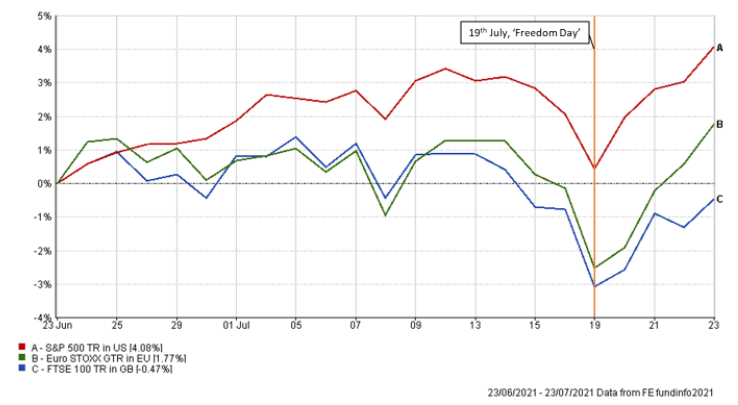

Delayed lifting of covid restrictions in England on 19th of July was met, perhaps only coincidentally, with a global sell off in stock markets over fears of rising case numbers of the Delta variant. European and US markets followed Asia losing almost 3% on the day while oil prices, which had traded bullishly for months, lost 7%. Markets have since recovered some of this lost ground however this highlights the volatility still present in markets amid worry that covid could once again derail much of the progress that has been made.

With over 70% of adults having received two doses of a covid vaccination, Britain’s vaccine programme is much more comprehensive than other countries who have tried to lift restrictions previously. It therefore offers a more thorough test of the real-world effectiveness of the vaccines. On a rudimentary examination of recent case numbers versus hospitalisations it suggests the vaccines are working to break the link between people contracting the virus and being subsequently admitted to hospital. However, that is not to say the number of hospital admissions resulting from covid is zero and it is a gamble, both politically and economically, whether now is indeed the right time to lift all restrictions.

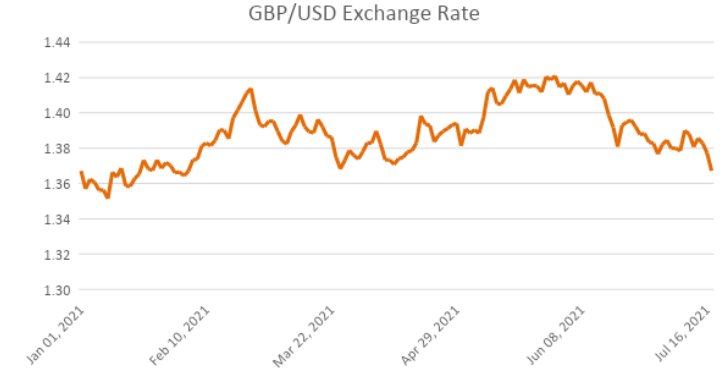

There was positive news in late July that case numbers were starting to fall however markets will closely monitor hospitalisation rates should the easing of restrictions cause a reversal of this trend. Any question over the efficacy of the vaccine should hospitals appear to be becoming overwhelmed will unsettle markets as that could pave the way for new and extended economic restrictions not just in the UK, but potentially worldwide. Uncertainty surrounding the UK as it continues its move out of lockdown is perhaps demonstrated by pound sterling falling to a 5-month low against the dollar of $1.36 as investors choose to wait on the side-lines to see the outcome of the UK experiment.

Inflation here to stay?

Inflation continues to be a concern for markets as it may force central banks to take action to manage it. We have written before that part of the reason why stock markets recovered so strongly from the initial onset of the pandemic has been supportive policies from central banks both in the lowering of interest rates and large asset purchase programs. If central banks reduce these supportive policies to combat inflation, it may remove some supports to stock market valuations along with it.

Whether central banks are forced to change policy seemingly depends on whether higher inflation numbers being recorded are a temporary phenomenon resulting from the economic recovery from the pandemic, or whether it is a more permanent fixture of economies in years to come. The difficulty in trying to predict the outcome to this question is that prices are not rising uniformly across the economy. Instead, rises are occurring at differing rates in differing sectors and for differing reasons.

Some prices are rising simply as a rebound from how they moved last year during the pandemic. Think of airline travel and hotels or even the fuel you put in your car which are seeing prices rise sharply simply as they return to more normal demand levels.

Some prices are rising simply due to limited supply and massively outweighed demand for example some commodity prices reached record highs earlier in the year and used cars have seen prices rise dramatically.

There are some prices that we can expect to remain higher permanently. Job openings have risen past pre-pandemic levels as employers particularly in hospitality sectors struggle to find staff. Filling these vacancies will require employers to pay more which will filter through to the prices we pay in the longer term.

For all the talk of rising prices though, some are not rising much at all. Rents, while demand for housing has been high due to the stamp duty cut and changing work preferences, have not increased dramatically more than what might be usually expected.

Prices are therefore not all rising at dramatic rates, and some are merely rising back to where they were pre-pandemic.

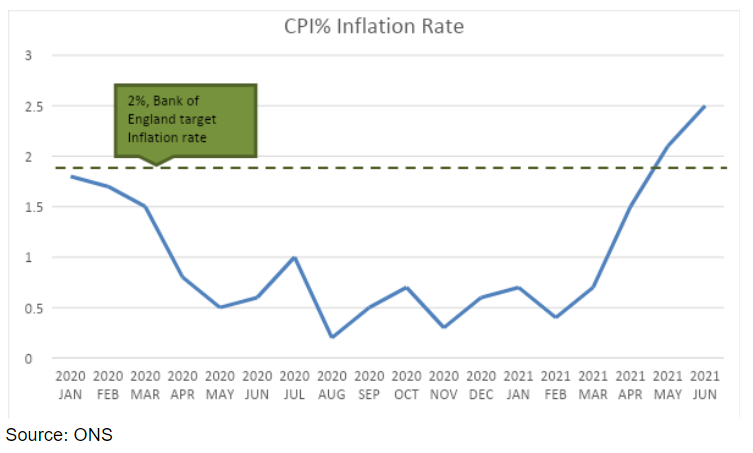

With a three-year high inflation number of 2.5% in June, markets will consider if the short-term transitory factors, such as the supply chain issues, might become more permanent fixtures like in wage growth. While inflation numbers are recording higher than in the very recent past, the overall numbers for the economy are returning to more normal levels and markets appear to be siding on the transitory side of the argument. If inflation measures continue rising further however this may cause a rethink when central banks are forced unhappily into action.

Invitation

If you would like to discuss your financial plan and investment strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.