To consider an analogy, the UK economy is a mountain walker standing in Fort William looking up to the summit of Ben Nevis, nervous of the climb ahead and unsure of the best path to take. Like many mountain walkers this is not their first mountain and they have made it to the top of other climbs before. But Ben Nevis is a big mountain.

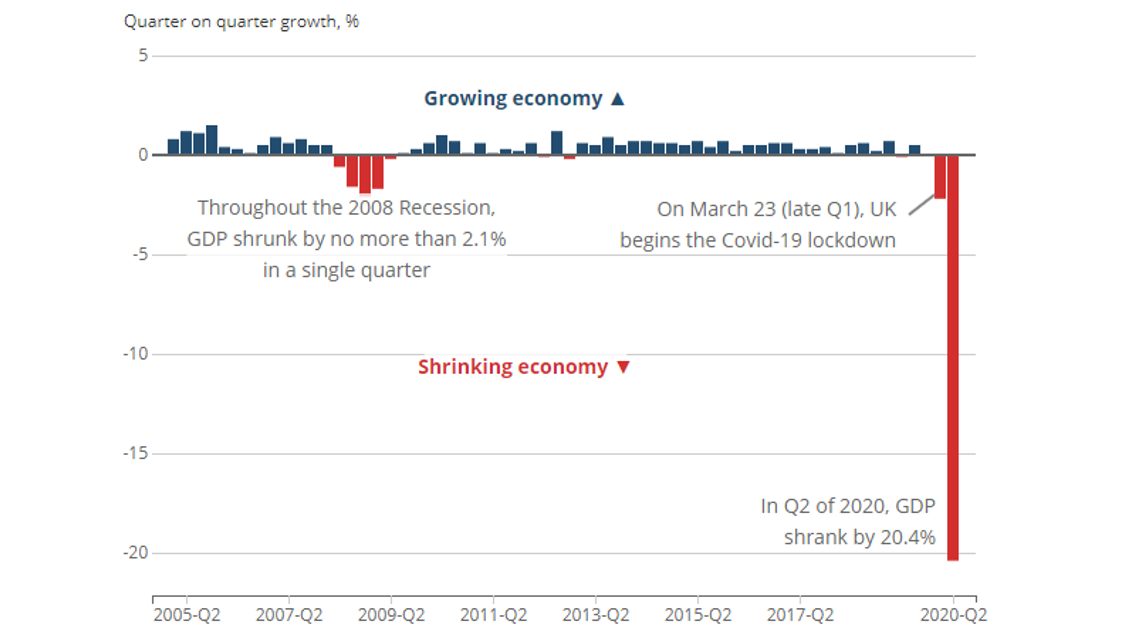

We find ourselves at basecamp as it was announced with little fanfare that the UK economy was confirmed to be in recession following two consecutive quarters of negative growth. The slump between April and June represented the biggest on record as the economy shrank 20.4% when compared with the first three months of the year. This was always going to be inevitable following the coronavirus lockdown measures which saw economic activity grind to a halt as the vast majority of businesses were ordered to close.

While the word ‘recession’ paints a very gloomy picture, the economy is now in recession only on this technical measure. This is not a structural recession like in the 2008 Global Financial Crisis, caused by overexuberance and structural problems in credit markets, but a deliberate act of economic self-harm to protect and save lives. As the number of cases has been reduced, so too has the number of restrictions on business activity and daily life and this has seen the economy begin its long ascent to the peak.

While the quarterly slump of 20.4% represents a record decline, on a month by month basis the economy actually grew by 8.7% in June following growth of 1.8% in May. Daily life, with masks and social distancing, hardly reflects normality but other measures certainly reflect the pickup in activity. Restaurants, hit particularly hard by the effect of lockdown, have seen an increase in bookings particularly on the days of the governments ‘eat out to help out’ scheme which appears to have been a success in driving footfall back to high streets.

https://www.opentable.com/state-of-industry (information from the UK dataset).

This increased activity can also be seen on road traffic data where daytime traffic has increased back towards historic trend levels. One area that has not returned to its historic level however is rush hour which remains well below historic averages reflecting a still significant proportion of the workforce still furloughed or working from home.

This is early progress, but it clearly demonstrates the gears that drive the economy beginning to turn again as shops and businesses begin trading, even if at reduced capacity. It is a path filled with dangers but perhaps governments and central banks can be assured to provide mountain rescue services if the initial progress loses its footing. It is unknown yet how the economy will react as Government support packages such as the furlough scheme are wound down.

If the economy is a hiker only on the foothills in its hike towards recovery, stock markets are mountain runners who have powered on up the mountain. Central Banks and Governments quickly stepped in to anchor the rope on the abseiling economy and this support has allowed share prices to quickly rebound. The US stock market has been the standout performer with both the S&P 500 and the tech-focused Nasdaq both reaching record highs in recent weeks, beyond what they achieved in the pre-Covid world.

This recovery has been driven by major companies such as Amazon and Microsoft seeing their share price increase to their own record highs. Apple became the first US company to be valued at $2 trillion, only 2 years after reaching the $1 trillion milestone. While the rally of these US indices has been swift, not all have matched the ascent.

Other stock markets have been unable to match the pace of the US and have paused for breath, unable to find a secure foothold, in their climb back towards the summit of pre-Covid valuations. While initial progress was positive, since June indexes have been stuck in what has been termed the ‘summer box’ with prices fluctuating in a small range with no real momentum up or down. The result is that the FTSE 100 is trading 20% down from the start of the year. A valuation perhaps more reflective of the true state of the underlying economy than our mountain running counterparts across the pond.

The other major story has been the gold price reaching its own record high in August ($2,070/oz, from $1,519/oz at the start of the year) due to a weak dollar, and rising demand both from investors seeking a ‘safe haven’ for their money and others not wanting to miss out on the rising price. The US dollar has been weak in recent weeks due to continued monetary support from the Federal Reserve, flooding the market with an overabundance of dollars.

Investors are nervous of what the future holds for investment markets. No one knows how the economy has truly been affected by the pandemic and the ongoing impact it has had. The ongoing management of Covid-19 is a fine line being tread by governments across the world, as they try to balance the health of their economies and the health of their people. If another lockdown is required, it could be a slippery slope back down the mountain. Even if the path remains secure it is a walk into strong headwinds with volatility caused by the US election, Sino-American relations, and the return of Brexit which will likely dominate headlines at the end of the year when the transition period is currently scheduled to come to an end.

Invitation

If you would like to discuss anything in this update, please contact your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England. Note that the information in this market update represents the views of the Investment Managers at Vesta Wealth Limited at the time of writing, which may change.

Reach us via:

t: 01228 210 137

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England. Note that the value of investments and the income from them call fall as well as rise.