Polls in the lead up to the US Presidential Election had anticipated a tight race. The result proved to be decisive. Former President, and now President-Elect, Donald Trump secured a comfortable victory in addition to unexpectedly winning the overall popular vote.

Significantly, the Republican Party also secured narrow majorities in the House of Representatives and the Senate giving them control of Congress. This places President-Elect Trump in an advantageous position to enact policy changes with more assurance of gaining congressional approval. However, not all Republican Party members are closely aligned to his “Make American Great Again” theme of politics.

Positive Markets

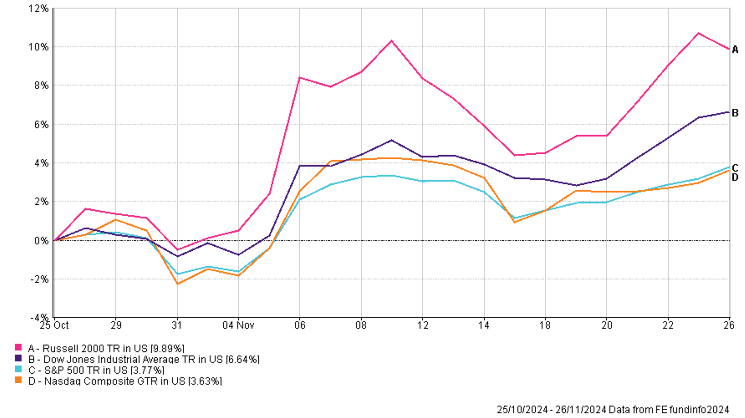

The equity market has responded positively to the outcome of the election. US stock markets soared as investors took an optimistic view on Trump’s expected business-friendly policies. Both the S&P 500 and Nasdaq composite Indexes rose to record highs in the immediate aftermath of the election. The S&P 500 crossed the significant 6,000 milestone, only seven months after reaching the then-significant 5,000 level.

As the month progressed, there was a notable change in leadership in the US equity market as investors adjusted for the anticipated economic polies of the administration of Donald Trump. This has seen more economic sensitive indexes such as the Dow Jones Industrial Average and the Russell 2000, an index made up of predominantly smaller companies, perform robustly. Technology giant, Nvidia, released highly anticipated third quarter earnings that, in a relief for markets, beat expectations. Forecasts for the current quarter were also raised, as demand for high end chips to support the boom in artificial intelligence continues unabated.

Bond Yields

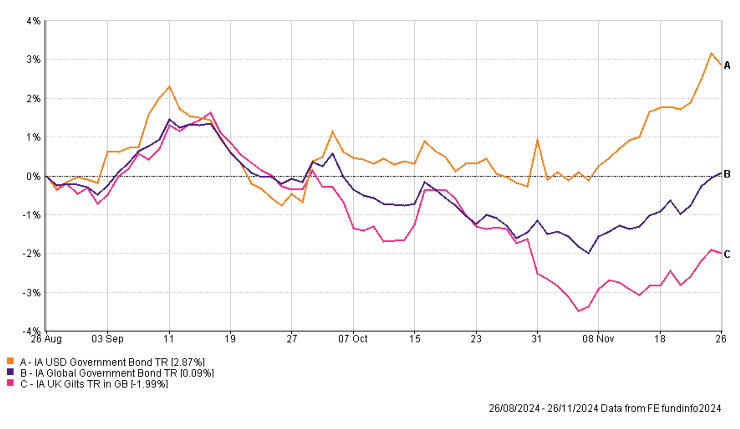

The bond market has been more cautious. Yields had steadily increased in the lead-up to the election, a sign market commentators pointed to as the market ‘pricing in’ the possibility of a Trump victory. In the immediate aftermath of the election yields rose higher still with investors focusing on the potential inflationary impact of Trump’s protectionist policies of trade tariffs.

Both bond and equity markets reacted positively to the nomination of financier Scott Bessant for the position of Treasury Secretary. Bessant is an investing veteran and seen, in contrast to some of Trump’s other nominations, as highly qualified for the role. Neither Kamala Harris nor Donald Trump paid any great attention to addressing government debt and budget deficits on their respective campaign trails. If approved, Bessant will have an important task of keeping financial markets calm and orderly in the face of ever-increasing debt levels.

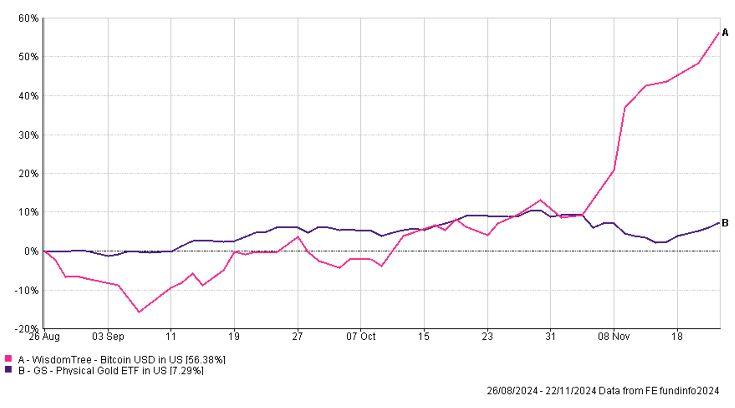

Gold prices have traded in a volatile fashion in November, suffering their biggest single-day decline in four years on reports of possible ceasefires in the Middle East. Cryptocurrencies in contrast made gains in November with Bitcoin trading close to the $100,000 milestone for the first time. Investors hope the Trump administration will create a favourable regulatory environment for cryptocurrencies.

UK Economy

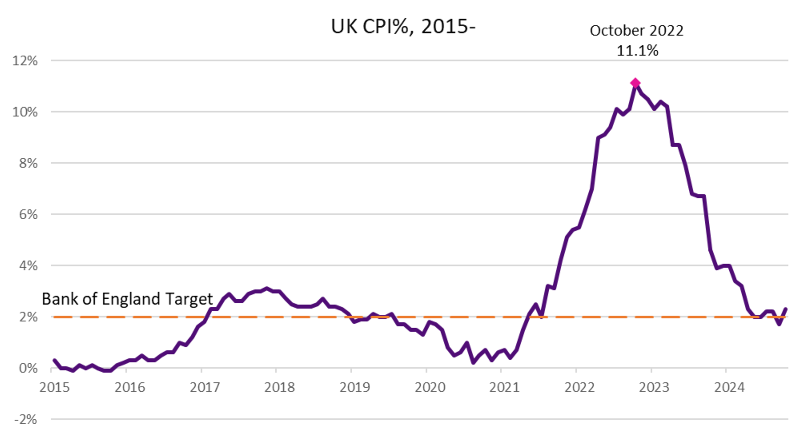

In the UK, the Consumer Prices Index (CPI) measure of inflation for October increased from 1.70% in September, to 2.30%. This took the rate back above the target level of 2.00%. The largest upward contributors came from electricity and gas prices following an adjustment to the energy price cap.

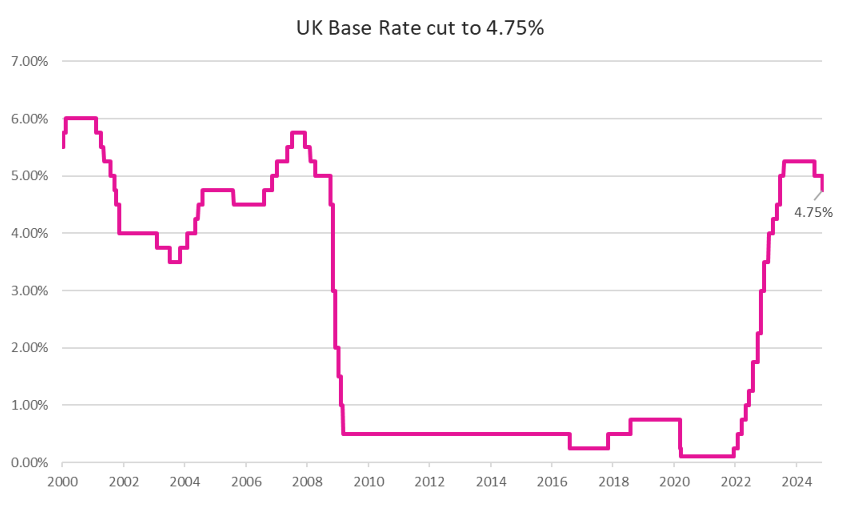

Earlier in the month, the Monetary Policy Committee (MPC) of the Bank of England, reduced interest rates from 5.00% to 4.75%. The Bank Governor, Andrew Bailey, cautioned following the decision that while rates would likely fall gradually, it is important to not cut too fast and risk inflation rising again. The inflation data, rising above the target rate of 2.00%, corroborated this stance.

The Office for National Statistics estimated the UK economy to have grown by 0.10% between July and September. Notably with a small contraction of 0.10% in September. Consensus forecasts from economists had expected growth of 0.20%, with growth in the preceding quarter estimated at 0.50%.

Budget Reaction

The response from investment markets to the first Labour budget in fourteen years was mixed. The announcement of significant levels of borrowing saw government bond yields rise sharply. Albeit they were also rising in line with US government bond yields in anticipation of the election. Several high-profile retailers have expressed concern that higher costs associated with employing modestly paid staff will be passed onto consumers, potentially sparking a further round of inflation.

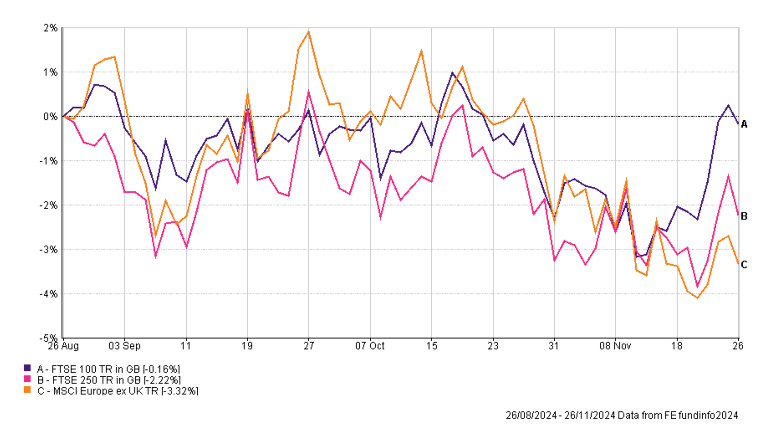

Sterling has weakened against the US dollar, as traders ponder the implications of potential trade tariffs from the US and higher borrowing announced by the UK Government. The FTSE 100 and FTSE 250 suffered declines in the lead up to, and immediate aftermath, of the Budget. Gilt yields, after initially rising, settled as the month progressed and equity markets moved higher in late November with UK indexes recovering much of their lost ground. Overall, market reaction has been placid in comparison to moves seen in the aftermath of the ill-fated mini budget in September 2022.