Any commentary on investment markets is a snapshot in time of the understanding of events when it was written. The irony is not lost then that the day after publishing our market update in November, a new heavily mutated variant of covid had been discovered in South Africa which sent markets spiralling rendering our comments immediately out of date.

Ο, Omicron

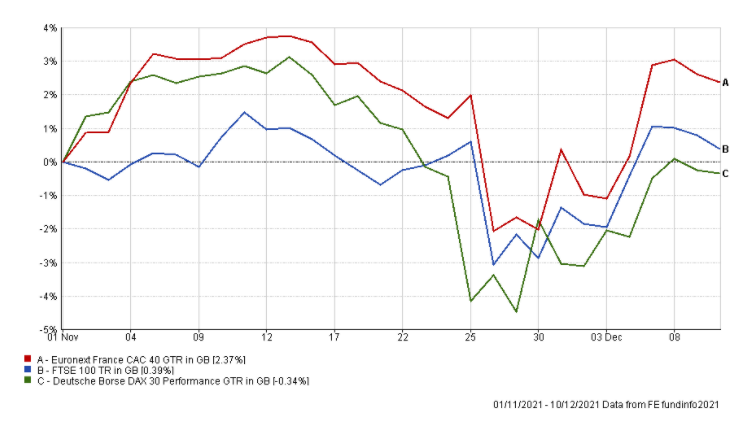

Covid was an issue that had largely been cast to the side-lines by markets over the summer months with more pressing matters of inflation and the economic recovery being considered. The new variant however thrust it back to the fore. Europe was already dealing with another wave of the Delta variant in November and restrictions in varying severity had been introduced across the continent in a bid to contain that spread. European markets were already experiencing a minor decline as a result of these restrictions, before the discovery of Omicron caused a sharp fall across all major developed markets, with Europe and the UK being particularly affected following headlines that the variant had already resulted in cases there.

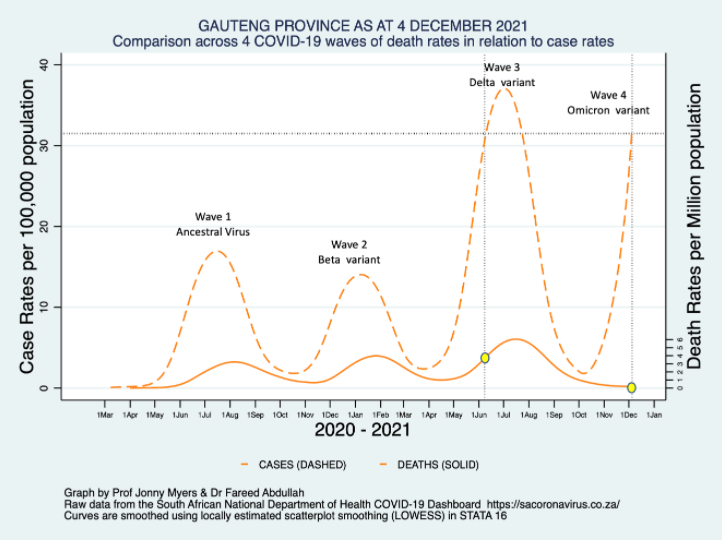

The biggest fear markets have over the heavily mutated new variant is that lockdown restrictions may be required should it prove vaccine-resistant and begin to place pressure on health services. This is the worst-case scenario and fears of which sparked the sharp falls. The very early signs out of South Africa, and the Gauteng province where the variant was discovered, however suggest that Omicron will be highly transmissible, resulting in many cases; but the effects are relatively mild, meaning that they might not translate into troubling levels of hospitalisations and deaths. This more optimistic news has meant that many stock markets have recovered much of their lost ground however the situation remains highly uncertain.

It must be caveated that this data comes from a very small sample size of early cases and the situation is evolving daily as knowledge of the new variant grows and certainly as cases rise quickly in the UK. The cause for optimism will only likely be found in the new year when we get a clearer understanding of the true impact of the variant as it spreads around the world. Omicron is forecast to become the globally dominant variant and should health services be put under strain as a result it will create volatility in markets as investors consider what policy response may be made to contain it. We have already witnessed this here in the UK with the announcement of ‘plan B’ restrictions in England and the heavy promotion of booster vaccines to combat the worst effects of the virus.

Inflation

In addition to covid concerns, markets have also been reassessing inflation and central bank policy following comments made by the US chairman of the Federal Reserve, Jerome Powell. Inflation has been a concern for much of the year with the debate raging between elevated readings being merely transitory or a more permanent issue. Central banks have been leaning on the transitory side of the argument given the obvious supply and demand issues and imbalances as economies have reopened from varying lockdown measures.

The theory was that as supply chain issues are resolved and demand normalises, prices will potentially return to normal, and with it, inflation would fall to a more manageable level. If there was a possibility that inflation would go away on its own, then central banks were hesitant to remove or reduce the currently supportive policy as this might jeopardise the potentially fragile economic recovery. If there was a risk it might derail any progress, it was one they wanted to avoid.

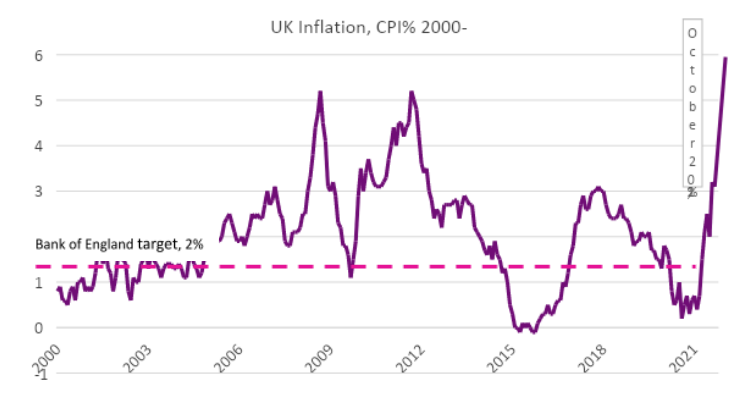

However, US inflation currently measures at a 3-decade high and UK inflation at a 10 year high; in the face of this, Jerome Powell at the end of November made one of the first admissions that inflation may not be transitory and stated that the Fed will discuss speeding up bond-buying tapering in a bid to limit inflation. This admittance marked a very real turning point given the previous dismissal of inflationary forces by major central banks for much of the year.

These comments created volatility within bond markets as yields gyrated between policy indecision and what it might mean for the economic recovery. Adding the new Omicron variant into the mix only increased the level of uncertainty. While the attention of the world is focused on watching how the situation develops with the new variant, many eyes will also be trained on upcoming meetings of major central banks for indications of what action will be taken as it could be a major driving force for markets in 2022.

Santa Rally?

On a lighter note, to end our final update of 2021, a rise of investment markets in December is termed a Santa rally, a holiday gift delivered to investors to end the year. Since 2000, the FTSE 100 has risen in 17 of the last 21 Decembers and this has led market observers to believe there is some clear pattern for this outcome. Some touted explanations for these price moves have ranged from people being in an optimistic festive spirit, to tax reasons, with many other theories in between.

The question therefore can be asked of whether 2021 may deliver another positive December? However, while trends like these can be interesting patterns to observe they are merely that, observations, and there are never any guarantees when it comes to investing.

Whether markets rise in December is unimportant as long-term investors. But it is important to not lose sight of your investment objectives and to remain invested. Despite uncertainty, 2021 has so far delivered strong returns for investors who have been gladly rewarded for staying invested through the lows of the market in 2020 and the recovery through into 2021. Whatever challenges 2022 brings, this mantra will always remain true.

Invitation

If you would like to discuss your financial plan and investment strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.