After a challenging year, investment markets are in their own state of festive cheer. Following recent market movements, it appears likely that most markets will end the year in positive territory. With inflation appearing to be falling, and early suggestions that interest rates may fall next year, November’s newfound investor optimism has continued into December providing a boost to investor portfolios.

A Volatile Year

For most of 2023, markets have grappled with the push and pull of inflation and the response of central banks in their attempts to control it. High inflation, the cost of living crisis, and rising interest rates are related issues that have combined to deliver a difficult and challenging year for investors. Investment markets do not like uncertainty and these issues have resulted in a high degree of volatility for markets, continuing from a difficult 2022.

In the last twelve months, when data has pointed to inflation remaining stubbornly high, investors reacted negatively, and markets fell on the assumption interest rates might need to remain higher for longer. However, when inflation data appeared to show prices rising at a slower rate, this provided a boost to investors. The hope being that it may give central banks scope to pause interest rate rises, or even begin to lower rates. As 2023 draws to a close, it is this latter sentiment that is dominating the investment narrative and markets have delivered strong returns, most notably in the US.

A fall in interest rates

What has driven the US stock market higher, and in the case of the Dow Jones index to record highs, has been a potential pivot in central bank policy by the Federal Reserve. After 11 increases in the US Federal Funds Reserve Rate from essentially 0.00% to a target range of 5.25-5.50%, investors had hoped all year that signs of lowering inflation could prompt more supportive policy from central banks. Now, what was previously a hope for investors, instead appears to be more of a reality.

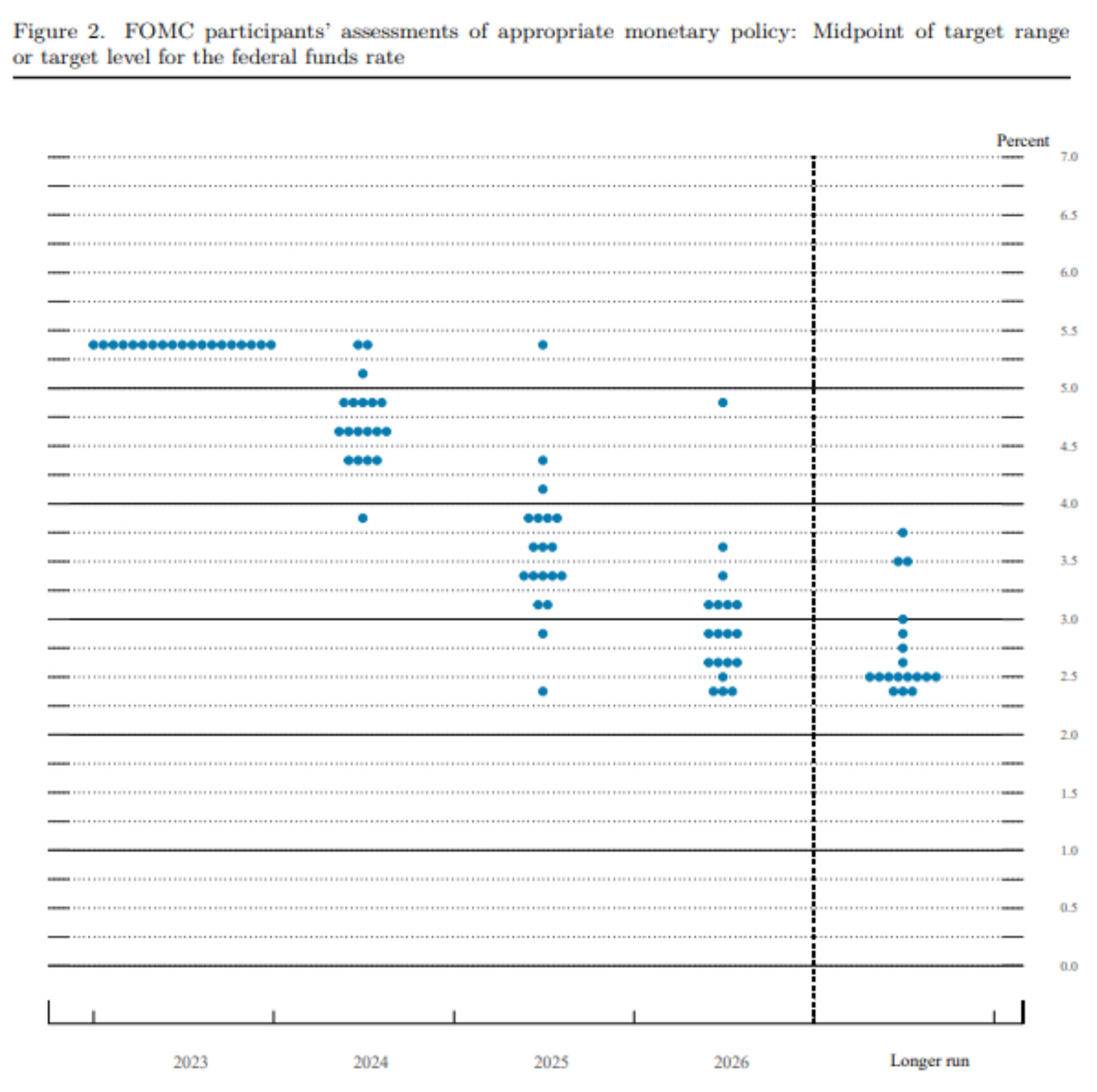

Source: Federal Reserve, Summary of Economic Projections (2023)

Falling inflation has prompted members of the US Federal Reserve to change their opinions on the future path of interest rates. This was confirmed in the minutes released following the meeting of the Federal Reserve earlier in December. Updated ‘dot plots’ showed a consensus view that interest rates could be cut three times next year. Financial markets believe this might even be four.

Further comments made by the Federal Reserve have given further signs of future rate cuts. This has provided a boost to investor optimism on the hope of more supportive market conditions in 2024 with lower inflation and interest rates.

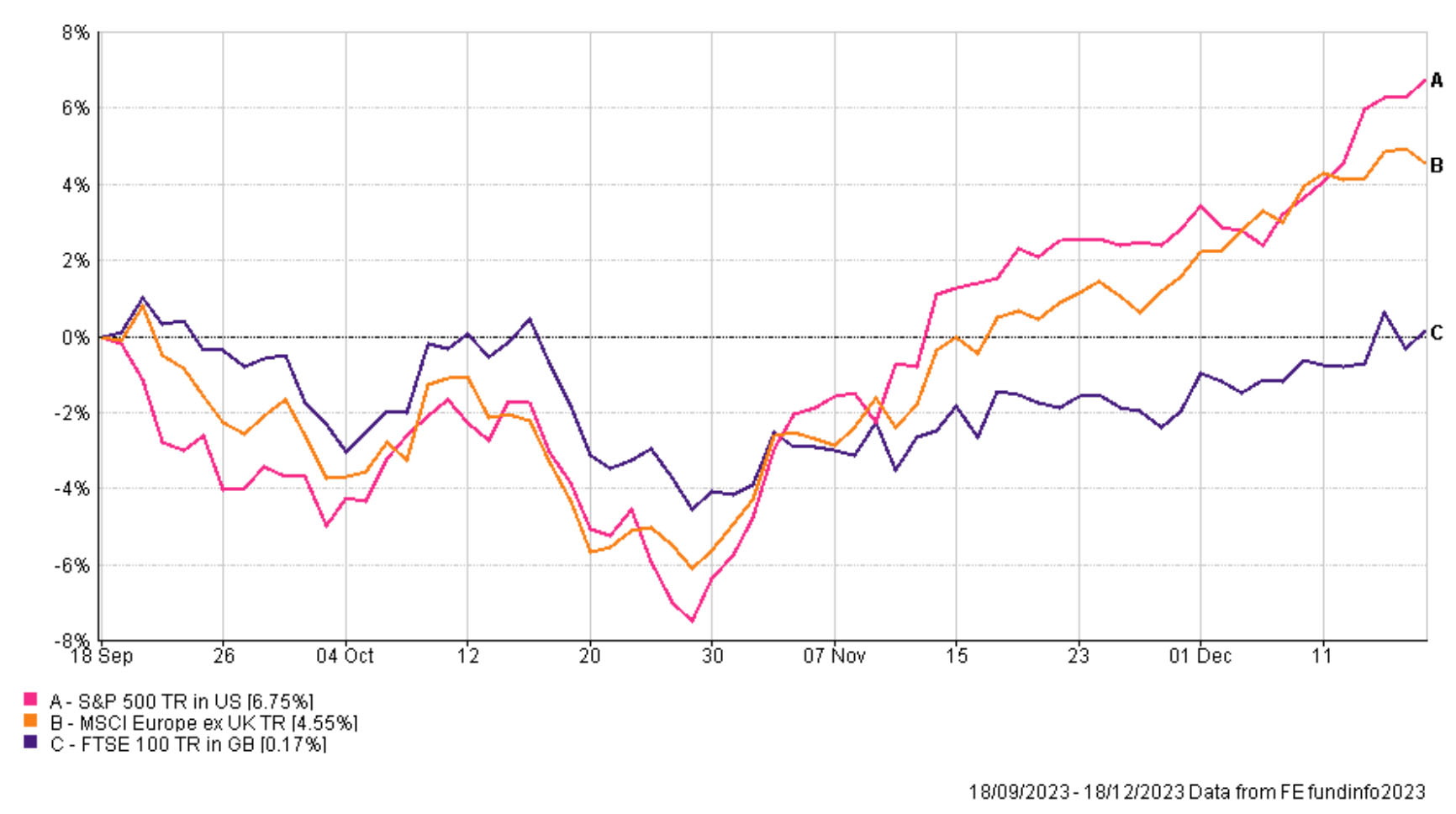

US vs Europe

Since the start of November, developed markets globally have mostly all delivered positive returns following this change in investor sentiment. However, it has been apparent in recent weeks there appears a divergence in central bank policy on either side of the Atlantic. The Federal Reserve has given dovish signals and made little effort to counter any market expectations for rate cuts. The Bank of England (BoE) and the European Central Bank (ECB) on the other hand have given more neutral guidance.

Following the respective meetings at the start of December, the chairpersons of both institutions warned investors not to expect rate cuts in the immediate term. Andrew Bailey (Governor of the BoE) stated “it’s really too early to start speculating about cutting interest rates” and Christine Lagarde (President of the ECB) suggested that rate cuts were “definitely” not discussed at the most recent meeting.

Despite these comments, investor optimism in the respective markets remains high. Both UK and European markets have delivered positive returns in recent weeks. In the UK, this is particularly true for the more domestically focused FTSE250, often viewed as being more representative of the UK economy. With UK CPI inflation recorded at 3.9% in November, it may add to pressure on the BoE to cut interest rates in 2024.

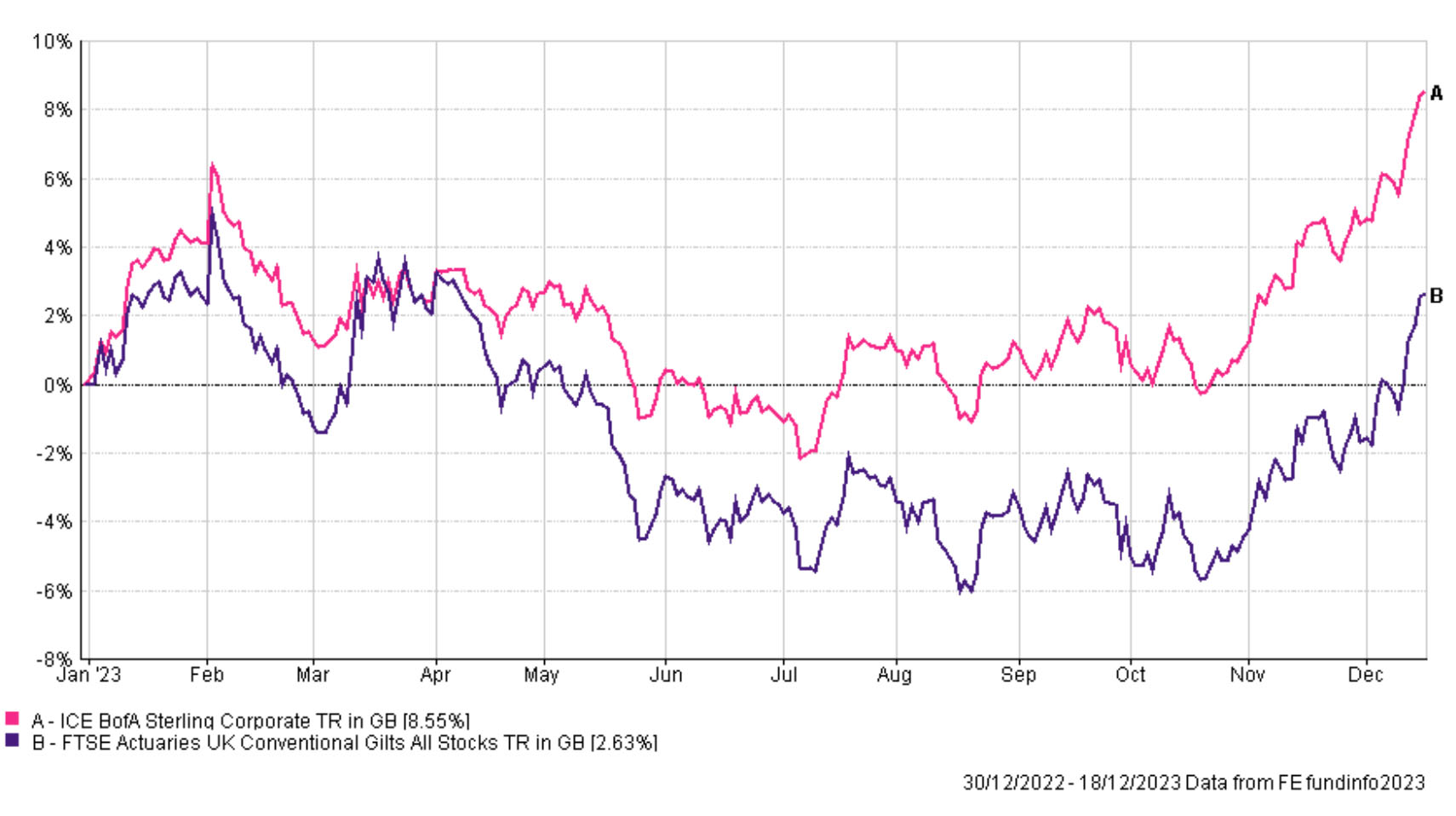

A boost for bonds

One area of financial markets particularly benefiting from the changing expectations of central bank policy is the capital value of bonds and other fixed interest investments. These investments, traditionally seen as lower risk, had suffered large losses in the past two years as interest rates rose. The way that fixed interest investments are priced means that as yields (the interest rate an investor receives for holding a bond) rise, the value of the bond fell to compensate. Investors, particularly those in lower risk portfolios which hold a greater proportion of fixed interest investments, have witnessed first-hand the impact of this on the value of their investments.

In a boost for investors holding these assets however, the changing expectations has started to reverse this trend. With the recent moves in bond yields, investors in lower risk portfolios are now holding assets offering a higher yield, with the potential for capital appreciation if interest rates fall. In the long-term this could provide an overall boost to performance despite the short-term pain of the last two years.