August has proved highly volatile for investment markets. Investor concerns about the fragility of the economy resulted in sharp falls at the start of the month. However, more favourable economic data alongside the promise and expectation of upcoming interest rate cuts prompted a market recovery, with indexes such as the US Dow Jones reaching new record highs.

Fall and rise

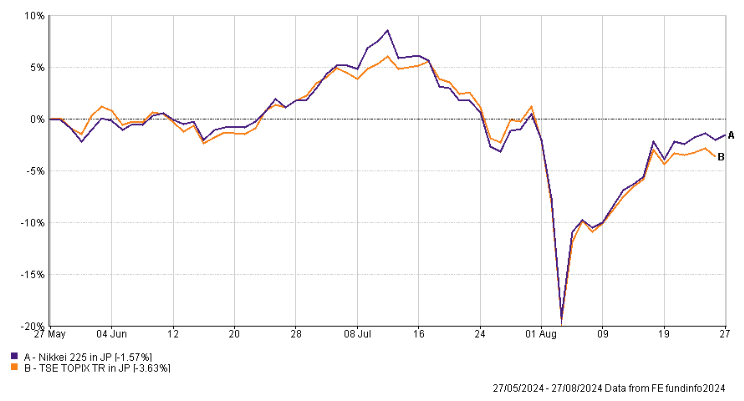

This pattern was most evident in Japan with the country’s Nikkei 225 index falling more than 12% in a single day. This was the biggest daily decline suffered by the index since 1987. There were a variety of factors at play. Principally, the tightening of Japanese monetary policy by the Bank of Japan alongside concerns about a US economic slowdown.

The changes to monetary policy disrupted a long running, and lucrative, ‘carry trade’. This entails traders borrowing cheaply in yen, and investing in higher yielding assets elsewhere. With changing expectations of future interest rates, this impacted on the demand for Japanese assets with concerns that a slowdown in the US could reduce global demand for goods produced by Japanese companies. The market has since stabilised, with investors resuming their focus on improving corporate governance and more efficient uses of capital.

Interest Rates

As other equity markets recovered from the initial bout of volatility, emphasis shifted back to the timing of interest rate cuts and broader monetary policy easing. Weakening employment data in the US economy prompted investors to tighten their focus on the US central bank, the Federal Reserve. The thinking being that a faltering economy could provide the motivation to cut interest rates to stimulate demand.

Speaking at the closely watched Jackson Hole Symposium, a meeting of the world’s most prominent central bankers, Federal Reserve Chair, Jerome Powell, reaffirmed the widely anticipated pivot in monetary policy. It is now widely expected that the Federal Reserve will join the Bank of England and European Central Bank in commencing a program of interest rate cuts in September.

The velocity of cuts, however, is subject to fluid debate in financial markets. While a cut in interest rates is expected, investors are looking to economic data for signals of whether the first decrease will be 0.25%, or 0.50%. Whilst this may appear somewhat frivolous, its importance rests in the degree of concern expressed about emerging labour market weakness.

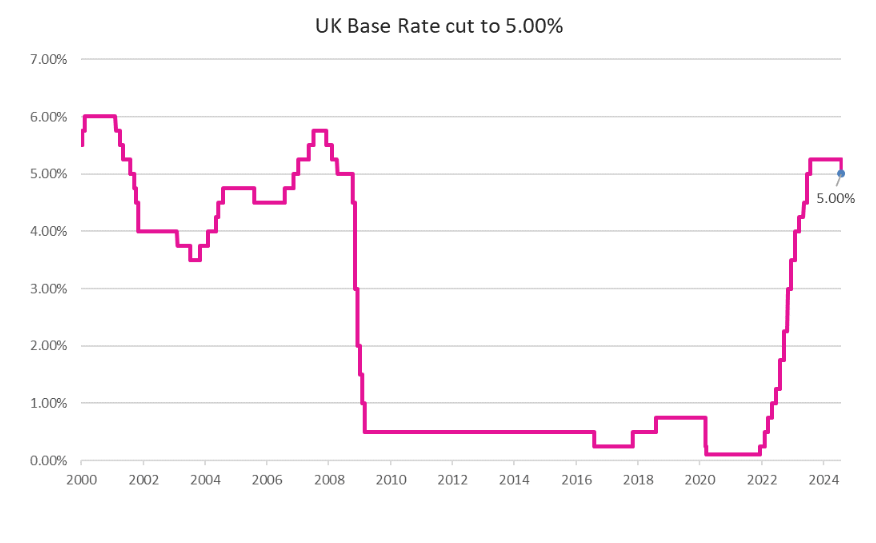

In the UK, the Bank of England cut interest rates from 5.25% to 5.00%. This was the first reduction since 2020, when the UK economy was facing the initial outbreak of covid. It was a close decision, with the Monetary Policy Committee voting 5-4 in favour of a cut.

Inflation

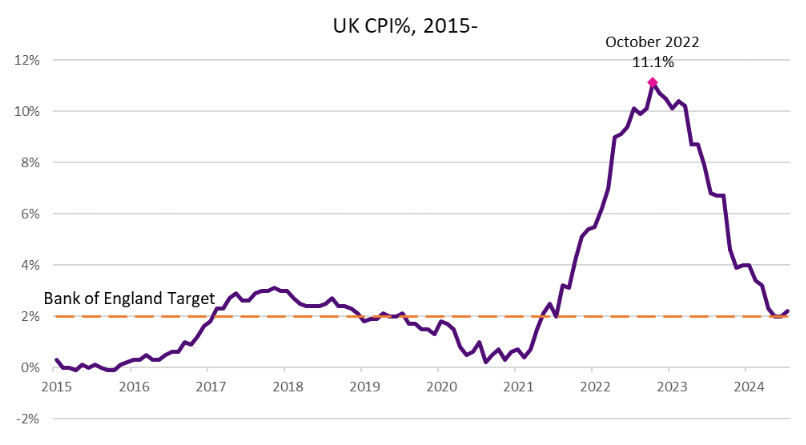

The decision preceded the release of inflation data for July. After two consecutive months of inflation in line with the BoEs target rate of 2.00%, the UK Consumer Price Index (CPI) measure of inflation showed a modest uptick in the pace of inflation to 2.20%. The data exhibited upward pressure from housing and household services, with downward relief from restaurants, hotels, and transport.

There are positive signs for the UK economy. Most recent figures from the noted forward-looking indicator, the S&P Purchasing Managers’ Index, suggested an increase in activity in both the manufacturing and service sectors.

In a boost for consumers, recent figures from the British Retail Consortium ‘shop price index’ have shown a fall in prices for the first time since 2021. It was reported prices fell by 0.30% in August, down from an increase of 0.20% in the prior month. Declines were led by retailers seeking to move on summer stock amid underwhelming weather. Food price inflation was also thought to have eased to 2.00%.

Politics

Looking forward, Prime Minister Keir Starmer took to the garden of 10 Downing Street to deliver a sobering speech ahead of the October budget. Starmer forebode of a “painful budget”, implying tax rises to cover higher levels of public indebtedness. The Chancellor, Rachel Reeves, is expected to focus on wealth, pensions, and property for additional sources of revenue.

The US Presidential Election closely follows the Autumn budget in the UK. Both former President, Donald Trump, and current Vice-President, Kamala Harris, are laser focused on key swing states. Harris, the newly anointed Democratic Party nominee, has started her campaign with energy and has received a subsequent boost in recent polling. The race remains tight, with Donald Trump seeking to adjust his campaign to a new opponent.