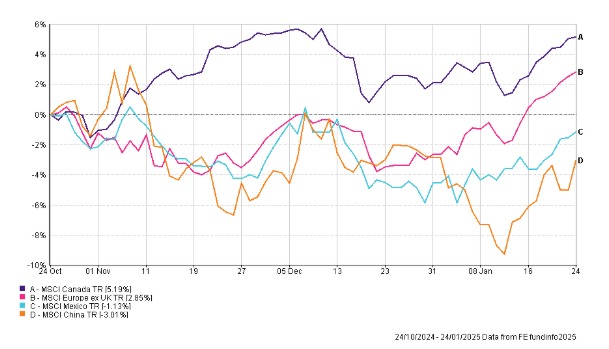

After enjoying a positive 2024, investment markets started 2025 facing a string of negative headlines. Sticky inflation, investor concerns about high government debt levels, and uncertainty surrounding the incoming President Trump were all areas of concern for investors. Despite the perceived headwinds, investment markets remain near all-time highs.

Bond Troubles

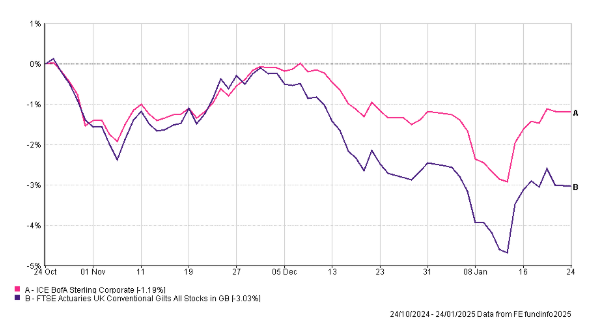

Bond yields were one area in sharp focus at the start of 2025. Yields had been rising globally for several months in response to global concerns about inflation. However, particular focus was placed on the UK in January.

The 30-year gilt yield reached a 27-year high and flirted with the 5.40% level. The 10-year yield touched 4.90%, the highest level since 2008. These rises had a negative impact on the value of fixed interest securities due to the way they are priced. The movement of bond yields is complicated, being driven by expectations of future interest rates and inflation and the stability and growth of economies amongst other factors. Markets exhibited concern that a combination of higher borrowing, low growth, and more elevated financing costs with higher yields, could cause Chancellor Rachel Reeves to breach her self-imposed fiscal rules. Simply, it could mean needing to borrow more money at a higher cost.

Political and economic commentators speculated that the rising bond yields have essentially eroded the fiscal surplus generated through the announced package of tax rises, most pertinently the increase in employers’ national insurance. In the absence of substantial spending cuts, or further tax increases, some forecasters suggested that Reeves’s fiscal room for manoeuvre has greatly diminished. The Treasury has pushed back, reiterating their commitment to fiscal discipline and the prioritisation of economic growth.

There was relief for the Chancellor and for markets following reporting of December inflation data. The Consumer Prices Index (CPI) measure of inflation fell to 2.50%, down from 2.60% in November. Other positive news came as the UK economy was estimated to have grown 0.10% in November, the first expansion in three months. The market took both data points as broadly positive. Sterling found some stability, and gilt yields fell as quickly as they had risen providing a boost for investors.

The economic picture, as in other developed markets, is mixed. Wage growth in the UK in the three months to November was 5.60%, with private sector growth at 6.00%. This is a healthy indicator for consumer finances, as the rate of growth sits above that of inflation. Conversely, there are developing signs of labour market weakness ahead of tax increases on employers with surveys of business and consumer confidence suggesting a degree of fragility.

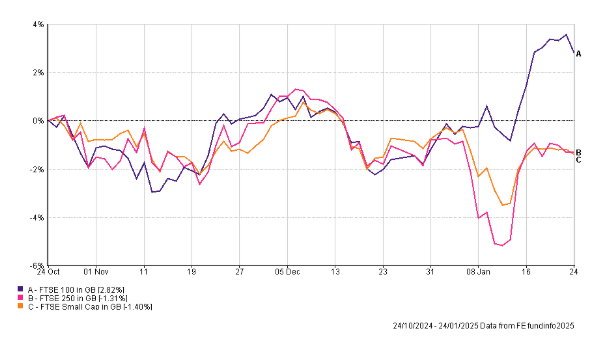

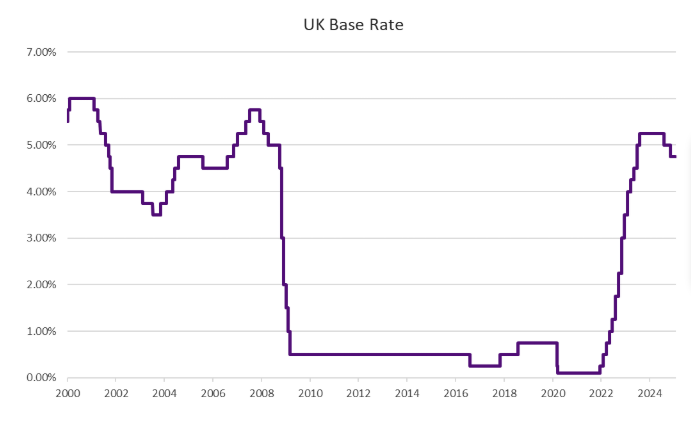

Despite the challenging fiscal and economic backdrop, investment markets remain buoyant. The FTSE 100 started the year positively reaching a new all-time high. There will be much anticipation around the next meeting of the Monetary Policy Committee of the Bank of England on 6th February to determine the future path of interest rates.

Top Trump

As the month progressed, attention turned towards the inauguration of President Trump. Trump used his speech to reiterate many of his much-discussed policies and promptly set about signing a raft of executive orders. Early rhetoric, and suggested policies, have been supportive of artificial intelligence and cryptocurrency.

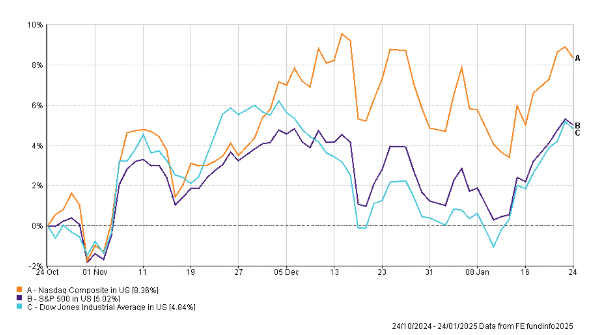

Trump’s rhetoric is very fluid which presents challenges for investors. Assumed support for a country or asset class can be completely removed in a tweet. It is therefore difficult for investors to have certainty. Despite this, continuing investor enthusiasm for the US saw the S&P 500 once again hit record territory.

Trade tariffs remain a central negotiating instrument. Whilst it is still very early days, there have been some interesting trends. When addressing delegates at the World Economic Forum in Davos, Trump appeared to express more grievances about the European Union, while being more conciliatory towards China. In the context of his own plans to drill for more fossil fuels, he expressed the desire for a lower oil price.

Perhaps more controversially, President Trump suggested he would demand immediate lower interest rates. This raises interesting questions over both the independence of the Federal Reserve, and his relationship with the Chair, Jerome Powell. The US dollar weakened following these comments