July has presented investors with much to contemplate, both domestically, and internationally. Politically, Boris Johnson delivered his own tragedy. His Prime Ministership suffering an Icarus style fate. One controversy too many saw him plunge to a mere caretaker role. But there is little time for sentiment, politics moves on. Liz Truss and Rishi Sunak now face a battle not only for the role of next Prime Minister, but also the heart of The Conservative Party. Should we tax our way to a prudent financial position, or operate a less burdensome fiscal position, and grow our way out of debt? This question is more than about campaign hustings, it is ideological, and will impact the economy and financial markets.

Fighting Inflation

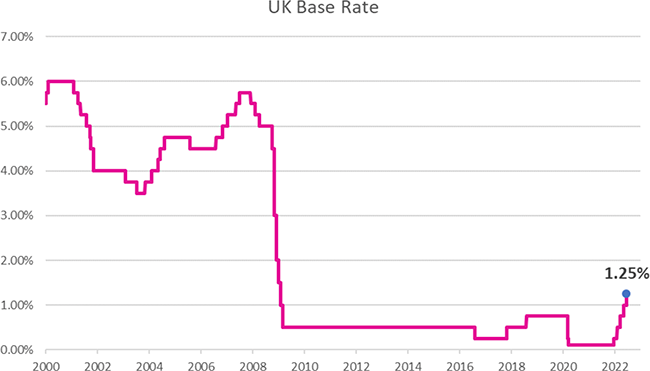

The June 2022 inflation print in the UK established a new 40 year high at 9.40%. Standing tall of wage increases, industrial unrest in unionised workforces is on the rise, which could prompt more Thatcherite comparisons if the new Prime Minister is confronted with a ‘winter of discontent’. Inflation is not an issue isolated to the UK however with decades high price pressures a phenomenon being suffered throughout much of the developed world.

With central bankers finally alert to the challenge of battling inflation, the projected path of future interest rate increases is becoming steeper. Even the hitherto ultra-dovish European Central Bank recently raised rates by 0.50%, the largest rise in 20 years, to a hardly lofty 0.00%. Both the US Federal Reserve, and the Bank of England’s Monetary Policy Committee in the UK, are expected to announce substantial hikes at their next respective meetings.

Financial markets are likely to remain unsettled until inflation has peaked, and the trajectory of interest rates becomes clearer. As this conundrum has impacted both equity and bond investors, 2022 has been a vexing year for investors thus far. This is of course unsettling, but economic cycles were never meant to be smooth, and inflation will eventually peak and head lower.

Energy Pressures

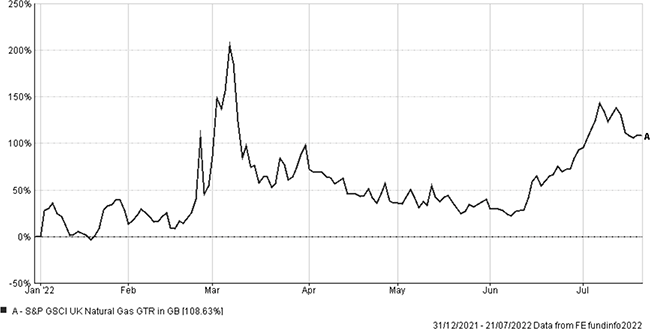

Geopolitical factors remain poignant. The war in Ukraine has taken many forms. Alongside the military theatre, there is an economic struggle. The financial sanctions imposed on Russia and some of its influential citizens, as punishment for the invasion, are only amplifying some inflationary pressures. This can be seen most notably in energy markets as restricted supplies have seen surging energy prices. The required move to sustainability, in the headlines again during the recent record heatwave in the UK, and wider clean energy aspirations must now dovetail with more independent, less strategically vulnerable, energy production and supply chains. Both provide long-term opportunities for investors, despite the near-term volatility.

Investment markets have been under pressure in 2022 primarily due to concerns surrounding inflation and the impact this might have on economies and the businesses within them. Recession fears continue to weigh on investor sentiment however economic data continues to offer reasons to remain optimistic. Labour markets are buoyant, and economic activity, while weakened, has yet to turn fully negative.

Earnings Season

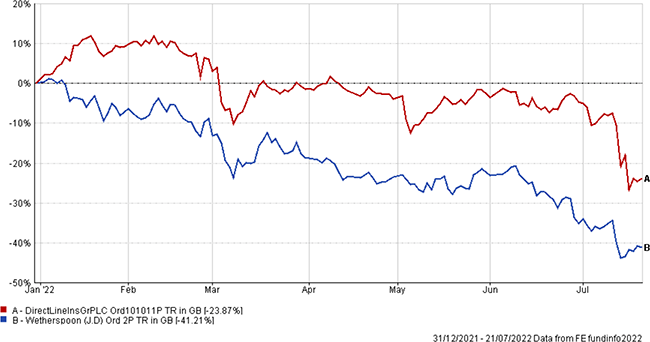

While the economic environment is challenging and broad market indices have mostly declined year to date, equity market falls often overlook the diversity of their constituent businesses. Analysts can also be slow to adjust earnings estimates to reflect differing conditions. This is most evident in the current earnings season, with the winners and loser stocks more sharply demarcated in performance. In the UK, motor insurers, Direct Line and Sabre Insurance Group fell heavily, as claims inflation exceeded premium rate growth. Meanwhile, the value proposition of JD Wetherspoons has provided little support against declining beer sales.

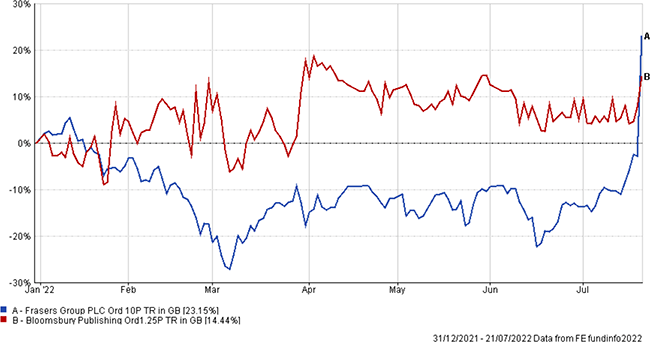

But updates have not been uniformly disappointing. Frasers Group, operator of the Sports Direct business, demonstrated that its retail strategy is delivering growth. Elsewhere, Bloomsbury Publishing has illustrated that the reawakening of the appeal of a good book has outlasted the lockdown periods. The same trends may be observed in the US. Streaming giant Netflix rallying on less than anticipated subscriber losses and social media stock, Snap, plunging following disappointing second quarter results.

What next?

Volatility can depress asset prices and portfolio performance in the short-term, but as long-term investors, rather than speculators, it is necessary to maintain faith and conviction where it is due. The remainder of the 2022 will be eventful. Inflationary pressures remain and political changes in the second half of the year could set a new direction for policy.

A new UK Prime Minister will set a revised course. The US mid-term elections will be keenly watched to see who controls the key legislative chambers. There will also be elections in Brazil and Italy. Brazil is South America’s largest economy and a key driver for the continent. In Italy, the spread of Italian bond yields is widening over German bunds and the nation needs to present a credible fiscal plan. Finally, as Europe scrambles to secure winter energy supplies, the weather forecast will be studied more keenly than ever in attempts to determine the level of demand. At Vesta Wealth, we remain on hand to answer any queries you have concerning your investments.

Invitation

If you would like to discuss your financial plan and investment strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

e: [email protected]

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.