Following the positive returns made by investment markets in 2020, 2021 delivered more mixed outcomes. Some assets continued to deliver positive returns while others struggled under the weight of uncertainty. These returns were driven by issues that dominated the investment narrative for much of the year as investors also started looking beyond the pandemic as life continues its slow move towards normality.

2021 in review

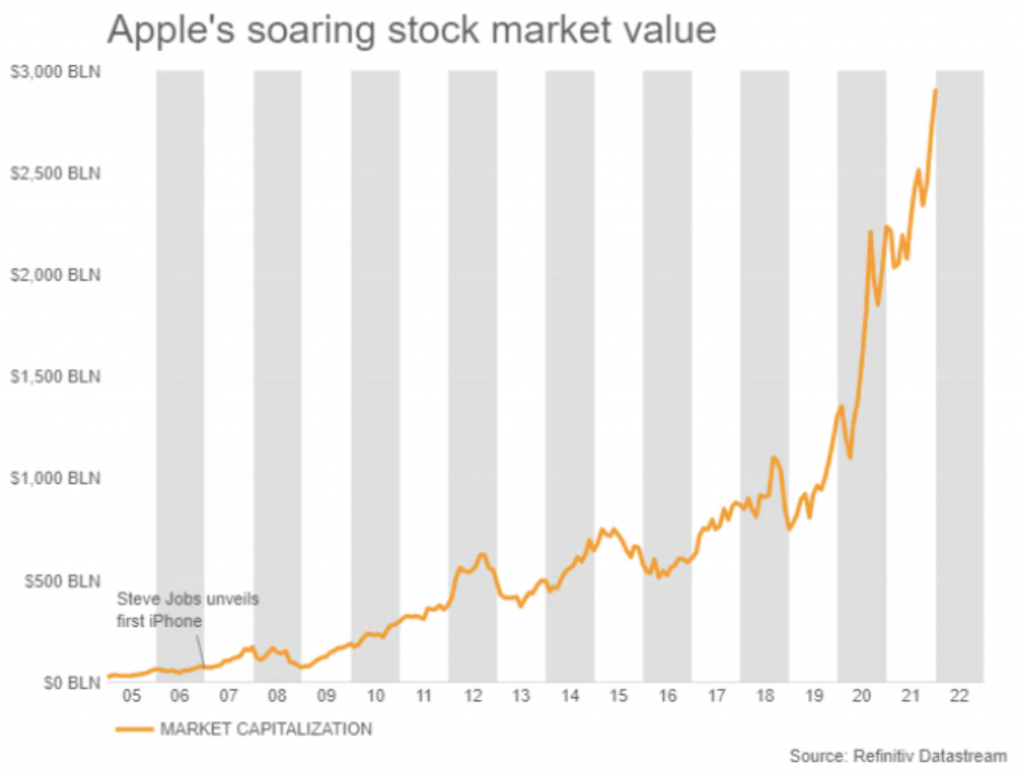

Continuing their strong performance from 2020, developed market equities were the standout performers in 2021, with North American equities delivering the best overall returns. The sharp rise in the valuation of technology companies was a large contributing factor to this performance and saw Apple become the world’s first $3 trillion company early in 2022. This performance has led to question marks over the sustainability of these valuations and concerns that areas of the market might be overvalued.

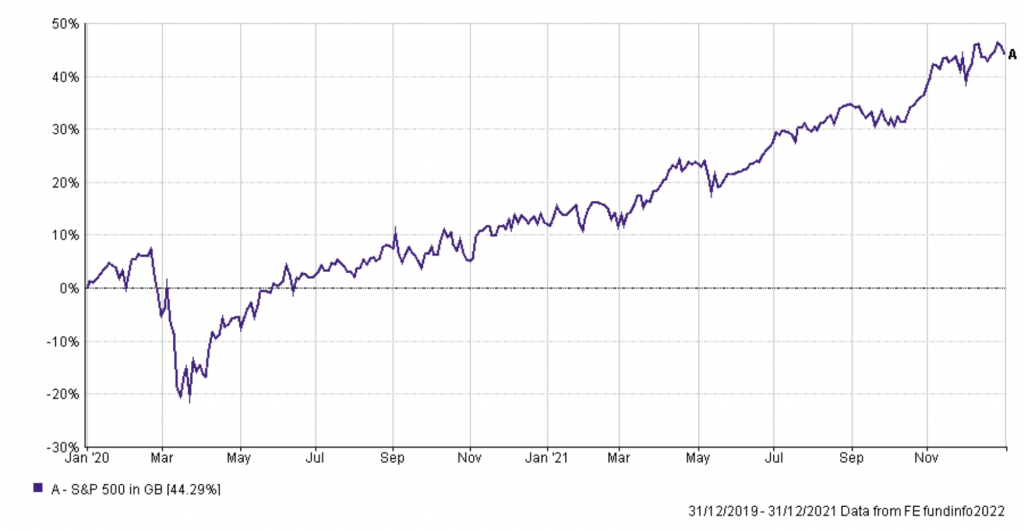

However, investors paid little regard to these concerns. The S&P 500, a US stock market index, recorded a new all-time high on 70 different days during 2021 as investors continued backing the world’s biggest companies. Much of this performance was a result of continued economic support from governments and central banks, alongside increased investor enthusiasm regarding the strength of the economic recovery and what a return to normal might mean for that recovery.

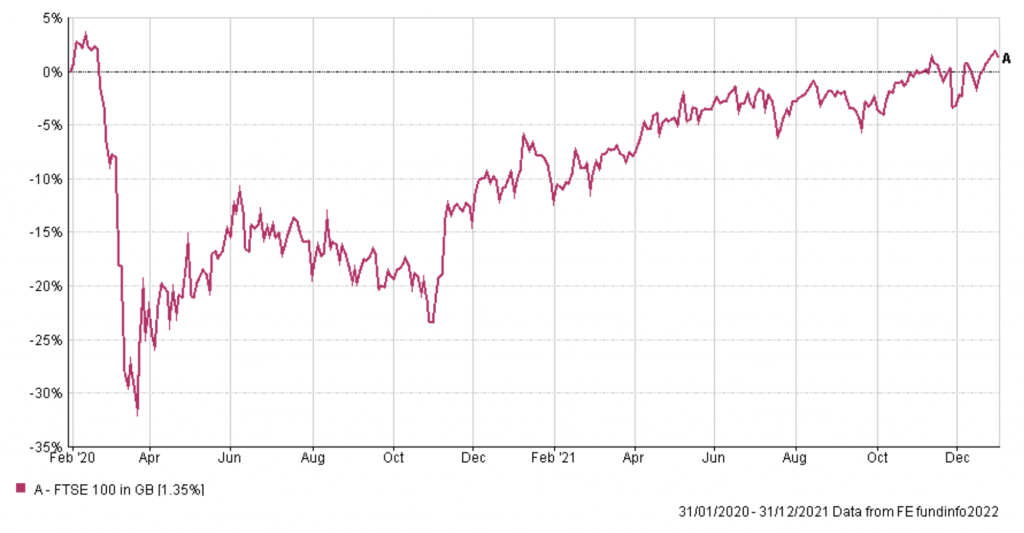

UK equities which had struggled in 2020 also benefitted from increased optimism and improving economic conditions as the world recovered from covid. The FTSE 100 was the only major stock market in 2020 to deliver a negative return being made up of companies that were heavily impacted by lockdown restrictions such as those in the travel, leisure, banking and oil and gas sectors. With relatively high vaccination rates the UK benefitted from more open trading conditions in 2021 and UK companies thrived as a result; with the FTSE 100 finally recovering to its ‘pre-covid level’ in December.

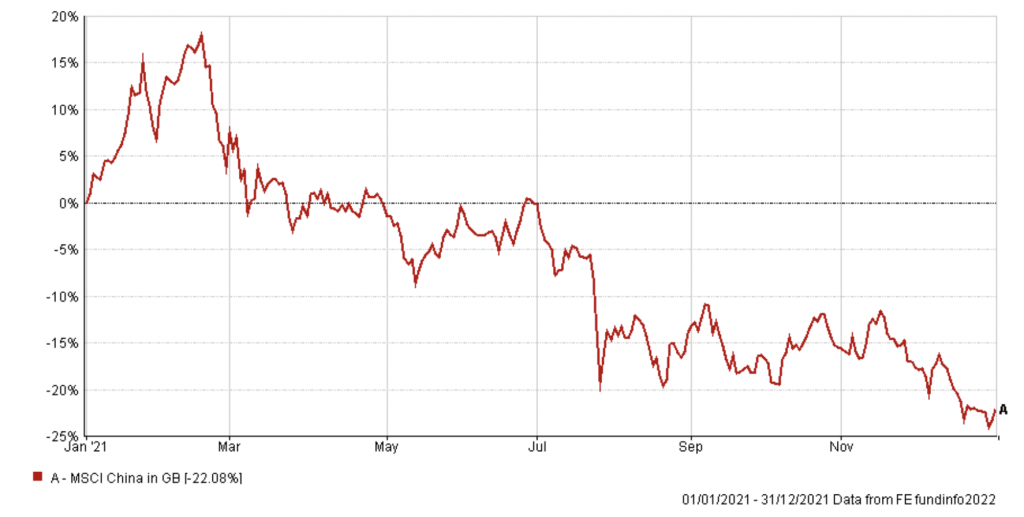

2021 was not all plain sailing for equity markets however as Asian and Emerging markets battled heightened uncertainty alongside greater troubles with covid. China started 2021 remarkably, delivering double digit returns through February. However, sentiment quickly changed following regulatory intervention by the Chinese government over monopoly concerns regarding some of China’s largest companies. This uncertainty combined with tightened monetary policy and the strict covid controls in China meant it was a difficult year for the country’s equity market.

Covid in 2021

Covid continued to play a large role in investment markets in 2021 as both the Delta and Omicron variants placed renewed pressures on economies. Omicron caused greater volatility due to initial fears about its potential resistance to vaccines. However, evidence has proven that vaccines remain effective against Omicron, and the effects of the variant on those who are infected have been relatively mild. Investors have therefore grown more confident about future prospects regarding the virus. With restrictions beginning to be lifted, covid will remain an issue and any new variants will pose questions, but the virus does not sit at the forefront of investor concerns at this time.

Inflation

As inflation readings continued rising throughout 2021, investor concerns rose in tandem surrounding the policy changes central banks might make to combat sustained price rises. Throughout most of 2021, elevated inflation was downplayed as a ‘transitory’ phenomenon. The argument was that it would only be temporary as economies reopened from lockdown restrictions and supply and demand imbalances would eventually normalise. Central banks hoped this would mean they would not need to take action.

Their hesitancy to act resulted from central banks fearing they were in a catch-22 situation. There is a strong argument that economies, and in turn equity markets, have recovered so quickly because of the generous support from monetary policy. However, there is another argument that the generous policy is a contributing factor to rising inflation. If central banks take the wrong action and remove supports the economic recovery may falter, a major concern for central banks when economies were forced into lockdown restrictions in late 2021 following the outbreak of the Omicron variant. Yet without changing policy, runaway inflation may cause greater structural problems for the economy.

Source: ONS

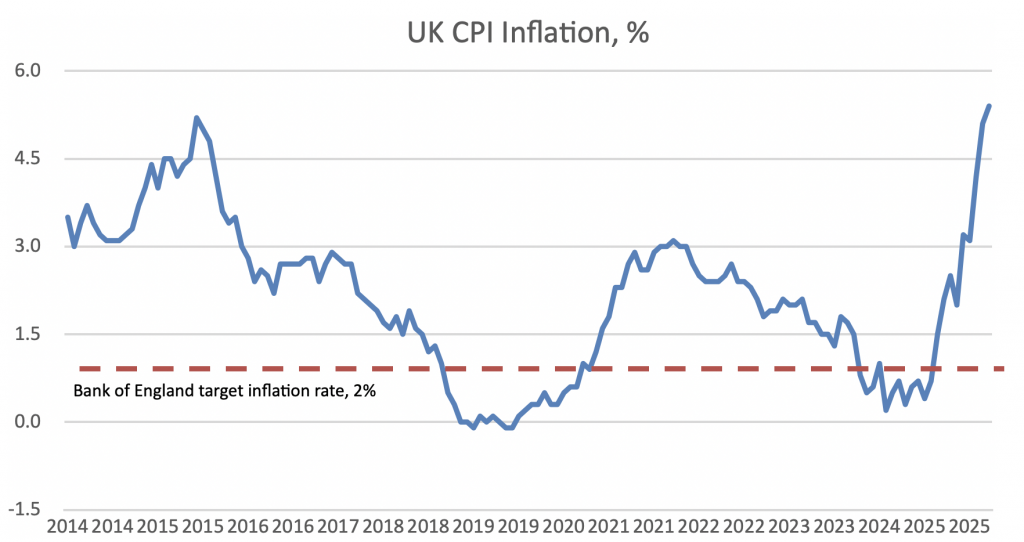

As 2021 moved on, it became clearer that inflation has not been a temporary phenomenon. Early this year, US inflation hit a 39-year high of 7% while UK CPI inflation is at its highest level since 1992 at 5.4%. Both figures are well in excess of the UK and US central banks’ target inflation levels of 2%. With inflation remaining stubbornly high, central banks have indicated they will have to take action to try to manage the sharp rises in prices, despite any pressure or damage this could cause to the economy.

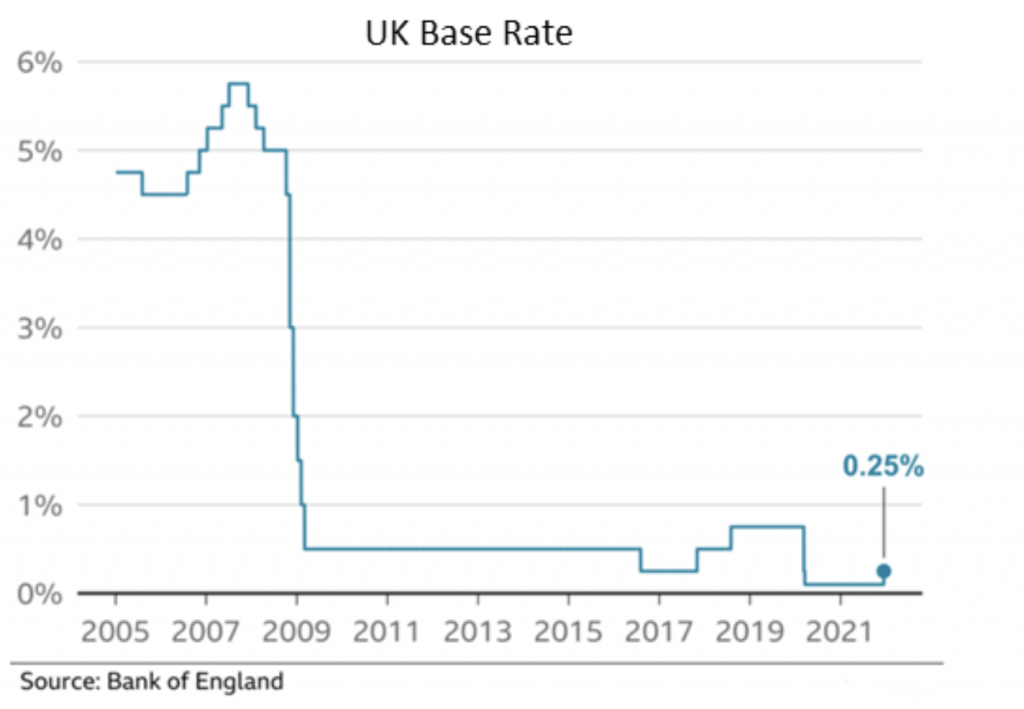

The concern for investors, and one reason for volatility in the opening weeks of the year, is what this action might look like and when it might be taken. The Bank of England surprised investment markets in December by raising interest rates for the first time in more than three years and there has been concern there may be more surprises in an upcoming meeting of the Federal Reserve, the US central bank. Less supportive policy makes for more difficult trading conditions for businesses and economies; with concern that central banks may surprise markets with more restrictive policies earlier than expected, investor sentiment has been challenged.

Ukraine

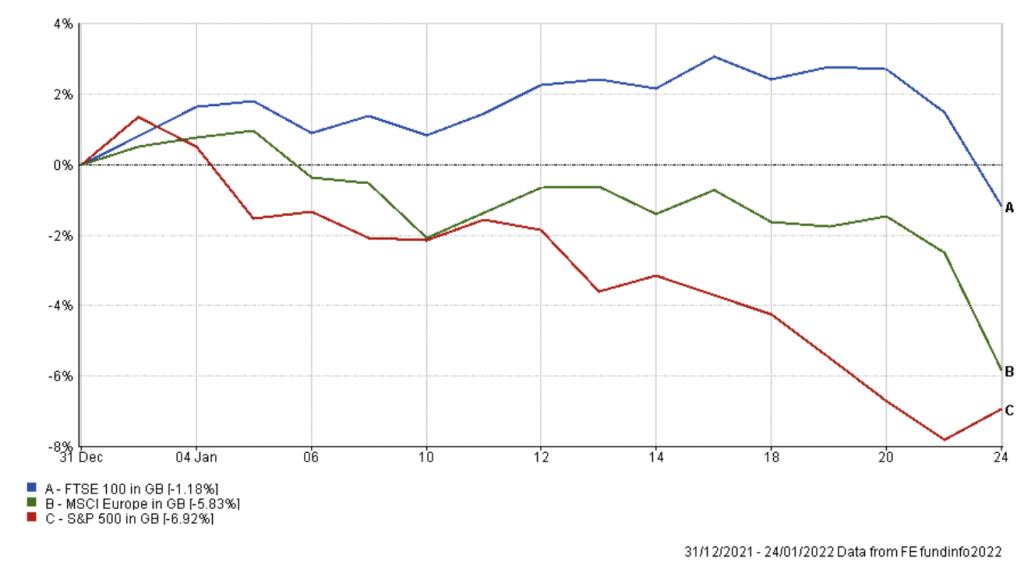

In recent weeks the news cycle has been increasingly dominated by reports of growing numbers of Russian troops amassing on the Eastern border of Ukraine. This situation has been ongoing for months; rumours have been escalating that the rising numbers of troops might now be a pre-cursor to military action. Investors do not like uncertainty and war is an inherently uncertain situation. With western leaders distracted by their own domestic issues, President Putin may feel there is a grim opportunity in Ukraine. Whether any military action leads to direct conflict is uncertain, any intervention is likely to result in economic sanctions at least. This will be damaging to trade and economic activity and fears over the situation created a risk-off mood in markets and caused a fall in investment values in the early weeks of 2022.

Since the very beginning of the pandemic, we have reminded our clients about the importance of staying invested for the long term, of the difficulty of timing the market, and how by selling out when markets fall it could be detrimental to achieving your financial objectives. It is natural to feel concerned about the impact of events such as inflation and the geopolitical tensions in Eastern Europe on your investments. But the mantra of time IN the market, and not timing the market, will remain true as volatility and uncertainty continues now and throughout 2022.

Invitation

If you would like to discuss your financial plan and investment strategy, then we would love to hear from you. Get in touch with your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.

Reach us via:

t: 01228 210 137

This content is for information purposes only. It should not be taken as financial or investment advice. To receive personalised, regulated financial advice regarding your affairs please consult your Financial Planner here at Vesta Wealth in Cumbria, Teesside and across the North of England.