Equity markets finished 2023 in strong form. Investors have taken encouragement from moderating inflation and have priced in a series of interest rate cuts in the year ahead. Despite the volatility and uncertainty that investment markets experienced throughout the year, this enthusiasm delivered a positive return for most asset classes.

Strong gains

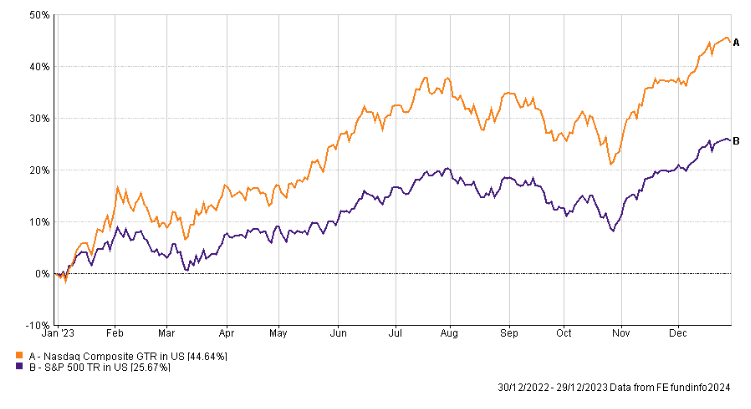

Gains, however, were far from uniform. The S&P 500, the flagship US equity index, gained over 25% in local currency terms, surpassed by the technology-heavy Nasdaq Composite index, which soared by nearly 45%. The latter being powered by the ‘magnificent seven’ of Alphabet (Google), Amazon, Apple, Meta (formerly Facebook), Microsoft, Nvidia and Tesla. Investors were also enthusiastic about any company able to participate in the broader theme of Artificial Intelligence (AI).

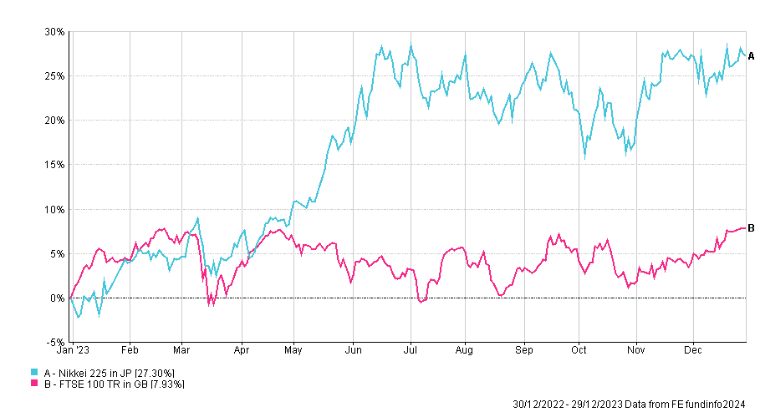

The FTSE 100, with no notable technology constituents, delivered mid-single-digit total returns. Further east in Japan, a corporate renaissance, with a sharper focus on shareholder returns, powered the Nikkei 225 to local currency returns of 27.30%. Momentum for both US and Japanese equities continued into the early weeks of 2024. The S&P 500 established new record highs, and the Nikkei 225 reached its highest level for 34 years.

A tale of two countries

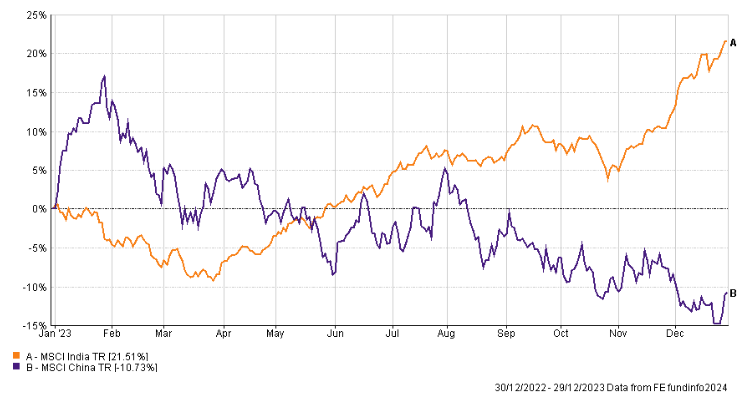

The developing markets also saw a schism of returns from two large members. The MSCI China index declined by -10%, while Indian equities closed 2023 with gains of 21%. China is facing a difficult adjustment to becoming one of the largest global economies. Its economy is still growing, but the recently announced GDP growth of 5.20% in 2023 is a slowdown in the rate of growth when compared to before the pandemic.

Chinese stock market woes can be attributed to investor scepticism given the well-documented difficulties confronting the influential real estate sector. Alongside this, and more worrying for future economic growth, has been the muted recovery in consumption following the reopening of the economy after the pandemic and associated lockdowns.

The Chinese authorities, mindful of the impact that poor real estate and stock market returns can have on a populace, have announced two initiatives. First, a plan to mobilise circa two trillion yuan (£222bn) from the offshore accounts of state-owned enterprises, to arrest a decline in equity prices. Second, a 0.50% cut in the bank reserve ratio, potentially boosting the availability of credit within the economy. Both initiatives could deliver notable results in the short term; however, broader structural issues will likely require more imaginative solutions. In India, Prime Minister Narendra Modi’s blend of business-friendly policies and Hindu nationalism has pleased investors and also bodes well for an expected election in 2024.

Inflation on the rise?

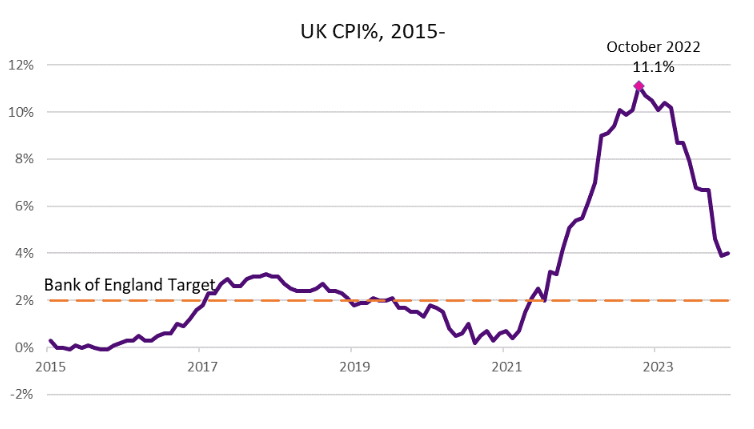

Inflationary pressures, while somewhat reduced from the early months of 2023, continue to occupy the minds of both central bankers and investors. The last yards in restoring inflation to target levels in developed economies are proving a challenge. Indeed, the most recently reported inflation data actually showed a small increase in inflation when compared to the previous month.

US CPI inflation for December was recorded at 3.4%, compared to 3.1% in November. In the UK, CPI inflation rose to 4.0% compared to 3.9%. While in the Eurozone, CPI inflation was recorded at 2.9% compared to 2.4% in the previous month.

Inflationary pressures have certainly abated, but they have not disappeared. Many businesses have warned in recent trading updates that energy and labour costs remain far higher than pre-pandemic levels. The latter is unlikely to offer any immediate relief, with a 9.60% increase in the National Living Wage scheduled for April 2024. In a wider context, continued disruption to global shipping, owing to tensions in the Red Sea, may also add complications to the inflation landscape.

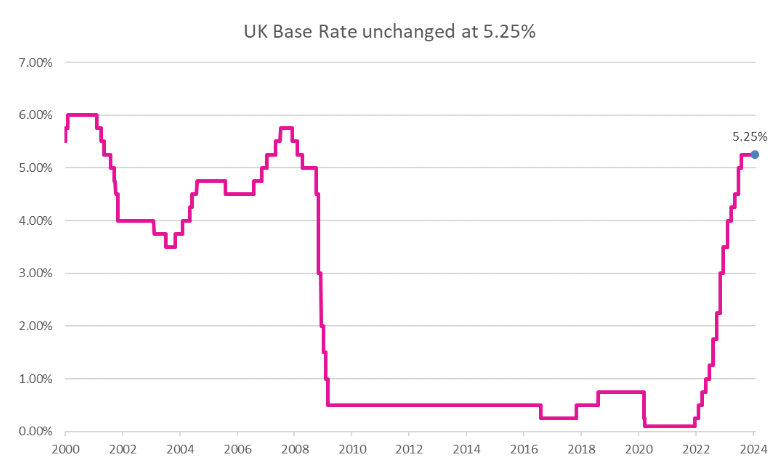

The strong performance of investment markets in recent months can be tied to investor hopes that central banks may begin cutting interest rates in 2024. However, this was not to be in January. Despite a plethora of disappointing economic data across the eurozone, the European Central Bank (ECB) left the key benchmark interest rate unchanged at 4% at its January meeting. The Bank of England will next meet to discuss interest rate changes at the start of February.

The US economy, in contrast to the EU, finished 2023 in fine form, growing at an annualised rate of 3.30% in the fourth quarter supported by higher consumer spending. This raises hopes of a soft landing (controlling inflation without causing a recession) despite the Federal Reserve raising rates to a 22 year high. Investors hope that falling inflation may allow the Federal Reserve to move ahead with the interest rate cuts hinted at in late 2023. However, the recent inflation data showing a slight increase in the rate of price rises has complicated this view. The irony for investors is that while they are hopeful that interest rates will fall, central banks are likely to be more favourable to doing so if economic growth is weak, or even negative.