Geopolitics dominated the narrative for investment markets in June. The escalating air-based conflict involving Iran, Israel, and the US was the biggest event adding to uncertainty, with the biggest impact being felt in commodity markets. At the time of writing, a tentative ceasefire had been announced, and markets took solace in the reduced level of uncertainty.

MOP

The impact the conflict had on markets was a mixture of reaction to what had happened, and uncertainty around what might happen. Israel’s attack on Iranian military sites was predicated on the need to eliminate the alleged threat of the imminent development of weapons grade nuclear material. Iran responded with missile attacks on Israel, seeing the pre-emptive attack as a violation of its sovereignty.

US President Donald Trump citied frustration over the pace of negotiations in resolving the conflict before authorising US attacks on three Iranian nuclear facilities. After pledging a response to the US attack, Iran launched a telegraphed and measured attack on a US airbase in Qatar. The importance of the attack being telegraphed meant there were no casualties, and it was a token retaliation paving the way for the cessation of hostilities. Shortly afterwards, Donald Trump announced a ceasefire between Iran and Israel albeit tensions remain high.

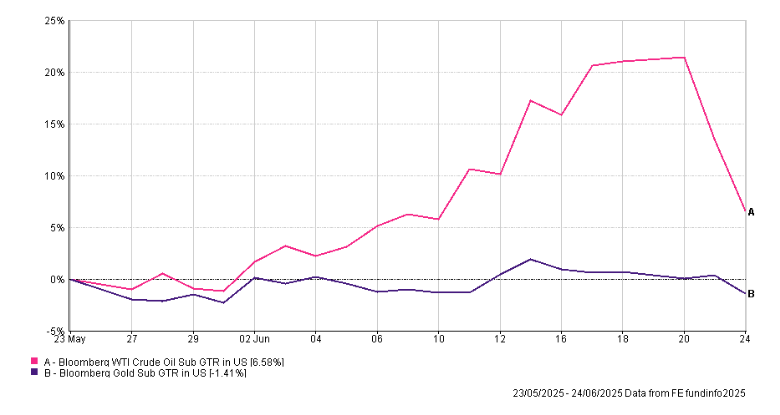

During the short, but significant conflict, markets saw an increase in volatility although less than might have been expected. Oil prices exhibited the highest level of volatility during the skirmishes amid fears that Iran could disrupt the passage of oil tankers passing through the Strait of Hormuz. This strategically important shipping lane links the Persian Gulf with the Arabian Sea; and accounts for around 20% of the global oil supply. Following the ceasefire, oil prices fell sharply as these fears abated. Gold prices experienced a similar movement with the precious metal benefitting from increased demand on the initial outbreak of the conflict, before also falling on the announcement of the ceasefire.

Despite the uncertainty of the conflict, equity markets were remarkably resilient. Trading was at times volatile however US markets made positive gains throughout June as they continued to recover from the fallout of Trump’s tariff announcement. Investors were able to shrug off concerns surrounding the conflict, and, taking comfort in various delays, negotiations, and legal challenges, appear less concerned about the impact of trade tariffs. As a result, the US S&P 500 index has recovered close to its record high set in February 2025.

Inflation, Interest Rates, and Banks

Away from geopolitics, it was a busy month for Central Banks. At the beginning of the month, the European Central Bank instituted its eighth interest rate cut in a little over a year; taking the deposit rate to 2.00%. President, Christine Lagarde, described rates as being in a “good position” despite the tariff-related uncertainty of Donald Trump’s trade policy.

In the US, the Federal Reserve kept rates on hold but continued to signal two cuts later this year. It was noted that while uncertainty remains significant, it has of late receded. With a number of trade negotiations ongoing, and the threat of tariffs real, the task for the Federal Reserve is difficult with projections indicating higher levels of inflation but lower levels of growth.

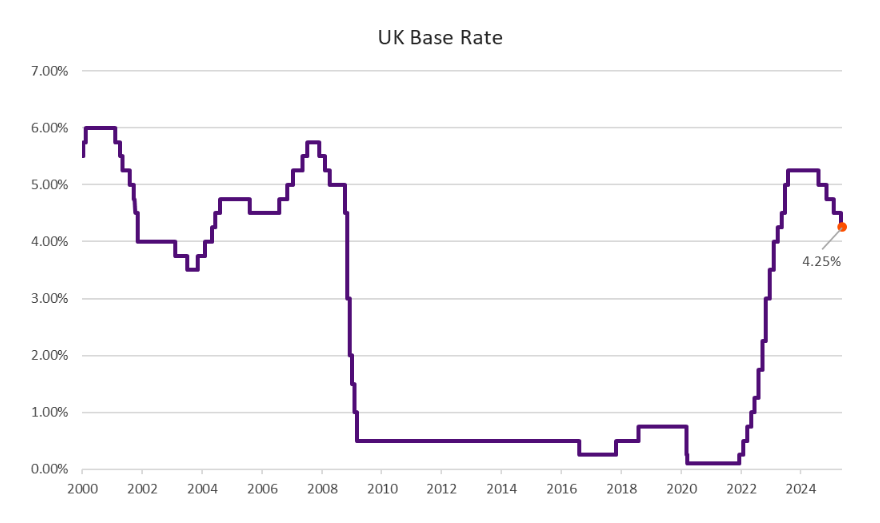

The Monetary Policy Committee of the Bank of England also held rates at 4.25% at its June meeting. With four cuts of 0.25% already instituted in this cycle, Bank Governor, Andrew Bailey, asserted that rates remain “on a gradual downward path,” whilst also noting high levels of unpredictability in the world.

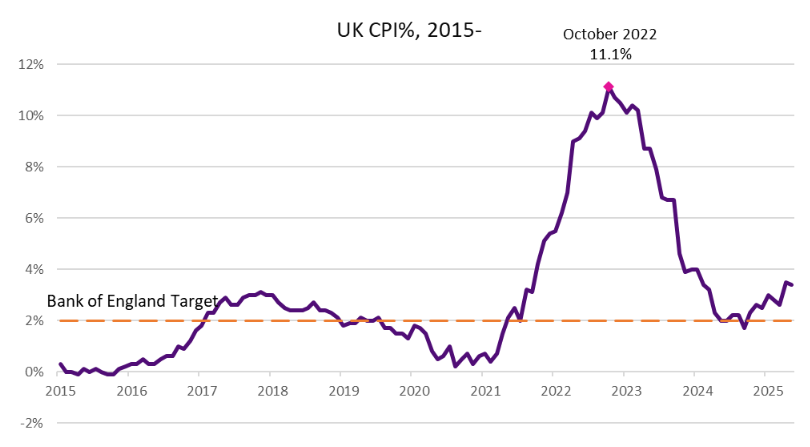

The decision closely followed the release of UK inflation data for May. The Consumer Price Index measure of inflation slowed to 3.40% from 3.50% measured in April. Whilst there were downward contributions from transportation costs, these were largely offset by upward contributions from food, furniture, and household goods.

June also saw UK Chancellor, Rachel Reeves, deliver her spending review setting out government budgets and planned spending in coming years. Reeves outlined plans for a national renewal, with large scale investments into nuclear power, social housing, and travel infrastructure. Sustainable growth remains a challenge for the Chancellor with the ONS estimating that the economy shrank by 0.30% in April, following growth of 0.20% in March. Higher levels of government borrowing have led to predictions of further tax rises in the autumn budget.

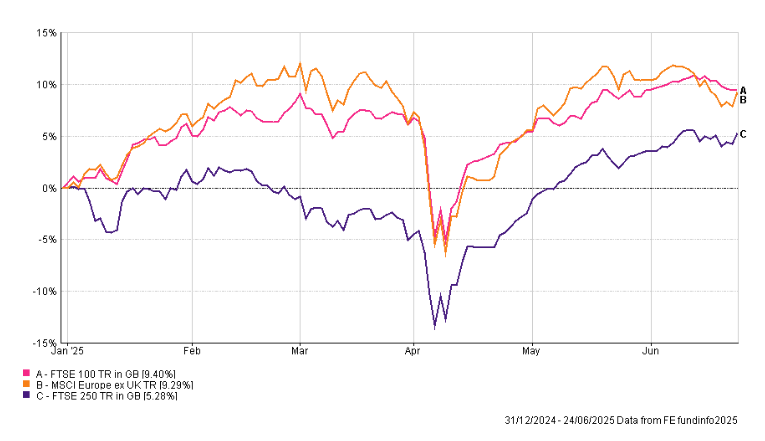

Stock markets in the UK and Europe had a mixed month. The escalating tensions in the Middle East and fading trade optimism put downward pressure on markets across the continent. The announced ceasefire had a positive impact however with markets rising to end the month, continuing a positive run of performance year to date.