After enjoying a positive year in 2024, investment markets have started 2025 on a more uncertain footing. Global investment markets have experienced a mix of volatility and resilience amid a backdrop of evolving economic indicators and tightening monetary policies. Both equities and bonds have seen notable movements, driven by a combination of central bank actions, inflation concerns, and geopolitical developments.

Falling interest rates

A key focus for investors remains central bank policy in respect to interest rates. Central banks continue to face the difficult challenge of managing inflationary pressures while being mindful of the economic impact of any policy changes.

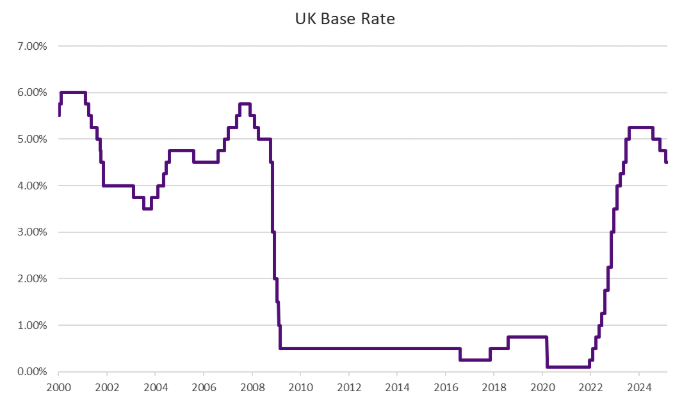

In the UK, the Monetary Policy Committee (MPC) of the Bank of England (BOE) voted 7-2 in favour of reducing the base rate by 0.25% to 4.50% in early February. Interestingly the two dissenters voted for a larger cut of 0.50% in contrast to dissenters at previous meetings who had voted to hold interest rates. The dissenters referenced weaker UK economic data in casting their votes with the BoE downgrading growth forecasts for the UK in 2025 from 1.50%, to 0.75%.

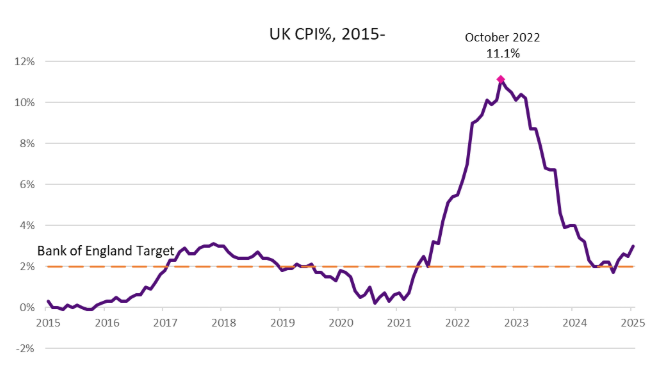

The difficulty for the central bank is while it is forecasting slowing growth, at the same time inflation is forecast to rise in the near-term. The Consumer Price Index (CPI) measure of inflation for January 2025 saw inflation jump from 2.50% to 3.00%. While inflation is showing signs of increasing, the Office for National Statistics estimated that annual growth in employees’ average regular earnings, excluding bonuses, was 5.90% in the period October to December 2024. A comfortable premium over the rate of inflation.

The UK government recorded a revenue surplus of £15.40bn in January. January is usually a surplus month owing to tax payments. However, while the surplus of £15.40bn was the highest since records began, it fell short of forecasts of £20.50bn. Attention will now shift towards to 26th March when the Office for Budget Responsibility releases its updated forecasts for the UK economy and public spending. The Chancellor will deliver a Spring Statement on the same day.

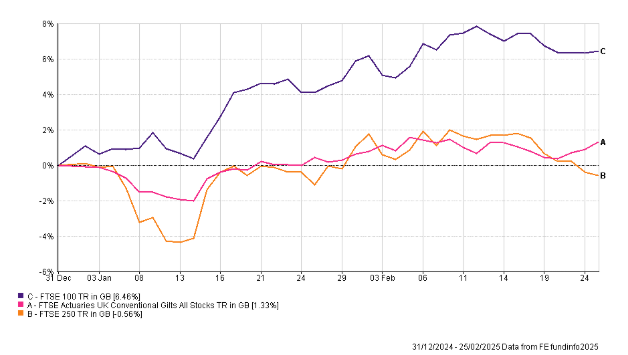

UK equities, long out of favour with global investors, have enjoyed a positive start to 2025. The FTSE 100 set a record high in February moving close to the milestone 9,000 level. The more domestically focused FTSE 250 continues to face greater headwinds and has struggled in recent weeks. After making headlines in January, gilt yields have been volatile in response to inflation and growth concerns.

The Trump Effect

In the US, Federal Reserve Chair, Jerome Powell, reiterated that a strong jobs market and still elevated inflation means there is no hurry to institute further cuts to interest rates. It is a challenging period for monetary policy in the US, as Donald Trump has a very fluid tariff-led economic policy. Policies that will have a direct inflationary impact by increasing purchase prices. An example being the announcement of a 25% tariff on all imported steel and aluminium.

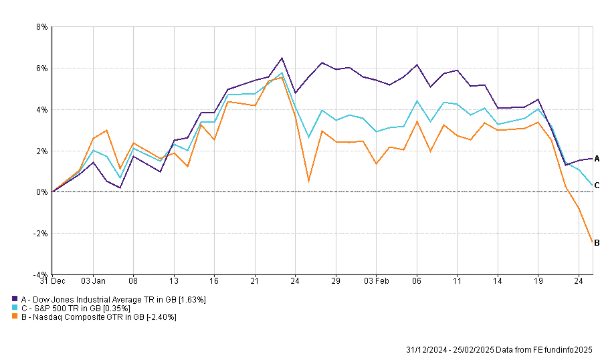

In contrast to the large cap UK equities, US equities have faced a more volatile start to the year. Long the poster child of investment markets, the S&P 500 and Nasdaq Composite indexes have experienced notable daily falls following underwhelming reporting from the ‘magnificent seven’ stocks (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla). The Dow Jones Industrial Average tumbled more than 700 points on 21st February after weaker service sector and consumer survey data. For US Investors, this was an opportunity for some profit taking, with the major indices still trading near record highs.

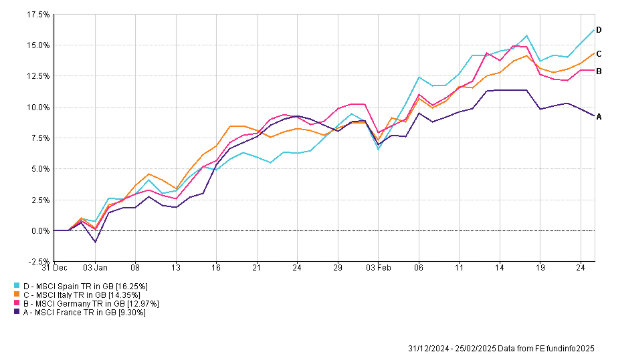

In Europe, Eurozone inflation for January came in at 2.50%, slightly ahead of forecast. The European Central Bank (ECB) lowered rates by a further 0.25% in January to 2.75%, the fifth cut this cycle. It has generally been a positive start to the year for European equities, with investors enthused by lower rates and the possibility of an end to the war in Ukraine following talks held in Saudi Arabia between representatives of the governments of the US and Russian Federation. Elections in Germany delivered a largely expected result with the Christian Democratic Union (CDU) and its Bavarian sister party, the Christian Social Union (CSU), winning the largest share of votes.

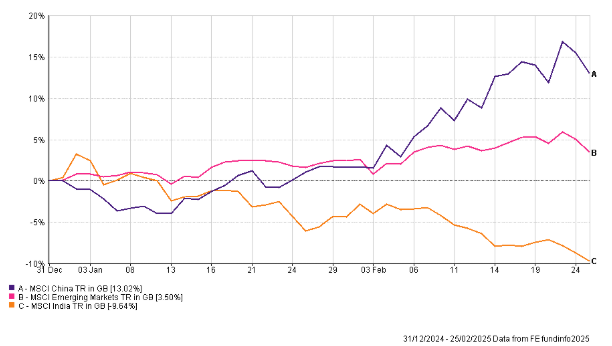

In composite terms, it was a positive month for Emerging Markets. However, there was a notable divergence between the performance of Chinese and Indian equities. The emergence of DeepSeek, the lower cost artificial intelligence app, and the expectation of further stimulus, has boosted performance of Chinese equities. Indian equities have continued to face pressures from a weakening currency alongside declining investor interest following tightening monetary policy and economic uncertainty.