Following a strong start to the year for investment markets, March proved much more volatile owing to concerns surrounding the financial strength of global banks. The Spring Statement, delivered by Chancellor Jeremy Hunt, on 15th March 2023, struggled to maintain headlines. The news was instead enveloped by troubles within the global financial system.

In the statement, Hunt unveiled a portfolio of growth initiatives, with a particular focus on trying to remove ‘disincentives’ to work. There was also relief for households, with a three-month extension of the energy price cap guarantee at £2,500 per annum for the average household, running from April to the end of June 2023. Beyond this point, it is hoped that the price cap will fall significantly as energy prices fall. Conversely, the tax burden continues to rise. The government is keen to project an image of fiscal responsibility following the tumultuous budget delivered by former Chancellor, Kwasi Kwarteng, under the short-lived administration of Liz Truss.

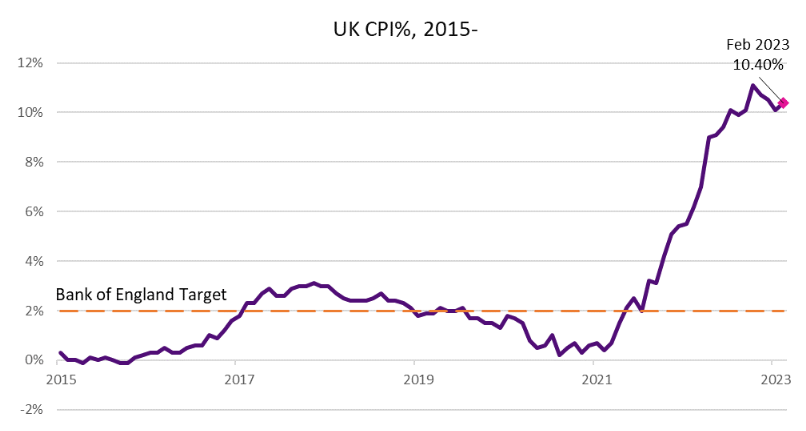

The maintenance of tax bands in an inflationary environment will result in workers seeing more of their income being paid away to the exchequer. Working with Office for Budget Responsibility (OBR) forecasts, the Chancellor delivered upbeat news on inflation, with projections for the consumer price index (CPI) falling to around 3% by the end of the year. Forecasters were surprised by the UK CPI print for February 2023, which reversed a run of three straight months of lower readings, coming in at 10.40%. Food prices were again an influential factor, be it in groceries, cafes, or restaurants.

Banking ‘Crisis’

Traversing back to before the Spring Statement. The rapid demise of technology sector focused, Silicon Valley Bank, heightened concerns about stresses in the financial system after a period of rapid interest rate increases by central bankers. Although the troubles afflicting Silicon Valley Bank related to a poorly managed maturity mismatch between deposits and investments, which came under pressure as interest rates increased, confidence began to erode in the wider financial system.

Initially, this spread within the US regional banking sector, where the regulatory framework is lighter, before moving onto Credit Suisse. There was no direct systemic link between the failure of Silicon Valley Bank and the distress experienced by Credit Suisse. However, years of underperformance and stated “material weakness” in internal financial reporting relating to previous years, proved to be potent, amid fragile confidence in the banking sector.

Prior to the troubles at Silicon Valley Bank, regulators were comfortable with the capital adequacy of Credit Suisse. But this provided to be insufficient as depositors withdrew large sums from the bank. This rendered the generous liquidity support provided by the Swiss authorities inadequate. Credit Suisse was ultimately acquired by another Swiss bank, UBS, which provided some stability within the banking sector and wider investment market. However, the way this acquisition took place introduced some uncertainty to the capital structure of banks.

Capital Structures

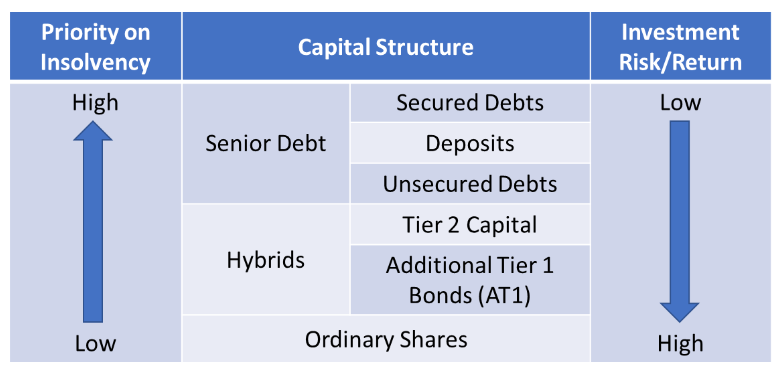

When banks, or any company, runs into trouble then there is generally assumed, and is written in law in many countries, to be an agreed order of priority for investors to receive their money back. In simple terms this can be condensed into secured debt, followed by unsecured debt, followed by shareholders. One of the reasons that corporate bonds are considered ‘safer’ than shares of the same company is a result of this assumed priority. However, this assumption broke down with Credit Suisse as a result of a special type of bond.

In the aftermath of the 2008 financial crisis, a new type of instrument called Additional Tier 1 bonds (AT1 bonds) was created to try to avoid some of the liquidity problems which banks faced at that time. While these instruments are not uniform, it was assumed that as bonds they would have priority over shares in the result of a bank facing financial difficulty. However, in the case of Credit Suisse, holders of AT1 Bonds saw their investment completely written down. While contrary to market expectations, those holding shares held on to a small amount of value.

The assumed role of AT1 bonds is to provide buffer capital, in that they convert to ordinary shares, should the capital ratios of a bank fall below a pre-determined level. Outside such events, being above ordinary shares in the capital structure, they are not expected to assume losses until the value of ordinary shares has depleted. The ensuing uncertainty prompted both the European Central Bank (ECB) and the Bank of England (BOE), to issue clarification that AT1 bonds continue to rank higher than ordinary shareholder of banks in their respective jurisdictions. Despite these assurances it can be easy to see why investors may not wish to hold these assets due to uncertainty about their worth.

Rock and a hard place

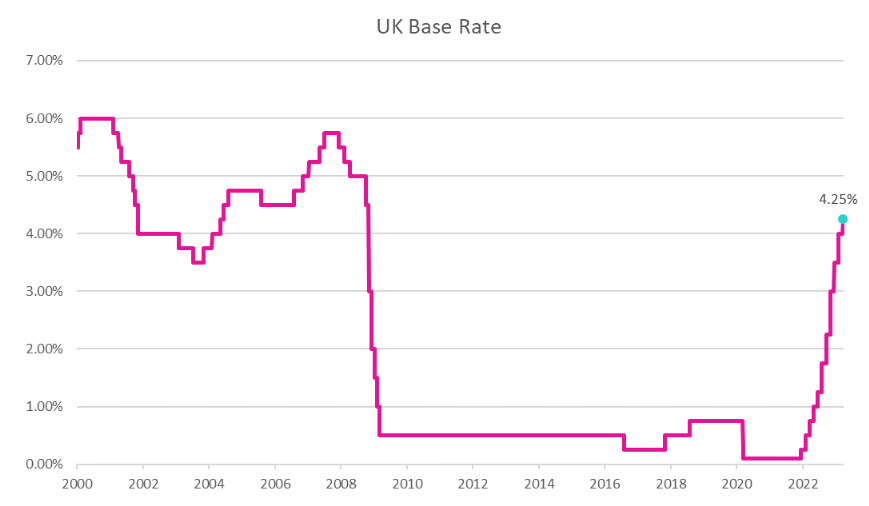

Mindful of the inflationary pressures within the global economy, the ECB, BOE and Federal Reserve all raised interest rates in March 2023. In the case of the BOE, rates were raised for the 11th consecutive meeting by 0.25%, to 4.25%. Central bankers are confronted by a vexing conundrum in balancing the desire for both price and financial stability. The desire for price stability, via efforts to tame inflation by a rapid path of interest rate increases, has exposed stresses in a financial system which has grown used to operating in a climate of cheap money.

Investors will be looking to see if policy errors relating to viewing post-pandemic inflation as transitory, are not followed by overtightening with interest rates increased too much. Inflation is forecast to fall in the second half of 2023 however the fear is if central banks raise rates too far the result will be a recession. Bond markets are currently pricing in interest rates peaking in the very near future. Market expectations are then suggesting interest rates may begin falling towards the end of 2023 and into 2024.

Invitation

If you would like to discuss your financial plan and investment strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

e: [email protected]

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.