There are two narratives at play within investment markets. One is that inflation is falling and so, with price rises under control, economies and companies can thrive. The other is that central banks might have gone too far in attempting to control inflation through raising interest rates. That this might prompt a recession and be in contrast difficult and painful for economies and companies. As news flows change, each narrative is able to take precedent and this has driven volatile markets both up and down in recent months.

UK Inflation

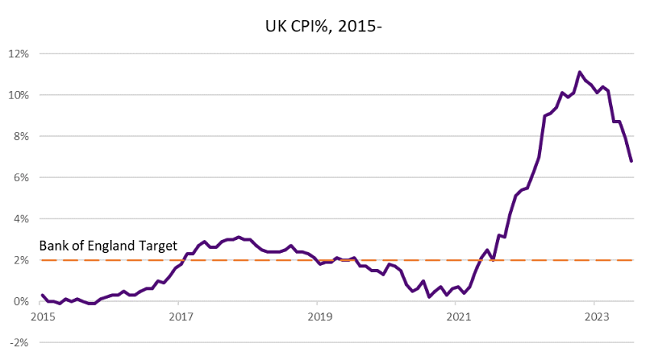

Inflation does appear to be falling. The UK Consumer Price Index (CPI) reading for July came in at 6.80%, a welcome decline on the June print of 7.90%. The decline was led by falling electricity and gas prices. In contrast the UK economy witnessed higher hotel and air fares as the UK consumer has continued to spend on leisure and experience-led pursuits. While food prices continued to rise, the pace of such declined.

Beyond the headlines, and more concerning for investors and central bankers, the core CPI reading for July, which excludes more volatile inputs such as food and energy, remained unchanged at 6.90%. This followed wage data, which pointed

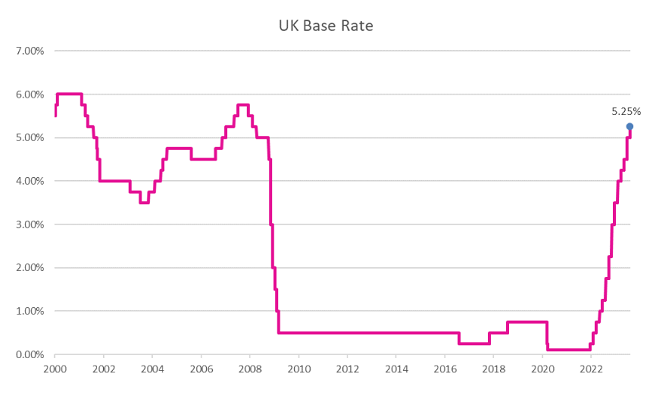

to growth in average total pay, including bonuses, of 8.20% in the three months to June. The stickiness in core inflation, and wage price growth, is a cause of concern as it suggests there is more embedded inflation within the economy which may require further intervention from central banks to resolve. In response, the Bank of England raised rates by a further 0.25% at the start of August to 5.25%, the 14th consecutive increase.

Inflation vs Economies

The Bank of England’s Monetary Policy Committee (MPC), as well as other central banks globally, are seeking to achieve a fine balance. Reducing inflation without inflicting too much unnecessary economic pain. There is a lagged effect to interest rate movements, which can make it difficult to assess both the impact of previous rises, and the potential need to increase them further.

Both central banks and investors are therefore reacting to data to consider what direction future policy might take. Investment markets have therefore found it difficult to forecast at what point interest rates should ‘peak’. This has been most evident in the bond markets, with considerable volatility in yields, and by extension bond valuations, as investors attempt to call the top in the cycle.

There are mixed signals about the strength of the UK economy. The Nationwide Building Society reported average house price declines of 3.80% in the year to July. But price declines are not uniform, with areas such as the North of England, where affordability is less stretched, showing more resilience. UK industry surveys have pointed to a slowdown in activity. But once again this varies by sector and business. While the economic climate is uncertain, it is important to stress the news flow has not been uniformly bad. Crucially, the UK has thus avoided a recession.

Going forward, some of the notable pressures on household budgets, such as food and energy price increases, are abating. This might provide a boost to consumption, and an easing of the cost of living crisis. However, the impact of interest rate rises may not yet have been fully felt. For example, many mortgages holders remain on historic longer-term fixed rate deals.

Inflation and higher interest rates are also going to mean winners and losers in the corporate world. Troubled retailer Wilko was placed into administration, while Mark & Spencer has continued its revival by exceeding profit expectations. Highly indebted companies are likely to come under pressure as the rising cost of financing such debts increases.

China

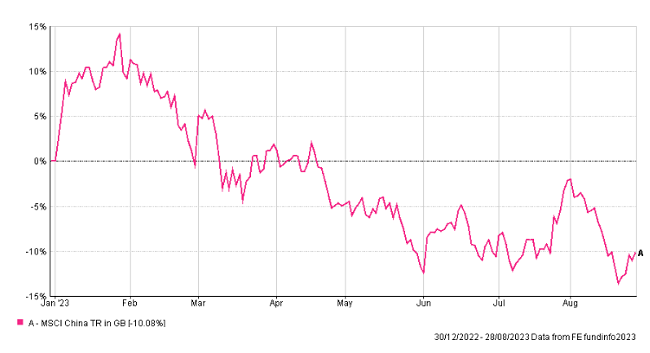

The Chinese economy has continued to disappoint investors. Chinese investment markets were initially met with optimism following the move to reopen the economy following the cessation of the country’s zero-covid policy. This momentum appears to have stalled though and second quarter economic growth slowed to an annualised rate of 3.20%. Far short of the heady days of double-digit expansion. This disappointing economic performance has resulted in volatile price movements of Chinese companies.

There is a general lack in confidence in the Chinese economy. Difficulties in the economically influential real estate sector have prompted concerns about deflation, with building materials and household appliances seeing price declines. While deflation in the price of Chinese exports may help sooth near-term inflation in the west, such indicators are rarely positive in the long-term. While the Chinese authorities have trimmed short-term benchmark interest rates, investors are hoping for a more comprehensive growth and stimulus package. Stimulating the economy, while avoiding reigniting speculation in the property sector will be no easy task.