Note that the following article was published on 23rd February 2022 and that the situation is rapidly developing.

The biggest concern for investment markets in recent weeks has been the ongoing situation on the eastern border of Ukraine, and the resulting fears of armed conflict in the region. Investment markets have been volatile in February as rumours swirled surrounding the legitimacy of any invasion plans. Falling on any news of impending military action, while rising on reports suggesting an easing of tensions.

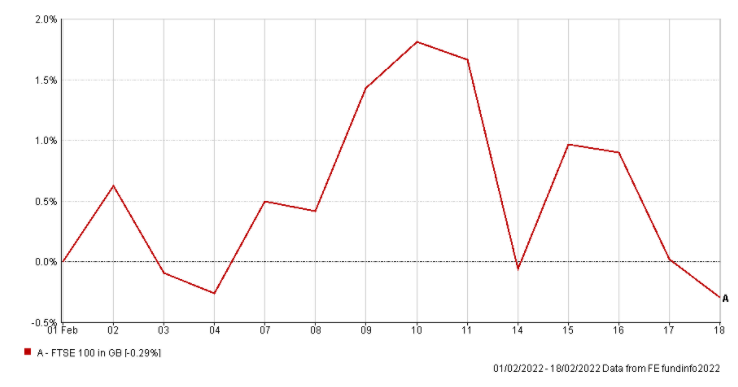

This volatility was notable on Valentine’s Day with news reports over the previous weekend suggesting the US had ‘intelligence’ that Russia was planning to invade on the coming Wednesday. This worried markets and, as can be seen, the FTSE 100 experienced a fall of 1.70% on the news. It was later reported this was merely a sarcastic comment made by the Ukrainian President and the FTSE recovered 1.00% the following day alongside news of a supposed reduction in the Russian military presence near the border.

Volatility has been a result of investment market concern about the potential economic impact following any intervention. The global response at the least would likely be heavy economic sanctions. This introduces a greater level of uncertainty and would create barriers to trade, impacting global economies as the world already faces pressure with rising inflation, particularly in energy markets.

Tensions escalated in late February following President Putin’s recognition of the eastern separatist-held regions of Donetsk and Luhansk as independent entities. Alongside this came the order of Russian armed forces into these regions to perform “peacekeeping functions”. At the time of writing, the move has been widely condemned and several countries, including the UK, are considering what sanctions to impose against Russia in response to the move.

The immediate market response to the movement of Russian troops into the Donbas region was volatile but understated. Russian equity markets perhaps understandably faced the biggest sell-off on the news, given the biggest economic impact of sanctions will likely be felt by the Russian economy. Neither East nor West have anything to gain by a full-scale war which can hopefully be avoided.

Inflation

Alongside the geopolitical tensions in Eastern Europe, the inflation debate continues to cause volatility within markets. Investors have been concerned for some time that rising inflation would force central banks to make changes to accommodative policies that have boosted the economic and market recovery since the start of the pandemic.

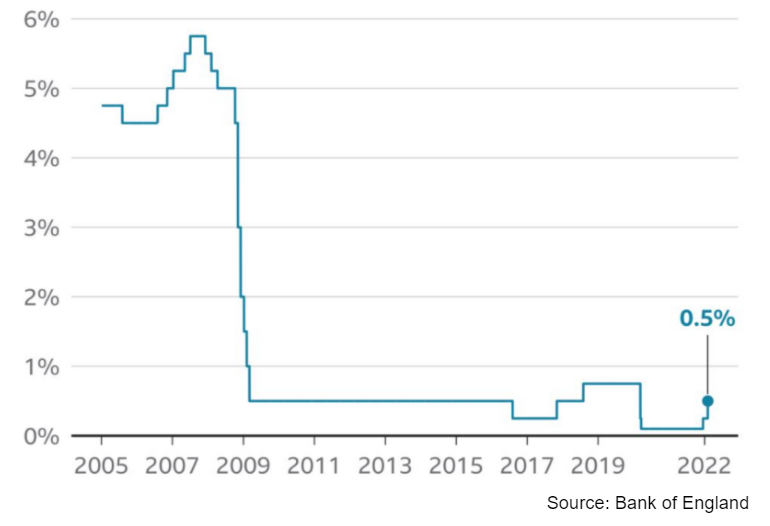

The Bank of England (BoE) has been at the forefront of developed market central banks in making these changes by raising intertest rates. February saw the 2nd rise in 3 months with the bank once again making the decision to raise the base rate. This time increasing it to 0.50%. While this returns the base rate to the level it was for much of the decade following the global financial crisis in 2008, it remains well below historic levels.

The motivation behind these moves is to attempt to limit rising inflation which continued to rise in January; UK CPI inflation measured at a 30-year high, 5.5%. This heightened level of inflation is also before the energy price cap is set to rise in April which is when some are forecasting inflation to ‘peak’.

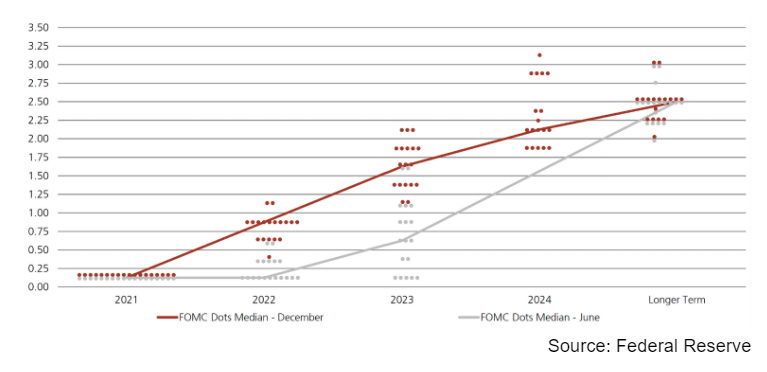

Inflation is not just limited to the UK and is an issue impacting economies globally. Inflation in the US reached a 40-year high 7.5% in January leading to expectations that the US central bank, the Federal Reserve, might bring forward interest rate rises of their own. Following guidance from the Federal Reserve, investment markets are now forecasting interest rates in the US to be around 1% by the end of the year. Here in the UK, financial markets are pricing in the BoE raising the UK base rate further to around 1.25% by November 2022.

The actual impact these interest rate changes might have on controlling inflation is unclear. Supply chains continue to face pressures; while consumers continue in many instances to spend savings accrued during lockdown periods. Raising interest rates has no impact on areas such as food and energy prices so it is difficult to forecast whether hawkish monetary policy will have a substantial impact on inflation. Despite this, and with inflation forecast to remain high at least in the near future, central banks feel that they have no choice but to take action. Even if those actions might be futile.

The concern for investment markets is how inflation, and the attempts to control it, impact on economies and the companies within them. High growth companies, notably ‘tech’ stocks, have felt the biggest impact of rising interest rate expectations as their high valuations appear harder to justify with traditional valuation models. ‘Value’ companies, previously out of favour in the post-pandemic recovery, have been more resilient in the face of rising interest rate expectations.

It is impossible to forecast both the outcome of the situation in Ukraine and how markets will continue to react to persistent inflation. However, the resulting volatility within markets highlights the importance of diversification. Holding a range of different asset classes can protect your overall portfolio against severe market falls, while offering the opportunity to benefit from opportunities when markets rise.

Invitation

If you would like to discuss your financial plan and investment strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.