Global equity markets continue to exhibit considerable volatility, as inflation, and the resultant pressure on consumer incomes and company profits, has created negative sentiment in the investment community. These headwinds combined with the ongoing war in Ukraine and continuing disruptions to supply chains have resulted in a challenging month for investment markets.

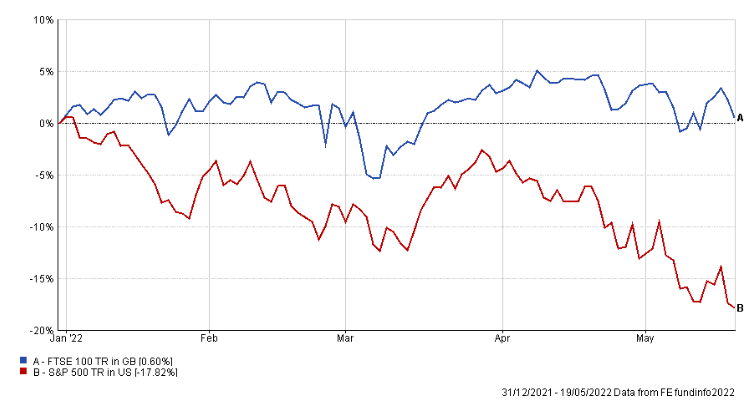

It is a continuing theme that rising inflation is putting upwards pressure on bond yields as central banks seek to increase interest rates in an attempt to control it. This continues to place previously highly rated growth stocks under significant pressure as investors have continued to rotate into cash generative, value/cyclical stocks. In relative terms, this has favoured the FTSE 100, which has a notable value tilt. Since the beginning of the year, the index generated a total return of 0.60%, comfortably outperforming the US S&P 500 index, which has lost 17.82% in dollar terms.

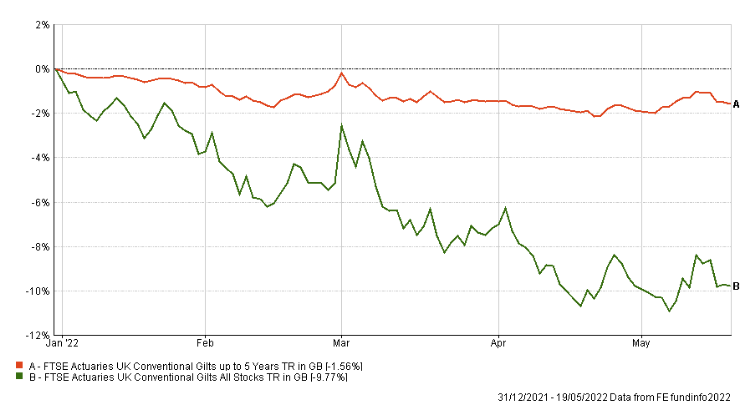

Bonds have offered little comfort, with the FTSE Actuaries UK Conventional Gilts All Stocks Total Return index falling nearly 10% over the same period. Short dated, lower duration, fixed income stocks have shown greater resilience.

Still Inflation

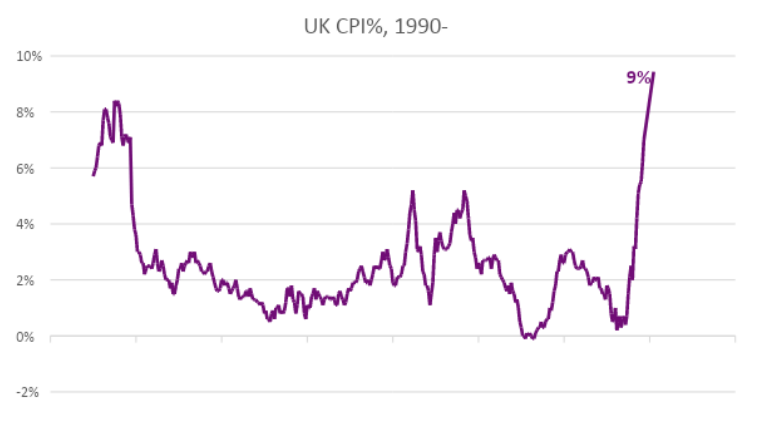

It was announced earlier in May that Inflation has hit a 40 year high in the UK of 9% as energy price rises were added to the measure. High inflation is not simply a UK problem; but a global trend as a result of disrupted supply chains matched with increased demand for goods. This has created a dilemma for central bankers who must assess the ability of higher interest rates to tame inflation, as the causes of such rests in circumstances beyond their control.

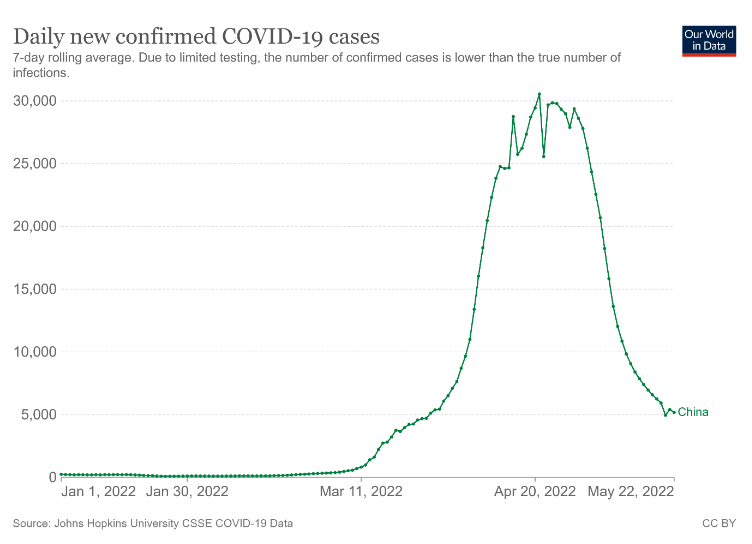

The war in Ukraine has become more about economic and military attrition. Russia and the west are fighting a proxy military and economic war, the latter in the form of sanctions adding to inflationary pressures. In Asia, the zero-tolerance approach of the Chinese government towards Covid-19 is impacting global supply chains. However the Chinese government have indicated an intention to stimulate the economy alongside an easing of Covid-19 restrictions.

Even as these supply chain disruptions eventually resolve themselves, inflation, or at least higher prices, might not fall back to any ‘pre-covid’ levels. The world is undergoing considerable change, as covid and geopolitical tensions, are rolling back long-periods of progressive globalisation, and associated price declines. The need for countries to shorten supply chains in the interests of national security, means the era of ever cheaper consumption is drawing to an end as vast reservoirs of cheap labour have started to dry up.

A higher cost, higher wage alternative appears to be emerging, which is prompting investors to reprice longer duration assets, such as bonds and growth stocks. Investors are favouring companies which can generate and offer cash now, rather than cash at a more distant point, premised upon demanding growth assumptions. The analyst community have arguably been too slow to recognise that lock-down earnings for shop-, entertain-, and exercise-at-home stocks, have been extrapolated too far.

With volatility comes opportunity

While the volatility that markets are currently experiencing can be unsettling for investors, such conditions create long-term opportunities.

For instance if climate change goals are to be achieved, there must be vast investment in smarter infrastructure and low carbon economies. While working patterns and where we work changes, the demand for energy efficient office space remains robust, as does sensibly priced retail space. While profits have been taken in the logistics space, as investors have begun to look at the growth of ecommerce more realistically, this is likely to lead to more sustainable pricing. With fixed income investments temporarily losing their ‘safe haven’ status, rising yields will eventually attract back lower risk investors, particularly when inflationary pressures are shown to have peaked.

A sharp reversal in what were once considered one-way bets, has provided a sobering reminder that diversification remains important. It is easy to become seduced by compelling rhetoric, which justifies richly valued assets, and equally easy to write off those no longer considered relevant. Even the much taught just in time production has had to acknowledge the need for just in case. While trading with global partners will always bring benefits, becoming over reliant is no longer as viable in a less predictable world. The volatility we are currently seeing is in many ways a function of markets attempting to price the new realities that face us. Change, while at times may seem daunting, does bring new opportunities for those optimistic enough to pursue them.

Invitation

If you would like to discuss your financial plan and investment strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

e: [email protected]

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.