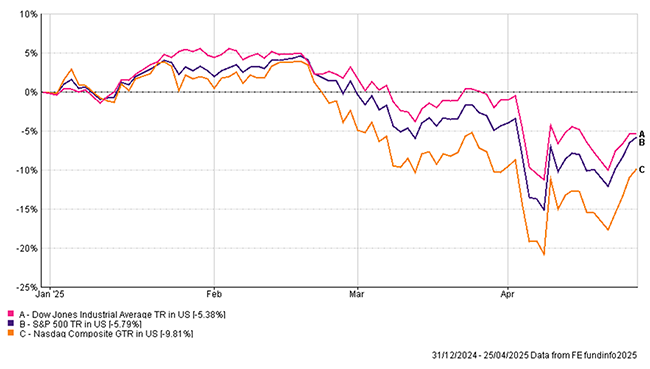

Investment markets made headlines in April as markets fell in response to Trump’s trade tariffs and the potential impact on global economies. US stock markets suffered the largest losses. The Dow Jones, S&P 500, and Nasdaq Composite indexes all fell over 10% in the days following the announcement.

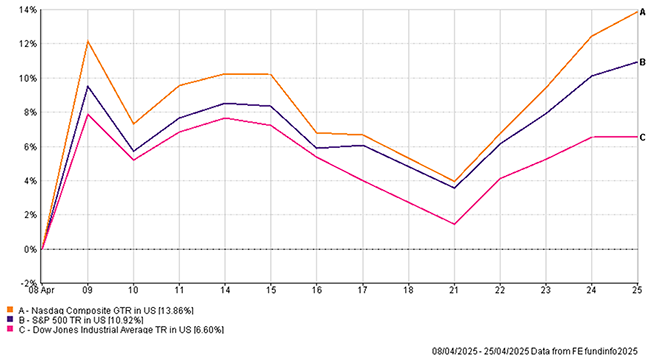

Markets have since attempted to recover; however, uncertainty remains high. Despite the significance of the headlines and the severity of the falls, when viewed in context of long-term returns for markets the impact is less pronounced. At the lowest point for the S&P 500 in early April, this was a return to the levels markets traded at in April 2024.

Why Tariff

The tone for the month was set early on by Donald Trump’s much vaunted “Liberation Day”. In theatrical style, Trump unveiled a raft of tariffs on global trade partners which shocked financial markets in both their level and scope. In simple terms a tariff is a tax on imports. This makes imports more expensive, increasing the competitiveness of domestically produced goods.

While the tariffs were termed “reciprocal”, they were not set at a level matching the tariffs which US exports face to a particular country. They instead were said to reflect a holistic range of ‘trade barriers’, including value added tax and perceived currency manipulation. The methodology underpinning the calculation of the “reciprocal” tariffs essentially considers the level of trade deficit or surplus a particular country has with the US. Countries who export more to the US than they comparatively import were due to face higher tariffs.

Excluding Canada and Mexico, there was a minimum base level tariff of 10%, which included the UK. Under Trump’s own ‘formula’, the UK tariff should be negative i.e. the UK imports more from the US than it exports. China, where trade relations are most obviously strained, initially faced tariffs at 34%. However, this was the most obvious example of a ‘trade war’ as a tit-for-tat of increasing tariffs eventually saw this figure raised to 145%.

Market Pressure

With pressure on US equities, government bonds, and the dollar, all risking economic instability, alongside a chorus of concerns from the US corporate sector, a variety of concessions have since been announced by The White House. These took the form of various delays and exemptions. It is reminiscent of the market reaction to Liz Truss’s mini budget where financial instability essentially forced a backtrack on policy.

Stock markets globally rallied strongly after it was announced that, excluding China, the abrupt tariff hikes would be subject to a 90-day delay to allow time for trade negotiations. The pause saw the single best day of performance for the S&P 500 since 2020 with the index rising 9.52%. Despite this, a high degree of uncertainty remains and investors remain cautious.

Investment markets reacted negatively to comments made by Trump criticising the US central Bank, the Federal Reserve, for not cutting interest rates. The Federal Reserve face an unenviable task of balancing the inflationary risks of moveable tariff levels, alongside the negative shock to demand in the economy. There has also been confusion over the extent of negotiations with China. The Chinese authorities have claimed that there has been no contact over trade, with Donald Trump suggesting the opposite. With such fluid rhetoric, financial markets have struggled to find a base throughout April.

Resilience

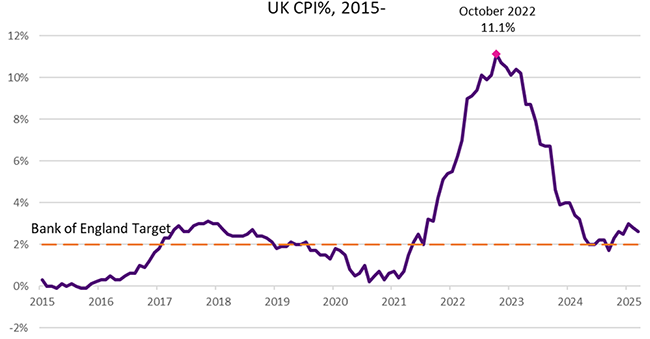

In contrast, although not immune from financial market turbulence, the UK has been an area of stability. Dollar weakness has provided a lift to sterling. The UK economy received a boost with GDP growth figures exceeding expectations at 0.50%. In addition, inflation, as measured by the consumer prices index, fell to 2.60% in March down from the prior month’s reading of 2.80%. This has led to strong expectations of a cut to interest rates at the upcoming meeting of the Bank of England in early May. For UK stock markets, the more domestically focused FTSE250 has suffered amidst global uncertainty. However, the FTSE 100 continues to be a relatively strong performer attracting attention from investors seeking alternatives to US investments.