We have said before that investment markets do not like uncertainty; increasing the number of variables makes it more difficult to forecast the outlook for companies and markets, leading to increased volatility. Although markets are facing a number of questions as we move into the festive season, there are reasons for both optimism and concern.

COP26

Much of the press in early November was dominated by COP26, the global conference to discuss efforts to combat climate change. Investment markets were not moved to any great degree as a result of the talks. Significant compromises were made to pledges which fell some way short of what was required. However, we believe that the transition to a net zero economy is likely to provide opportunities within investment markets as new technologies and practices emerge and there has been an increased interest in sustainable investing.

Covid

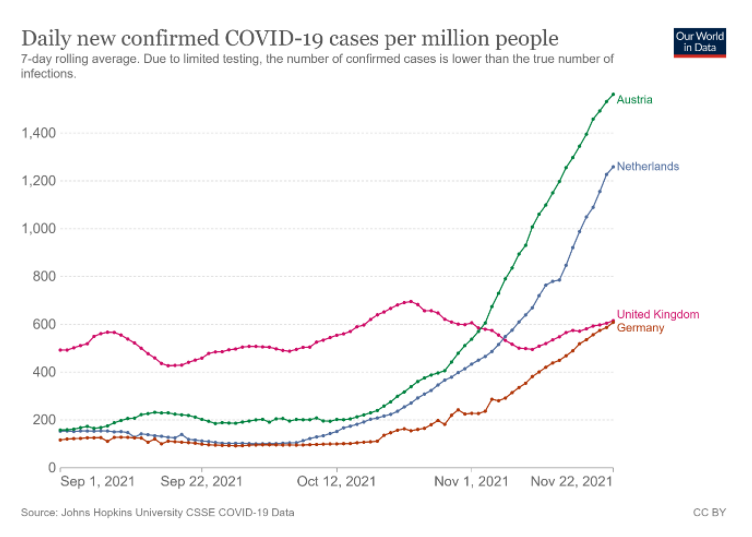

The summer months provided welcome respite from commenting on the pandemic with the warmer months limiting the impact of the virus. However, with the arrival of colder months, a rise in cases has prompted new restrictions across Europe. The Netherlands announced a three-week partial lockdown, Germany has introduced a new system of tougher controls, while Austria has returned to a full national lockdown. Case numbers certainly look considerably higher when compared to the numbers which resulted in previous lockdowns and investment markets are nervous this could potentially mean more restrictions in more countries.

However, we feel this is less likely due to how effective the vaccines currently are in preventing higher cases translating into higher numbers of hospitalisations. The biggest worry for markets regarding the virus continues to be that a vaccine-resistant variant might emerge. It is in this outcome that major economic restrictions would be likely. As long as the vaccines continue to be effective, markets will be concerned, but not obsessed, by covid. However, the uncertainty it causes over potential economic obstacles is likely to lead to increased market volatility throughout the winter.

Inflation

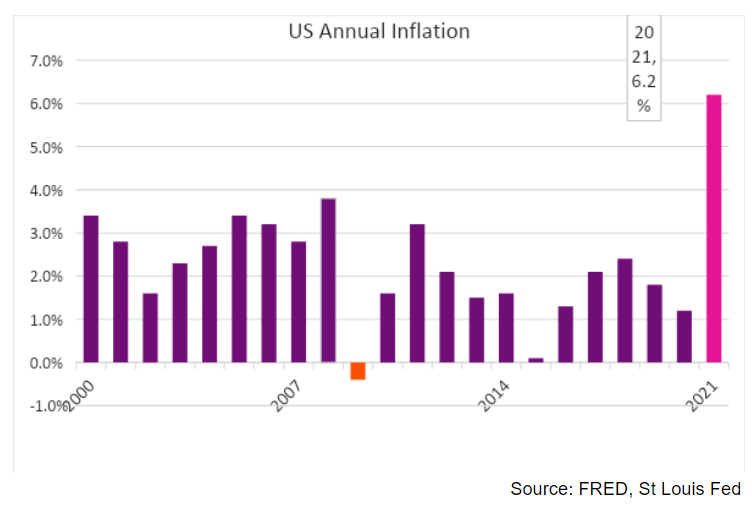

Investment markets, most specifically bond markets, have been highly volatile in recent months due to the action, and in some cases inaction, of central banks in combatting rising inflation. Markets were highly confident that the Bank of England would raise interest rates at its November Monetary Policy Committee (MPC) meeting following comments from Andrew Bailey, the Governor of the Bank of England (BoE), that the bank “will have to act”. These comments were interpreted as a clear signal that interest rates would rise at the next MPC meeting and therefore markets were surprised following the decision at the November meeting to leave the base rate unchanged.

Central banks are not in an easy position. Raising interest rates would have no impact on the structural issues that are causing price rises in many areas of the economy. The UK base rate does not create extra capacity in Chinese shipping ports, does not magically create new supplies of natural gas, and does not solve the labour shortage in many areas of the economy. These issues, among others, are entirely out of the banks control and taking a more hawkish policy stance may simply damage the UK’s economic recovery.

But central banks risk losing credibility and placing themselves in an untenable position. Inflation in the US reached a three-decade high in November while UK inflation is forecast by the BoE to reach 5% early next year. Their mandate is to maintain balance and structure in the economy by ensuring price and financial stability i.e limiting inflation. If they do not act, they risk being seen as not fulfilling their only directive. Whether this is then seen as a political decision or more worryingly a perceived admittance that they do not have the ability to conduct their responsibilities, neither will deliver confidence in Central Banks. It does ask a big question surrounding the strength of the UK economy though when the BoE is cautious about the impact of even minor policy adjustments.

Geopolitical risks

Another area where uncertainty is elevated is in raised geopolitical tensions. The scenes on the Belarus border with Poland are increasing fears it may be a proxy for Russian intervention in Eastern Europe. There have been reports of Russian troops assembling on the border with Ukraine and there are worries President Putin may take the opportunity to test the waters. Elsewhere, the presidents of the USA and China held a virtual meeting with discussions over Taiwan causing unease. All-out war is unlikely, but investment markets remain apprehensive about the potential for any small conflicts to escalate.

How to deal with uncertainty

With heightened uncertainty this reinforces the importance of making sure your investments are suitably diversified. By spreading your investments across a range of different asset classes and regions it means that when the value of one falls, another might rise. Here at Vesta Wealth, we ensure all our clients’ investments are diversified to minimise the impact of this uncertainty and volatility while being positioned to take advantage of opportunities as they arise.

Invitation

If you would like to discuss your financial plan and investment strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.