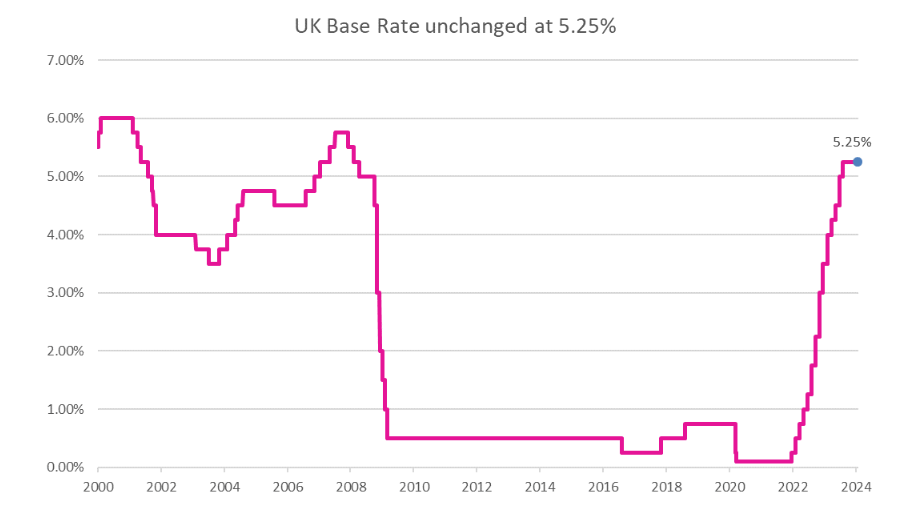

January ended with the first meeting of 2024 of the Bank of England’s (BoE) Monetary Policy Committee (MPC). Investors had been anticipating this for guidance on the future direction of interest rates in the UK in the months to come. Despite hopes for interest rates to start falling in early 2024, the BOE left the base rate unchanged rates at 5.25%.

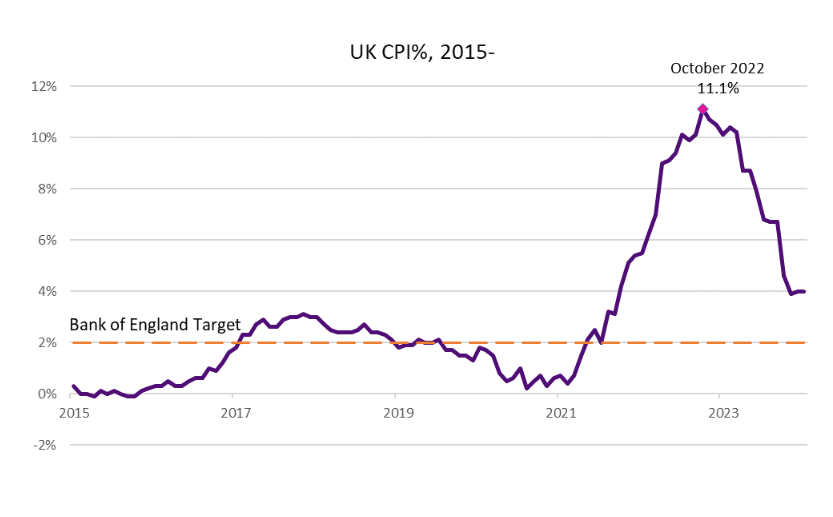

This meeting set the scene for a busy month of economic data for investors to digest. UK inflation is still stubbornly above target with the consumer prices Index (CPI) reading in January remaining unchanged from December’s reading at 4.00%. There remains continued divergence between the rate of prices rises of goods and services within the data. The CPI goods inflation reading fell from 1.90% to 1.80%, meanwhile CPI services inflation climbed from 6.00% to 6.10%. As a service sector focused economy, the figures served a reminder that inflation in the UK is far from tamed. The BoE have forecasted that inflation will fall to the target rate of 2% in the coming months, before increasing again towards the year end.

Technical Recession

Beyond inflation, the UK economy was estimated to have shrunk by 0.30% in the fourth quarter of 2023, following a decline of 0.10% in the third quarter of the same year. This placed the economy into a ‘technical’ recession, defined as two consecutive quarters of negative growth. While this headline appears alarming, this differs from an actual recession usually characterised by a sharp rise in unemployment.

Looking forward there is a degree of optimism for the UK economy. There was better news for retail sales which expanded by 3.40% in January. This was the largest monthly increase since April 2021, following a weak reading in December 2023. Unemployment remains at historically low levels, and wage increases are outpacing the general rate of inflation. Industry data, such as the purchasing managers’ index, also appears to suggest the services and manufacturing sectors are expanding. The shallow technical recession at the end of 2023 may prove to be short-lived.

Positive Returns

Despite the uncertainty surrounding the future path of interest rates and mixed economic data, investment markets have continued their positive momentum into early 2024. In the US, the S&P 500 index closed at a new record high with continued optimism for technology and AI companies. This performance has been volatile however as a result of the uncertain outlook for interest rates and their impact on economies.

Investors are divided over the power and the concentration risk of the much vaunted “magnificent seven”, comprising Alphabet (Google), Apple, Amazon, Microsoft, Meta (Facebook), Microsoft, and Tesla. Research by Deutsche Bank estimated that the combined profits of these seven companies greatly exceed those attributed to all UK listed companies. It is the performance of these companies that has driven US stock markets to new record highs, despite the middling performance of other US companies. The concern for investors is the potential negative impact on US stock markets if these companies begin to underperform.

Despite these concerns, Nvidia more than justified its current valuation with stellar fourth quarter 2023 results. The microchip giant comfortably beat analyst forecasts for both revenue and earnings, with the company also issuing strong guidance for the current quarter and beyond. Nvidia’s total revenue soared by 265% year on year, and it is this growth that has driven the company’s share price increasingly higher. The challenge for investors is assessing how far in the future such a growth rate can be maintained, and what value to place on it?

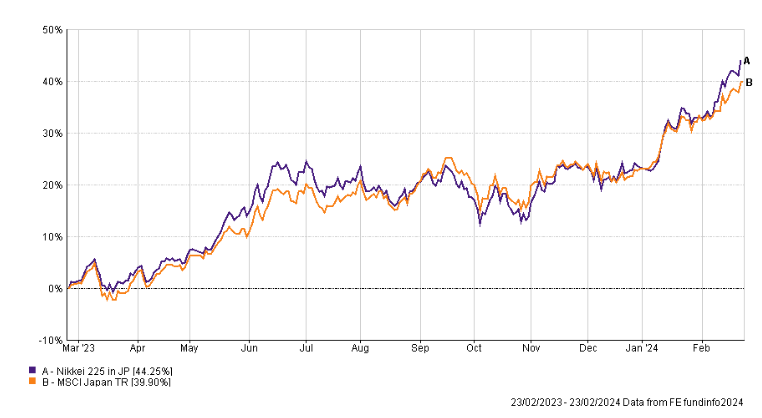

Japanese equities also continued their impressive run. The Nikkei 225 index has risen more than 10%, year to date, in local currency terms. This performance helped the index establish a new high of 39,156.97, topping the previous record dating back to 1989. Investors remain enthused by the earnings profile of Japanese businesses, following a sharper focus on improving return on equity and the delivery of shareholder value.

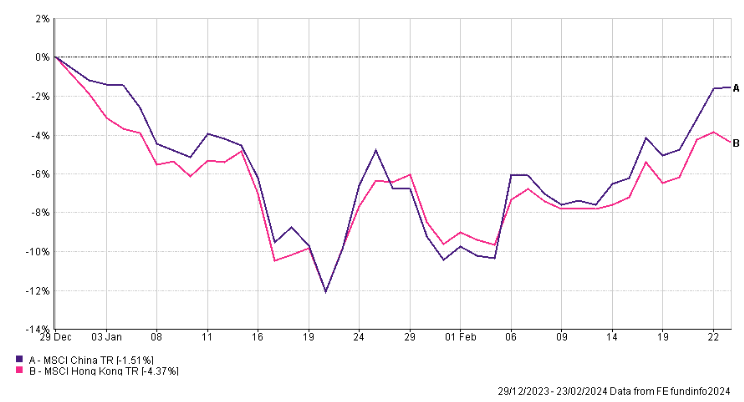

After a difficult year for Chinese equities, the leading Chinese stock market indexes rallied in February following the introduction of supportive measures announced by the Chinese authorities. In addition to these measures, spending was reported to be robust over the Chinese Lunar New Year period. This was the first celebration in the country to not be affected by covid restrictions since 2019, and investors hope this could be a boost for economic growth. Investors will however be keen to monitor the extent to which any momentum continues amid concerns about structural weaknesses in the real estate sector.