It has been a challenging post-budget period for the UK economy. Despite economists forecasting modest growth, the Office for National Statistics (ONS) estimated that the UK economy shrank by -0.10% in October. The second month of contraction.

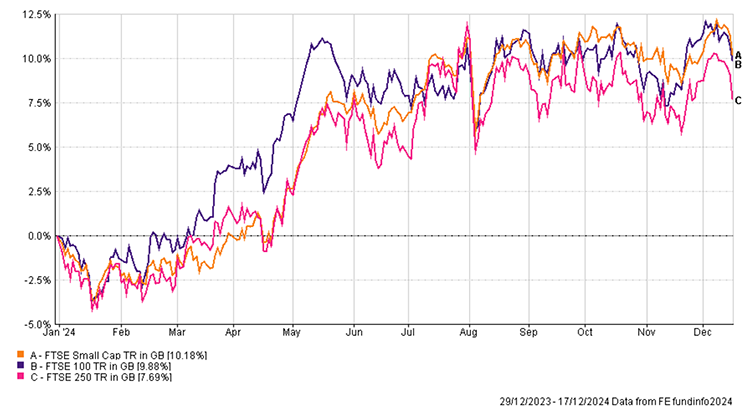

It is too early to call a recession. An economy is in technical recession following two consecutive quarters of negative growth, not just months. The UK’s gross domestic product (GDP) for the third quarter expanded, albeit, by a pedestrian 0.10%. With declining growth readings in recent months however the prospect will remain a concern for the new government. Regardless of economic concerns, the UK stock market has enjoyed a positive year.

Higher for Longer

Bond yields have moved in a volatile fashion in recent months. The Autumn budget in October, with the announcement of increased borrowing, and the victory of Donald Trump in the US presidential election were two events investors regarded as being potentially inflationary. With expectations of persistent inflation, bond yields rose in November before declining into early December.

Moving through December however, bond yields in the UK once again rose sharply. Firstly, the ONS recorded wage growth in the three months to October, excluding bonuses, at 5.20%. This was ahead of expectations of 5.00%.

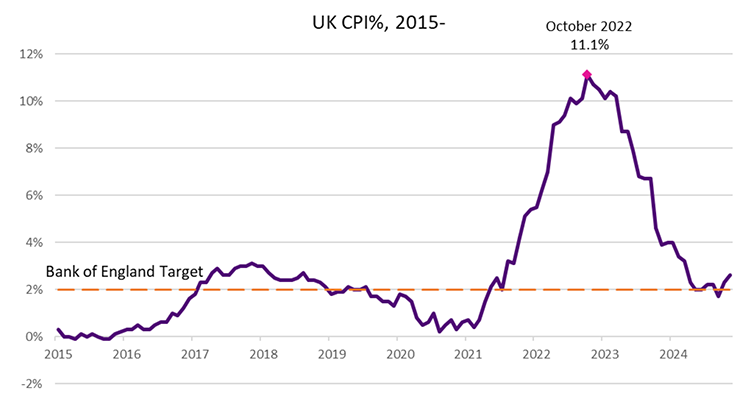

Closely following this announcement were UK inflation readings. The headline UK Consumer Prices Index (CPI) for November came in at 2.60%. An increase from 2.30% in October. The largest upward contributors being transportation and housing & household services.

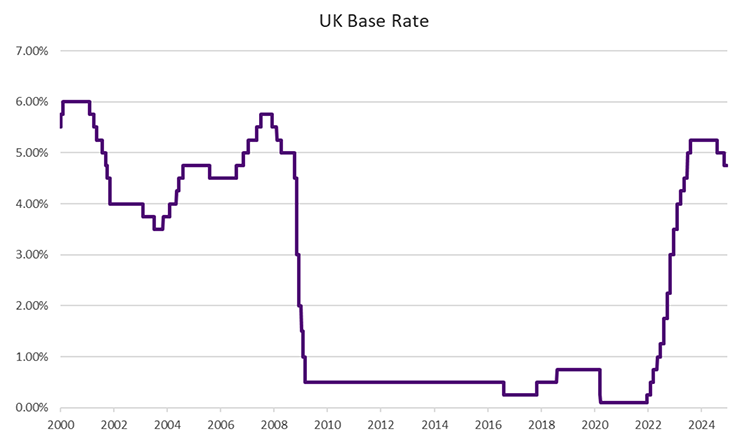

Higher wages and rising inflation mean investors now expect the Bank of England to cut interest rates at a more gradual pace. It is this reason why yields have risen so sharply as investors are now projecting that interest rates will remain higher for longer due to these inflationary pressures. The Bank of England made no change to the Bank Rate at its meeting on the 19th of December, maintaining interest rates at 4.75%.

European Markets

Earlier in December, The European Central Bank made a further 0.25% reduction in interest rates to 3.00%, the fourth such cut this year. The accompanying narrative was dovish in tone with the bank citing challenges to growth and falling inflation. The dovish stance, along with the potential impact of trade tariffs levied by the incoming Trump administration, has prompted investors to revise their assumption as to what represents a neutral rate of interest for the Eurozone. Further cuts are expected at future meetings.

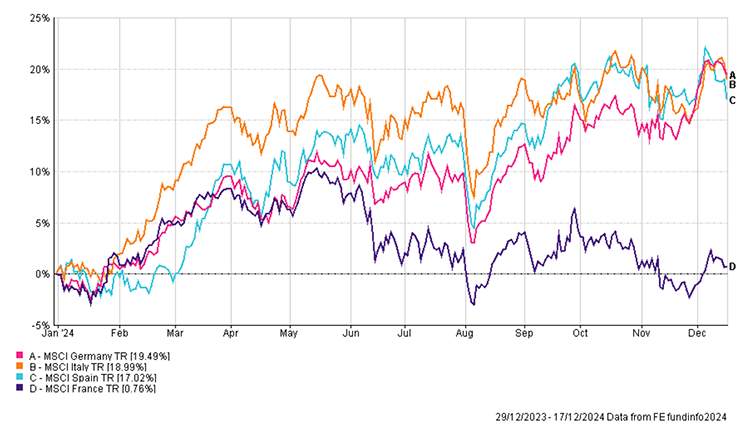

The political backdrop in Europe is also turbulent. In France, Prime Minister, and former Brexit negotiator, Michel Barnier, lost a vote of no confidence prompting him to resign. In seeking to tame the influence of National Rally, President Macron appointed political ally Francois Bayrou. He now faces the daunting task of trying to succeed where Barnier failed; passing a contentious budget amid stretched public finances. Meanwhile in Germany, Chancellor Olaf Scholtz took the unusual step of calling a confidence vote whilst urging peers to vote against him. This would clear the path for elections which are expected in February 2025.

Eyes on Trump

President-Elect Donald Trump continues preparations to assume office in January 2025. The Chair of the US Federal Reserve, Jerome Powell, reaffirmed that he would not step down early if asked to do so by Donald Trump, given their fractious relationship during his first term of office. Trump has since stated that he intends to allow Powell to serve the remainder of his term, offering stability to financial markets. The Federal Reserve delivered its latest interest rate decision on the 18th of December cutting rates by a further 0.25%.

Investors reacted positively throughout November to the election victory of Donald Trump however there has since been some divergence in the performance of respective US markets. The technology heavy Nasdaq index established new highs at the start of December. The Dow Jones Industrial Average index on the other hand registered its longest losing run since 1978, albeit following a series of shallow daily declines. Comments made by the Federal Reserve following their interest rate cut suggested there would be fewer cuts next year and investors in all markets reacted negatively to that prospect.

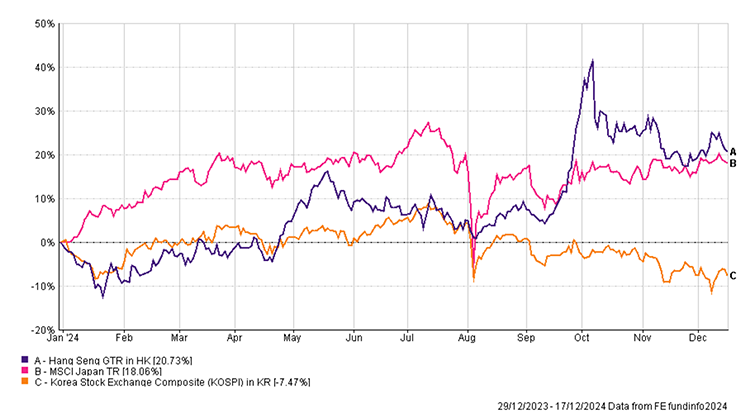

In Asia, South Korea’s main stock market, the KOSPI index, declined after a failed attempt by the country’s president to impose martial law. The decision was made following perceived nefarious actions by North Korea. The attempt was short-lived, and the President now faces an impeachment trial. After three consecutive years of declines, the Hong Kong Stock Exchange saw a big jump in new companies listing on the index. Commentators have suggested that confidence is returning to the territory, with the Heng Seng Index on course to record healthy gains for 2024.