Late July provided a challenging and volatile period of trading for investment markets. After regularly hitting record highs over the course of the year, the US Nasdaq Composite index fell by 3.64% on the 24th of July. This was the index’s worst trading day for nearly two years. Despite this volatility, US markets remain in positive territory year-to-date.

The recent declines were led by “Magnificent Seven” constituents, Alphabet (parent company of Google and YouTube) and Tesla. The former resulted from weaker advertising revenue, and the latter owing to a significant decline in quarterly profit. Beyond the immediate term, nothing has changed. Both companies are well-positioned in their respective markets.

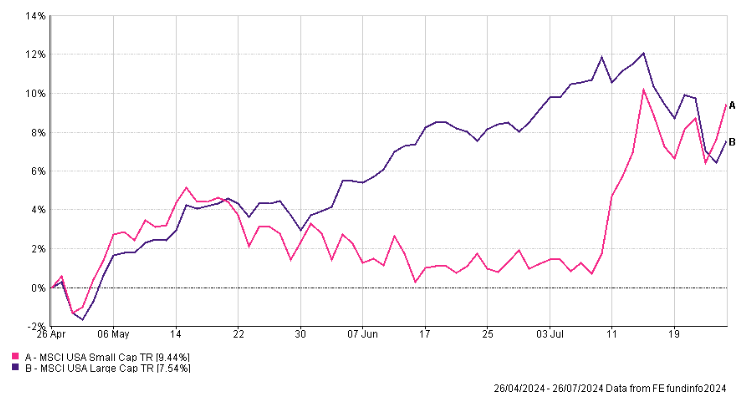

A more pressing matter has been valuations amid surging stock prices powered by enthusiasm for artificial intelligence. This has prompted some profit-taking and has seen capital rotated into stocks trading on lower valuations, including those considered ‘small caps’.

Politics Ignored

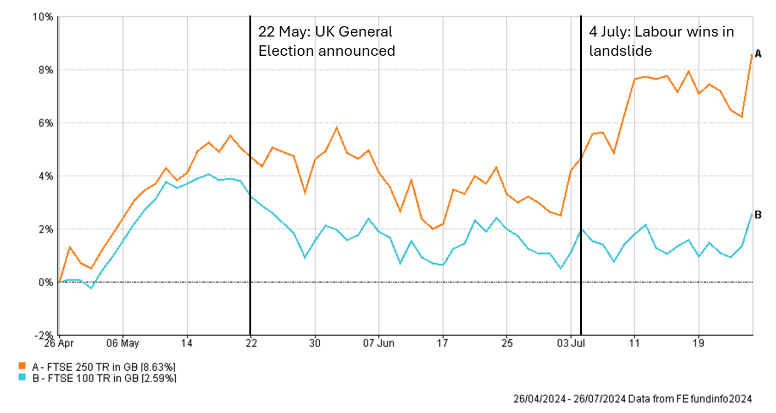

July also provided a slew of political news. Perhaps surprisingly, though, major developed markets paid little attention to it. The landslide Labour victory in the UK general election made no major impact on investment markets.

The new Labour government has made growth a key priority, along with fostering good relations with business and international partners. This is against a backdrop of challenging public finances. Financial markets remain poised for further direction in the much-anticipated Autumn Statement, although initial data points suggest that business is undeterred by the change in government.

In the US, the attempted assassination of Donald Trump, and the decision by Joe Biden to stand down as the Democratic Party nominee to run for office in November, also had a muted impact on financial markets.

Presumptive nominee, and current Vice President, Kamala Harris, is very much viewed as a continuity candidate. Current polling appears to favour former President Trump in the race for the White House. However, there is a long way to go, and Vice President Harris is early into her campaign. The attention which markets pay towards the US election will grow as the event looms closer.

Inflating Markets

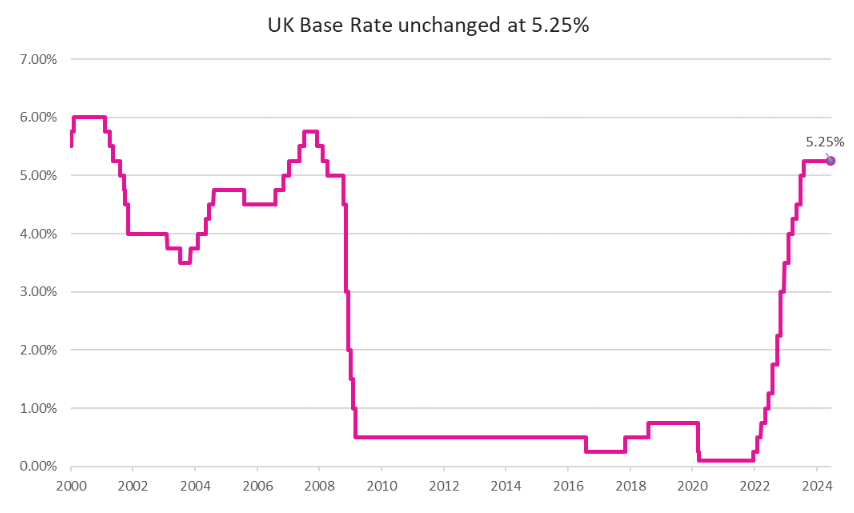

At the start of 2024, investors hoped that central banks would have started making multiple cuts to interest rates by now. While inflation has returned to more normal levels, it remains stickier and more persistent than expected. This has repeatedly pushed back on central banks’ ambitions to cut interest rates.

Investors remain focused on inflation readings in the hope they will inspire central banks to begin making changes to interest rates. The US Consumer Prices Index (CPI) measure of inflation came in at 3.00% for June, marginally down on the May print. There have also been indications that the jobs market is cooling, albeit from buoyant levels. The unemployment rate ticked up to 4.10% in June. Collectively, these respective dynamics have raised hopes of interest rate cuts in the US.

Officials from the US Central Bank and the Federal Reserve have echoed this sentiment. Recent comments have suggested that they do not need to wait for inflation to return the target level of 2.00% before easing monetary policy. However, it is not a clear-cut decision as economic growth in the second quarter was 2.80% annualised. This comfortably exceeded expectations of 2.10%. With economic growth being stronger than expected, central banks will feel less pressure to attempt to stimulate growth by cutting interest rates.

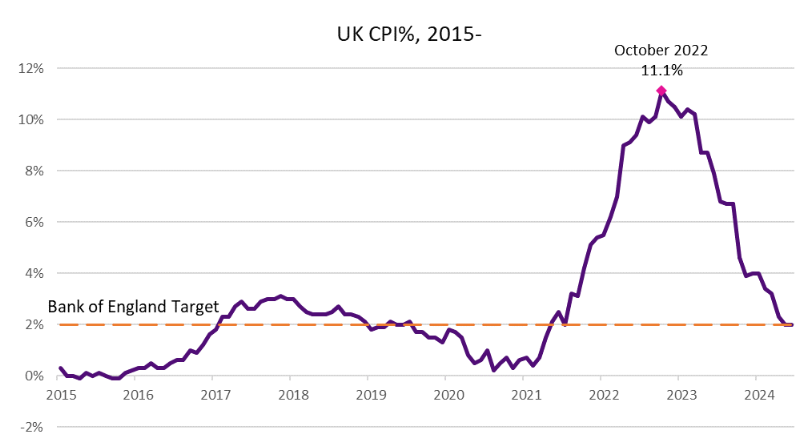

In the UK, the June CPI reading was unchanged from May at 2.00%. While this represents the second consecutive month in which inflation has been equal to the Bank of England’s target rate, policy makers remain cautious about pockets of inflation. Notably, for the UK as a service driven economy, services inflation specifically was recorded at a still elevated 5.70%.

After cutting rates in June, the European Central Bank, voted unanimously to hold rates in July. In similar fashion to the UK, officials noted elevated service sector inflation. Headline inflation in Europe is expected to remain above target into next year and September’s interest rate decision is said to be “wide open.”

Asia

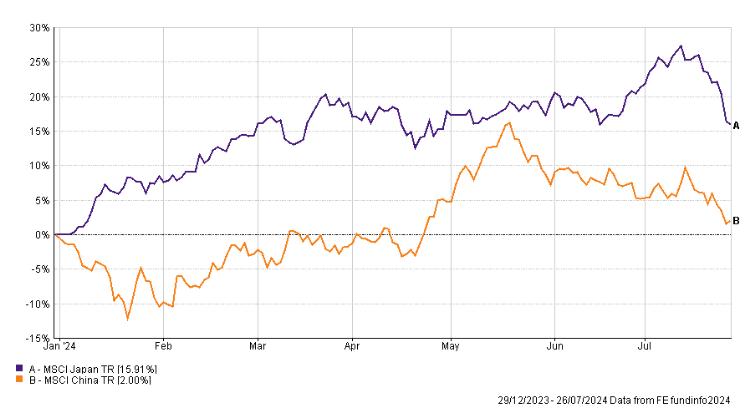

Japan’s Nikkei 225 index, a strong year-to-date performer, endured a run of daily losses in July that saw it retreat to its lowest level since April. In contrast, the Japanese yen has clawed back some ground against the US dollar. This has been driven by speculation that the Bank of Japan is poised to discuss raising interest rates and halving its bond-buying operations. In addition, a government panel has agreed to raise the average minimum wage in the country by 5%. All of which are seen as supportive measures for the currency.

In China, uncertainty about the future growth prospects and stability of the country’s economy has returned. China’s CSI 300 index has fallen back to its lowest level since February as investors fret over indifferent economic data. In efforts to stimulate demand, China’s central bank has cut both the medium-term facility lending rate and prime loan rates.