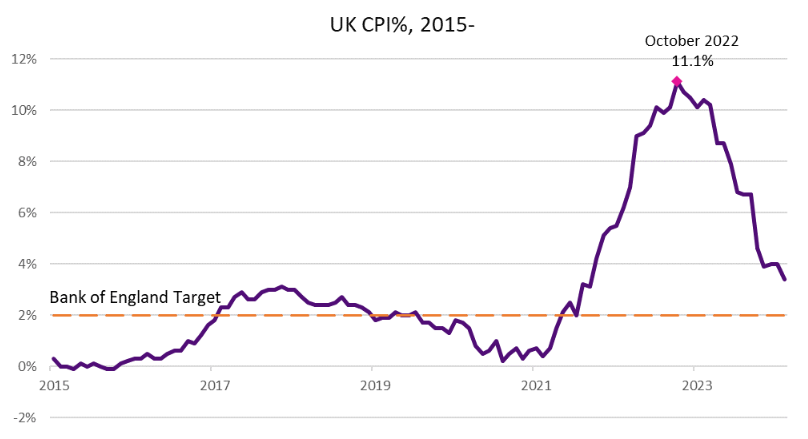

The UK Consumer Prices Index (CPI) inflation reading for February 2024 was 3.40%, lower than consensus forecasts. This represented a significant fall from the January reading of 4.00%. The core reading, excluding energy, food, alcohol, and tobacco, also fell to 4.80% from 5.10%. It is worth noting still that there is a notable divergence between CPI goods, and CPI services; recorded at 1.10% and 6.10% respectively. As a service sector orientated economy, the respective figures indicate that inflationary risks are not completely vanquished.

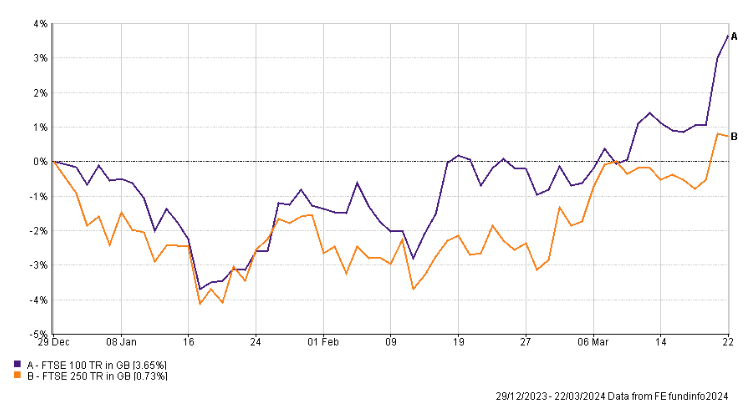

Nevertheless, both equities and bonds responded positively to both the inflation data, and the actions and comments made by the BoE. The FTSE 100 moved within sight of the 8,000 level, a threshold it briefly crossed in February 2023.

Economic Outlook

The outlook for the UK economy is still mixed. In positive news, there was some relief for household budgets, with the prices for food and non-alcoholic beverages increasing by 5.00%, a reduction from the January reading of 7.00%. There was some economic disappointment however, as retail sales for February were flat. This was however thought to have reflected wet weather for the month rather than hesitancy to spend.

Despite this flat line in retail sales, the UK economy is still expected to emerge from its shallow recession. The UK was confirmed to be in a ‘technical’ recession following two consecutive quarters of modestly negative growth to close 2023. It is forecast however that the first quarter of 2024 will have delivered economic growth.

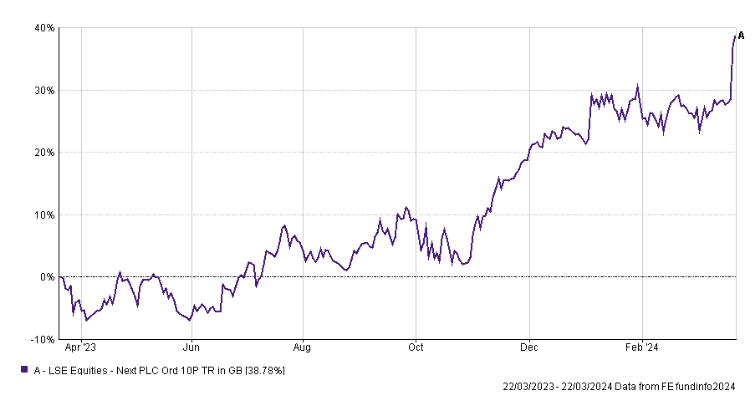

Retail bellwether Next delivered forecast-beating results for the year end of January 2024, powering the shares to an all-time high. There was a 5% increase in pre-tax profit to a record high level of £918m. Lord Wolfson, known for his cautious guidance, gave an uncharacteristically bullish assessment for the year ahead. Encouragingly, for both consumers, and the broader inflation outlook, amid falling costs, Wolfson noted the potential for some small price decreases throughout the year.

US Optimism

Meeting a day earlier than the BoE, the US Federal Reserve also chose to keep interest rates at their current levels. The Federal Reserve also offered optimism moving forward, suggesting that as many as three cuts could be made before the year end. These comments were however delivered with the condition that the committee wants to see more evidence that inflation is continuing to slow, amid an economy that is performing relatively well.

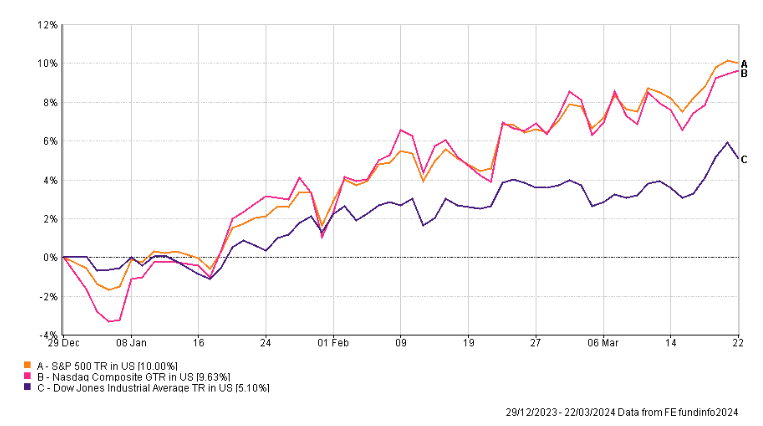

The comments were supportive of the equity market, with the Dow Jones converging on the 40,000 level for the first time in its history. Less than four years after reaching the 30,000 level for the first time. In addition, both the S&P 500, and Nasdaq Composite indexes sit on strong year-to-date gains.

Returns continue to be heavily dominated by behemoth technology stocks, and the broader theme of Artificial Intelligence (AI). Whilst these remain exceptionally well positioned in their respective markets, the debate over appropriate valuations continues. The divergence between stocks categorised as growth and value is eye-wateringly wide. There are also wide differentials between global markets.