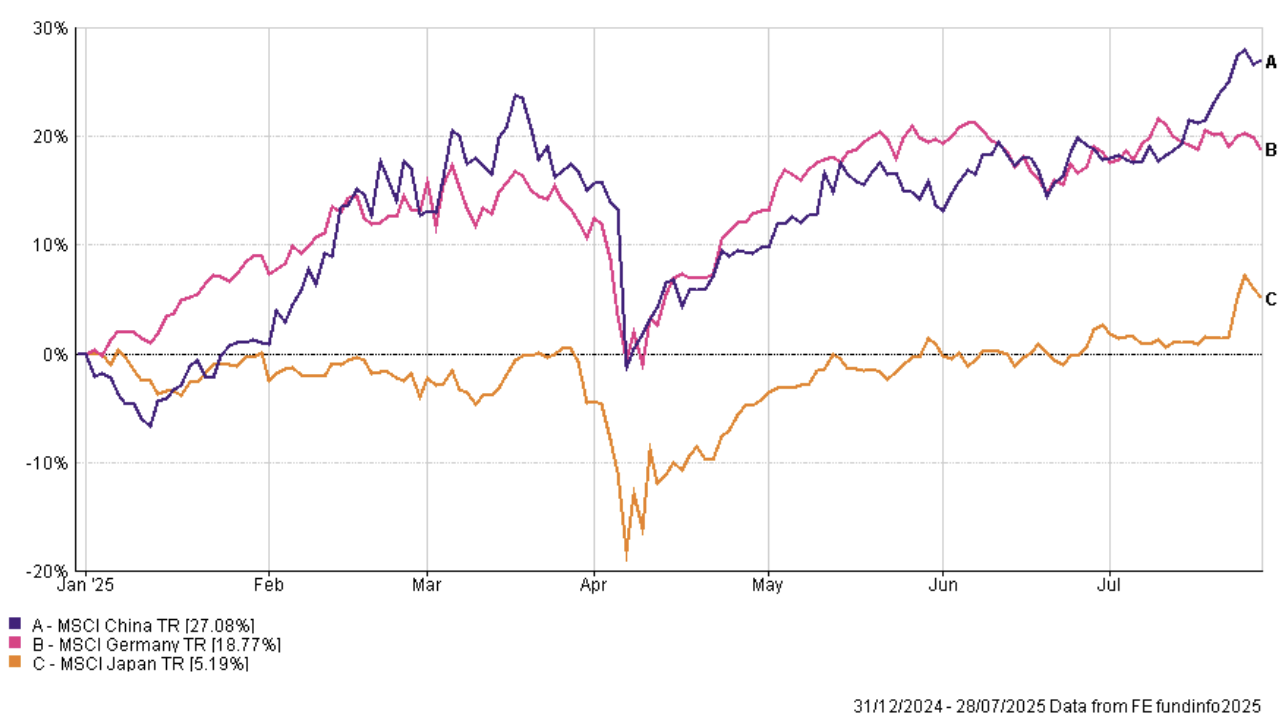

July was another positive month for equity markets with a string of notable headlines and milestones reached. Stock markets around the world reached new record highs, completing for many their recovery from the turmoil following ‘Liberation Day’ and the initial announcement of trade tariffs by US President Donald Trump. The FTSE 100, often seen as an international laggard, set a record high breaking the significant 9,000 level for the first time. Other examples include stock markets in Australia, Japan, Germany, and both the S&P500 and the Nasdaq composite indexes in the USA.

TACO

Despite the uncertainty surrounding tariffs, investors have taken comfort in various delays and trade deals. Markets have also taken a more optimistic view of Donald Trump’s propensity to engage in deadline-based brinkmanship when negotiating trade deals. This led to the acronym ‘TACO trade’, standing for Trump Always Chickens Out, referencing the numerous extensions and delays to tariffs that have been announced.

This was seen in effect as the initial 90 day ‘pause’ on tariffs was extended in July until the start of August. After this date, for countries failing to strike a ‘deal’, a range of penal tariffs were proposed. As the deadline has neared, a series of deals were announced with varying base level tariffs. Early indications would suggest that tariffs will sit in the 10% to 20% range. Japanese equities rallied, after Donald Trump announced a “Massive” trade deal between the two counties. Given the flurry of deals, it is challenging to assess the full extent of each arrangement. For example, the arrangement with China is a framework understanding, rather than a trade deal, with many issues of contention unresolved.

The uncertainty around tariffs, alongside the anticipated impact of Trump’s “Big Beautiful Bill”, has muddied the outlook for inflation. Donald Trump has repeatedly expressed his frustration at the lack of interest rate cuts from the Federal Reserve, aiming a series of derogatory remarks at Chair, Jerome Powell. This has prompted speculation that Trump may seek to replace Powell before his term ends next year. Such a move, likely to be viewed unfavourably by the bond market, has been denied by Trump.

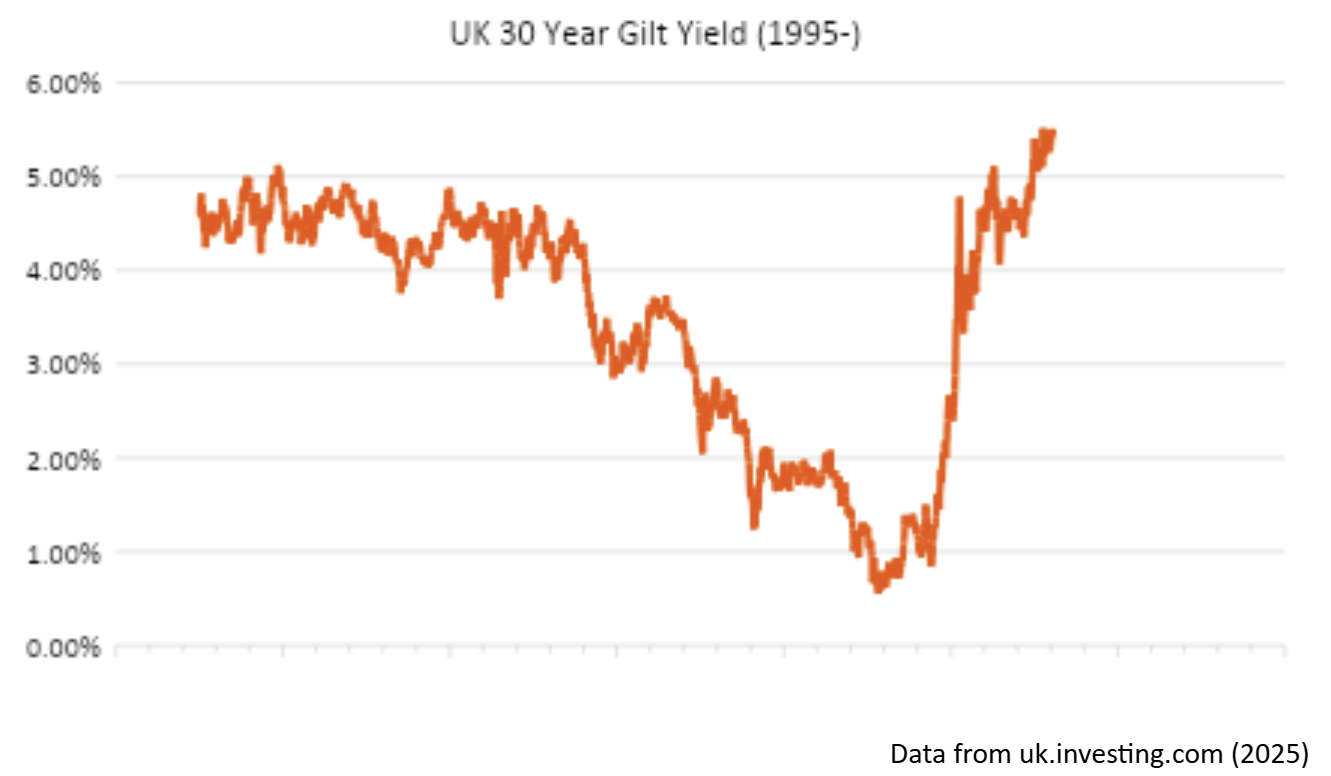

Whilst interest rate cuts are anticipated to varying degrees in respective economies, the costs of longer dated government debt have increased globally. Rising yields are an expression of investor concern over the sustainability of government finances. This has been notable in the UK where the 30-year gilt yield has flirted with the 5.50% level; a level last seen in the 1990s. The problem of rising bond yields was highlighted in recent data covering government borrowing and deficits. Of the £20.70bn deficit in June, £16.40bn was represented by the cost of interest payments on existing debt.

Negotiating Growth

For the UK economy, Chancellor Rachel Reeves faces a number of challenges as she looks ahead to her autumn budget. After booking solid growth of 0.70% in the first quarter of this year, estimates suggest the UK economy contracted in April and May. The Chancellor announced a plethora of initiatives in her Mansion House speech to encourage greater risk taking within the economy. These focused on deregulation to boost lending and investment. The speech evoked mixed responses, with Bank of England Governor Andrew Bailey cautioning on rolling back ring-fencing rules at banks. These rules were put in place after the global financial crisis to protect retail customers from the riskier commercial lending and investment banking activities of an institution.

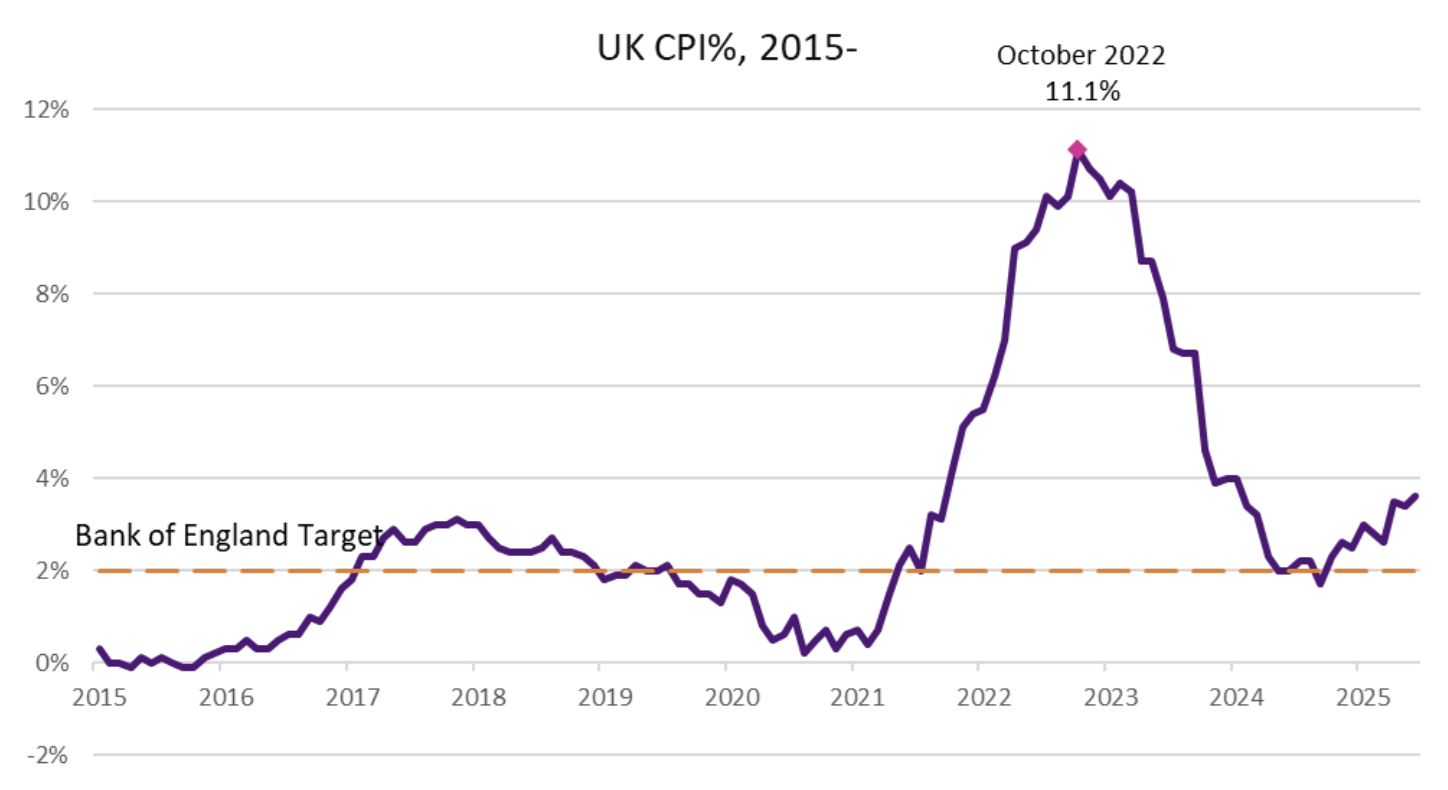

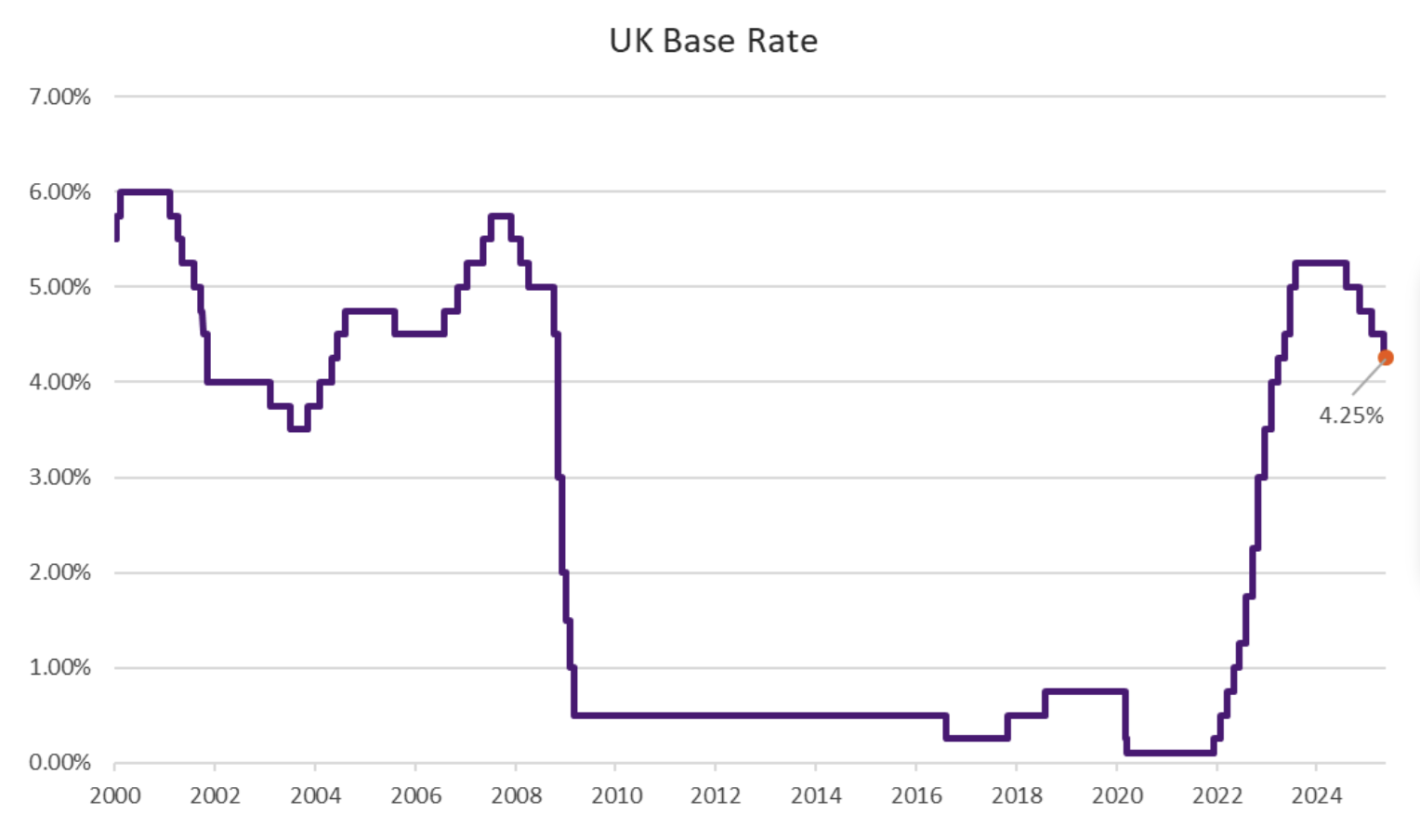

Inflation also remains stubbornly above the target level of 2%. The Consumer Prices Index (CPI) measure of inflation for June was 3.60%, up from the 3.40% in May. The Bank of England will meet to set interest rates in early August. The challenge for the central bank is balancing support for the economy with the inflationary impact that might result from lowering interest rates.

In Europe, the European Central Bank elected not to make a further interest rate cut at its July meeting. This follows eight cuts in the last year. The ECB noted that there would need to be a significant deterioration in growth for a cut to be instituted at the September meeting. The announced trade deal between the US and the EU saw baseline tariffs applied at 15% for good imported to the US from the EU. In comparison, the UK trade agreement with the US set baseline tariffs at 10%.